Analysis - By Type [Polyimide (PI), Polybenzoxazole (PBO), Benzocylobutene (BCB), and Others] and Application {Fan-Out Wafer Level Packaging (FOWLP) and 2.5D/3D IC Packaging [High Bandwidth Memory (HBM), Multi-Chip Integration, Package on Package (FOPOP), and Others]}

No. of Pages:

105

|

Report Code:

TIPRE00026110

|

Category:

Chemicals and Materials

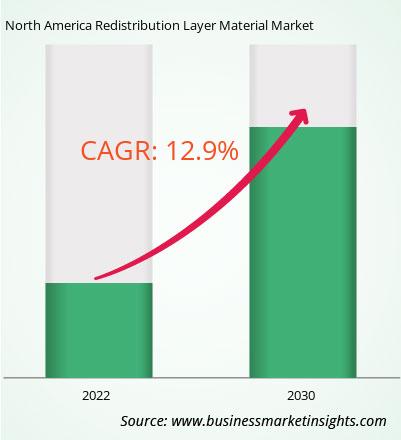

The North America redistribution layer material market was valued at US$ 22.34 million in 2022 and is expected to reach US$ 58.86 million by 2030; it is estimated to grow at a CAGR of 12.9% from 2022 to 2030.

Growing Focus on AI-based Equipment and Tools Drive North America Redistribution Layer Material Market

The growing demand for AI-based equipment and tools is significantly impacting the North America redistribution layer material market. The quest for more advanced AI capabilities necessitates the development of more compact and densely integrated hardware components. Redistribution layer (RDL) materials are fundamental in enabling the miniaturization of semiconductor packages, which is essential to accommodate the increasing complexity of AI devices. As AI systems become more sophisticated, the demand for smaller and more efficient components grows. In addition, AI applications are known for their voracious appetite for high-performance computing, which inherently generates substantial heat. Efficient thermal management is paramount to ensure the reliability and longevity of AI hardware. RDL materials play a crucial role by enhancing thermal conductivity and heat dissipation properties. As AI equipment becomes more powerful and heat-intensive, the demand for advanced RDL materials that can effectively address these thermal challenges escalates.

Scalability is also a critical consideration in the AI realm. As AI technology proliferates across industries, the ability to scale up hardware production efficiently is paramount. RDL materials simplify the integration of additional components or chips, streamlining the manufacturing process and enabling rapid scalability. This is especially valuable as AI-based tools and equipment become increasingly essential in finance, healthcare, and manufacturing sectors.

AI systems are intricate and typically involve multiple chips, sensors, and processors that must communicate seamlessly to process and analyze data in real-time. The demand for improved connectivity and signal integrity within AI hardware is ever-increasing. RDL materials are pivotal in facilitating high-speed data transmission and ensuring that various components in AI systems work harmoniously. As AI applications span diverse industries, from healthcare to autonomous vehicles, the need for RDL materials capable of maintaining robust connections becomes even more apparent. Moreover, the AI landscape is characterized by rapid evolution and customization. Different industries have unique requirements for AI hardware solutions, necessitating flexibility in design and configuration. RDL materials enable manufacturers to tailor semiconductor packages to meet these specific demands. This customization capability drives the adoption of RDL materials, empowering AI equipment manufacturers to create specialized hardware optimized for various applications. The rapid economic growth and industrial development across the globe also drive increased investment in AI technology. This growth includes the development of smart cities, autonomous vehicles, and industry 4.0 initiatives, all of which rely on AI-based tools and equipment. As these initiatives gain momentum, the demand for RDL materials as a foundation element in semiconductor packaging grows in tandem. Thus, the escalating demand for AI-based equipment and tools is fostering the growth of the North America redistribution layer material market.

North America Redistribution Layer Material Market Overview

North America has a wide presence of IT service providers, financial industries, and government agencies. The rapid pace of technological development and supporting government regulations made North America the most promising market for data centers. There are more than 2,500 data centers and 2,200 service providers in the US. With the increasing demand from customer for high-quality products and services, growing IT sector, and rising number of data centers, many companies are constantly innovating and developing new products to provide the best possible services to their customers.

The manufacturing industry plays a vital role in the growth of the North American economy. The availability of efficient infrastructure in developed nations has enabled manufacturing companies to explore the limits of science, technology, and commerce. Further, the US manufacturing sector is the second largest in the world, and manufacturers of the country hold 12% of total output in the economy. Moreover, the US manufacturing industry is expected to grow rapidly in the coming years due to several favorable factors, including increased productivity owing to the adoption of new technologies; decreased gas prices; and high labor costs in emerging markets. OEMs across all industries in North America are scaling up automation to compete with global manufacturing hubs such as China and Japan. This has led to the rapid developments in advanced semiconductors.

Also, the manufacturing industry in Mexico is witnessing significant growth due to government initiatives for attracting FDIs, as well as its proximity to the US and ability to achieve cost-competitiveness due to NAFTA. Moreover, the automotive industry in Mexico is experiencing a paradigm shift, with many huge automobile companies constructing their plants in the country. A few of the companies that recently opened their plants in the country include Kia Motors, Mercedes-Benz, Nissan, Audi, and General Motors, among others.

