亚太地区冷成型和冷镦市场预测至 2028 年 – COVID-19 影响和区域分析 – 按材料(铝、合金钢、不锈钢等)和行业(航空航天和国防、汽车、工业设备和机械及其他)

No. of Pages: 94 | Report Code: BMIRE00026923 | Category: Manufacturing and Construction

No. of Pages: 94 | Report Code: BMIRE00026923 | Category: Manufacturing and Construction

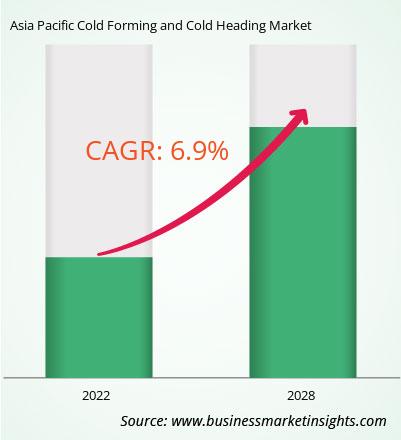

亚太地区的冷成型和冷镦预计将从 2022 年的 91.8318 亿美元增长到 2028 年的 137.2086 亿美元。预计复合年增长率为 6.9% 2022年至2028年。

汽车行业对冷成型和冷镦的需求不断增长

汽车工业广泛使用冷镦机成型的零件。用于冷镦的主要金属包括铜基(Cu)金属合金、纯铜、黄铜、磷青铜、不锈钢和铝。由冷镦机制造的接头是用于各种汽车控制单元、发动机控制单元(ECU)、压力传感器和其他车载传感器的端子和引脚。技术进步、气候变化相关政策以及不断变化的消费者品味正在推动对环保、节能、智能汽车以及电动和混合动力汽车创新的需求。跨国汽车制造商在印度、印度尼西亚、马来西亚和泰国等亚太国家进行了投资。在这些国家,冷镦机市场在未来几年提供增长机会。因此,所有这些市场趋势和汽车行业投资的增加正在推动对冷成型和冷镦工艺的需求。

市场概览

根据国家/地区,亚太地区 (APAC) 冷成型和冷镦市场分为澳大利亚、中国、印度、日本、韩国和亚太地区其他国家/地区。过去十年,中国和印度已成为全球制造中心。这些国家政府不断采取的促进制造业发展的举措正在影响地区和全球制造商设立生产工厂。随着全球医疗保健领域的不断进步,该地区的医疗器械制造商纷纷增加产量,并不断投资高科技医疗器械的开发。这些因素正在增加该地区医疗器械的制造量,从而增加了对冷成型和冷镦解决方案的需求,这些解决方案用于在制造和促进市场增长的同时集成医疗器械的多个小部件。由于国内外汽车制造商不断增加的投资以及政府促进汽车行业发展的举措,亚太地区汽车行业多年来一直在快速增长。例如,2021年4月,中国政府宣布要求汽车制造商增加电动汽车的产量。政府采取这一举措是为了提高中国电动汽车销量的比例。此外,汽车公司在该地区建立制造工厂的投资不断增加,预计将增加对冷成型和冷镦解决方案的需求。例如,2022 年 6 月,宝马集团在其耗资 22 亿美元的新工厂开始生产电动汽车。同样,2020 年 10 月,现代汽车宣布在新加坡开发新的电动汽车和研发工厂。因此,上述因素预计将对亚太地区冷成型和冷镦市场做出贡献。

;

亚太地区冷成型和冷镦市场细分

;

亚太地区冷成型和冷镦市场按材料、行业和国家细分。

Altra Industrial Motion Corp;巴拉特锻造厂;德林格-内伊公司;福井Byora有限公司;卡利亚尼锻造厂;和 STANLEY 是亚太地区冷成型和冷镦市场的领先公司。

Strategic insights for Asia Pacific Cold Forming and Cold Heading involve closely monitoring industry trends, consumer behaviours, and competitor actions to identify opportunities for growth. By leveraging data analytics, businesses can anticipate market shifts and make informed decisions that align with evolving customer needs. Understanding these dynamics helps companies adjust their strategies proactively, enhance customer engagement, and strengthen their competitive edge. Building strong relationships with stakeholders and staying agile in response to changes ensures long-term success in any market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 9,183.18 Million |

| Market Size by 2028 | US$ 13,720.86 Million |

| Global CAGR (2022 - 2028) | 6.9% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By 材质

|

| Regions and Countries Covered | 亚太地区

|

| Market leaders and key company profiles |

The regional scope of Asia Pacific Cold Forming and Cold Heading refers to the geographical area in which a business operates and competes. Understanding regional nuances, such as local consumer preferences, economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved regions or adapting their offerings to meet regional demands. A clear regional focus allows for more effective resource allocation, targeted marketing, and better positioning against local competitors, ultimately driving growth in those specific areas.

The Asia Pacific Cold Forming and Cold Heading Market is valued at US$ 9,183.18 Million in 2022, it is projected to reach US$ 13,720.86 Million by 2028.

As per our report Asia Pacific Cold Forming and Cold Heading Market, the market size is valued at US$ 9,183.18 Million in 2022, projecting it to reach US$ 13,720.86 Million by 2028. This translates to a CAGR of approximately 6.9% during the forecast period.

The Asia Pacific Cold Forming and Cold Heading Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Cold Forming and Cold Heading Market report:

The Asia Pacific Cold Forming and Cold Heading Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Cold Forming and Cold Heading Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Cold Forming and Cold Heading Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Cold Forming and Cold Heading Market

Get Free Sample For Asia Pacific Cold Forming and Cold Heading Market