North America Semiconductor Silicon Wafer Market

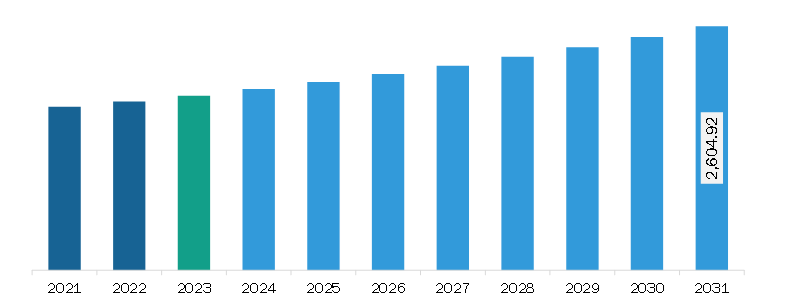

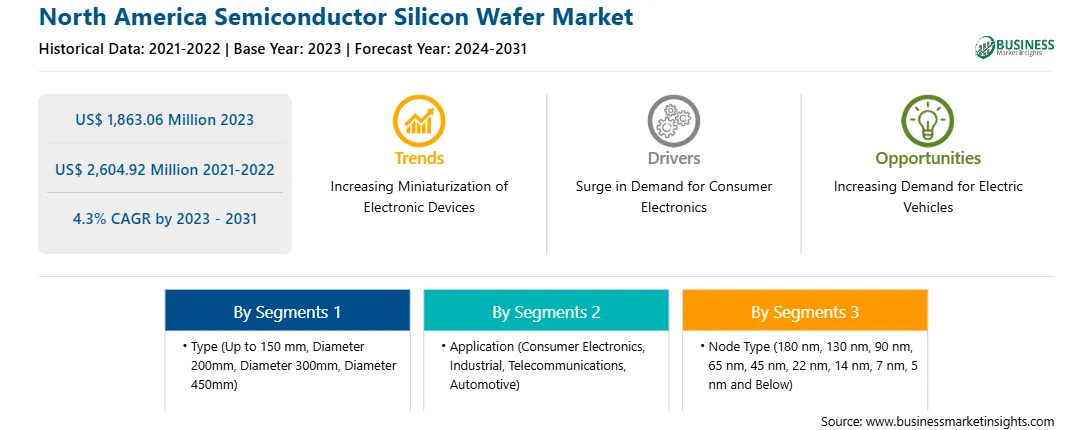

The North America semiconductor silicon wafer market was valued at US$ 1,863.06 million in 2023 and is expected to reach US$ 2,604.92 million by 2031; it is estimated to register a CAGR of 4.3% from 2023 to 2031.

The demand for tablets, smartphones, wearables, and other consumer electronics devices, such as smartwatches, fitness trackers, VR headsets, and headsets, is increasing worldwide. These consumer electronics are used for various purposes, which include accurate tracking of real-time data and providing enhanced convenience. According to the Groupe Speciale Mobile Association (GSMA), smartphone adoption across the globe was 76% in 2022, totaling 6.4 billion smartphone connections. The adoption is expected to reach 92% by 2030, making 9 billion connections worldwide. As per the same report, smartphone adoption in North America was 84% in 2022 and is expected to rise to 90% by 2030.

In multiple industries, wearables are utilized in tracking and managing personnel. For example, miners can be tracked under deep tunnels and alerted with a notification if signs of distress occur. Similarly, wearables are used for patients suffering from dementia to track their location if they go missing or get themselves in situations that require emergency help. As semiconductors such as silicon wafers can be used to manufacture chips and microchips in electronic devices, their demand is increasing worldwide. In addition, silicon wafers are used for the production of ICs, which is one of the important parts of various electronic devices, further boosting its demand. Thus, the growing demand for consumer electronics drives the North America semiconductor silicon wafer market.

North America has a significant share of the semiconductor silicon wafer market. The region has a vast presence of various fabless companies such as Qualcomm, Altera, LSI Corporation, Marvell Technology, Nvidia, ATI Technologies Inc, etc. Further, the region is also conducting various research and development activities on microelectronics, thereby increasing the production of silicon wafers. For example, in July 2024, as part of the Investing in America tour, the Biden-Harris Administration announced that the US Department of Commerce and GlobalWafers America, LLC and MEMC LLC ("MEMC"), subsidiaries of GlobalWafers Co., Ltd. ("GlobalWafers"), have signed a nonbinding preliminary memorandum of terms (PMT) to provide up to US $400 million in proposed direct funding under the CHIPS and Science Act to help onshore critical semiconductor wafer production and advance US-based technology leaders. President Biden signed the bipartisan CHIPS and Science Act, a crucial component of the Investing in America plan, ushering in a new era of semiconductor production in the US. The proposed CHIPS investment will fund the development of new wafer production facilities, creating 1,700 construction jobs and 880 manufacturing jobs. Such government initiatives across the region drive the semiconductor silicon wafer market.

Strategic insights for the North America Semiconductor Silicon Wafer provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market. The geographic scope of the North America Semiconductor Silicon Wafer refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas. Get more information on this report

Get more information on this report North America Semiconductor Silicon Wafer Strategic Insights

Get more information on this report

Get more information on this report North America Semiconductor Silicon Wafer Report Scope

Report Attribute

Details

Market size in 2023

US$ 1,863.06 Million

Market Size by 2031

US$ 2,604.92 Million

Global CAGR (2023 - 2031)

4.3%

Historical Data

2021-2022

Forecast period

2024-2031

Segments Covered

By Type

By Application

By Node Type

Regions and Countries Covered

North America

Market leaders and key company profiles

Get more information on this report North America Semiconductor Silicon Wafer Regional Insights

Get more information on this report

Get more information on this report

The North America semiconductor silicon wafer market is categorized into type, application, node type, and country.

By type, the North America semiconductor silicon wafer market is segmented into Up to 150 mm, Diameter 200mm, Diameter 300mm, and Diameter 450mm. The Diameter 300mm segment held the largest share of the North America semiconductor silicon wafer market share in 2023.

In terms of application, the North America semiconductor silicon wafer market is segmented into consumer electronics, industrial, telecommunications, automotive, and others .The consumer electronics segment held the largest share of the North America semiconductor silicon wafer market share in 2023.

Based on node type, the North America semiconductor silicon wafer market is segmented into 180 nm, 130 nm, 90 nm, 65 nm, 45 nm, 22 nm, 14 nm, 7 nm, 5 nm and Below, and Others. The 7 nm segment held the largest share of the North America semiconductor silicon wafer market share in 2023.

Based on country, the North America semiconductor silicon wafer market is segmented into the US, Canada, and Mexico. The US segment held the largest share of North America semiconductor silicon wafer market in 2023.

Alfa Chemistry; Ferrotec Holdings Corporation; Fujimi Incorporated; GlobalWafers Co., Ltd; NANOCHEMAZONE; Nanografi Nano Technology; Okmetic; Shin-Etsu Chemical Co Ltd; Silicon Materials, Inc.; Siltronic AG; Sino-American Silicon Products Inc.; SK Siltron Co., Ltd; SUMCO CORPORATION; Wafer Works Corp; Wafer World Inc.; and WaferPro are the among leading companies operating in the North America semiconductor silicon wafer market.

The North America Semiconductor Silicon Wafer Market is valued at US$ 1,863.06 Million in 2023, it is projected to reach US$ 2,604.92 Million by 2031.

As per our report North America Semiconductor Silicon Wafer Market, the market size is valued at US$ 1,863.06 Million in 2023, projecting it to reach US$ 2,604.92 Million by 2031. This translates to a CAGR of approximately 4.3% during the forecast period.

The North America Semiconductor Silicon Wafer Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Semiconductor Silicon Wafer Market report:

The North America Semiconductor Silicon Wafer Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Semiconductor Silicon Wafer Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Semiconductor Silicon Wafer Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Semiconductor Silicon Wafer Market

Get Free Sample For North America Semiconductor Silicon Wafer Market