A few of the major manufacturing industries in North America include aerospace, automotive, telecommunications, and electronics, among others. Further, owing to a favorable economy, the spending capacities of individuals in North America are high, which has led to the exponential sales of smartphones, tablets, laptops, personal computers, wearables, and other consumer electronics devices. The consumer electronics industry is another major user of semiconductor-based products. All these industries are highly dependent on the semiconductor industry for effective performance. In September 2020, KLA, the US-based capital equipment company, improved its systems portfolio for advanced packaging by introducing new tools. The new tools consist of a Kronos 1190 wafer-level packaging inspection system, ICOS T3/T7 Series, and ICOS F160XP. The new systems allow the end users to improvise semiconductor device fabrication at a packaging stage. Similarly, in May 2021, Intel announced its plan to invest US$ 3.5 billion in the fabrication of advanced semiconductor packaging technologies.

All the above mentioned factors are anticipated to support the growth of the North America redistribution layer material market during 2022-2030.

North America Redistribution Layer Material Market Revenue and Forecast to 2030 (US$ Million)

North America Redistribution Layer Material Market Segmentation

The North America redistribution layer material market is segmented based on type, application, and country.

Based on type, the North America redistribution layer material market is segmented into polyimide (PI), polybenzoxazole (PBO), benzocylobutene (BCB), and others. The polyimide (PI) segment held the largest share in 2022.

By application, the North America redistribution layer material market is segmented into fan-out wafer level packaging (FOWLP) and 2.5D/3D IC packaging. The 2.5D/3D IC packaging segment held a larger share in 2022. The 2.5D/3D IC packaging is further subsegmented into high bandwidth memory (HBM), multi-chip integration, package on package (FOPOP), and others.

Based on country, the North America redistribution layer material market is segmented into US, Canada, and Mexico. The US dominated the North America redistribution layer material market in 2022.

SK Hynix Inc, Samsung Electronics Co Ltd, Infineon Technologies AG, DuPont de Nemours Inc, FUJIFILM Holdings Corp, Amkor Technology Inc, ASE Technology Holding Co Ltd, NXP Semiconductors NV, JCET Group Co Ltd, and Shin-Etsu Chemical Co Ltd are some of the leading companies operating in the North America redistribution layer material market.

North America Redistribution Layer Material Strategic Insights

Strategic insights for the North America Redistribution Layer Material provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

Get more information on this report

North America Redistribution Layer Material Report Scope

Report Attribute

Details

Market size in 2022

US$ 22.34 Million

Market Size by 2030

US$ 58.86 Million

Global CAGR (2022 - 2030)

12.9%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Type

Polyimide

Polybenzoxazole

Benzocylobutene

By Application

Fan-Out Wafer Level Packaging

2.5D/3D IC Packaging

Regions and Countries Covered

North America

US

Canada

Mexico

Market leaders and key company profiles

SK Hynix Inc

Samsung Electronics Co Ltd

Infineon Technologies AG

DuPont de Nemours Inc

FUJIFILM Holdings Corp

Amkor Technology Inc

ASE Technology Holding Co Ltd

NXP Semiconductors NV

JCET Group Co Ltd

Shin-Etsu Chemical Co Ltd

Get more information on this report

North America Redistribution Layer Material Regional Insights

The geographic scope of the North America Redistribution Layer Material refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - North America Redistribution Layer Material Market

1. SK Hynix Inc

2. Samsung Electronics Co Ltd

3. Infineon Technologies AG

4. DuPont de Nemours Inc

5. FUJIFILM Holdings Corp

6. Amkor Technology Inc

7. ASE Technology Holding Co Ltd

8. NXP Semiconductors NV

9. JCET Group Co Ltd

10. Shin-Etsu Chemical Co Ltd

Frequently Asked Questions

How big is the North America Redistribution Layer Material Market?

The North America Redistribution Layer Material Market is valued at US$ 22.34 Million in 2022, it is projected to reach US$ 58.86 Million by 2030.

What is the CAGR for North America Redistribution Layer Material Market by (2022 - 2030)?

As per our report North America Redistribution Layer Material Market, the market size is valued at US$ 22.34 Million in 2022, projecting it to reach US$ 58.86 Million by 2030. This translates to a CAGR of approximately 12.9% during the forecast period.

What segments are covered in this report?

The North America Redistribution Layer Material Market report typically cover these key segments-

Type (Polyimide, Polybenzoxazole, Benzocylobutene)

Application (Fan-Out Wafer Level Packaging, 2.5D/3D IC Packaging)

What is the historic period, base year, and forecast period taken for North America Redistribution Layer Material Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Redistribution Layer Material Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2030

Who are the major players in North America Redistribution Layer Material Market?

The North America Redistribution Layer Material Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

SK Hynix Inc

Samsung Electronics Co Ltd

Infineon Technologies AG

DuPont de Nemours Inc

FUJIFILM Holdings Corp

Amkor Technology Inc

ASE Technology Holding Co Ltd

NXP Semiconductors NV

JCET Group Co Ltd

Shin-Etsu Chemical Co Ltd

Who should buy this report?

The North America Redistribution Layer Material Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the North America Redistribution Layer Material Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For North America Redistribution Layer Material Market

1. Complete the form

2. Check your inbox (and spam/junk folder)

3. Your Personal Data is Secure with us

GDPR + CCPA Compliant

Personal & transactional information is kept safe from unauthorized use.

WHAT'S INCLUDED IN FULL REPORT : Market Dynamics,

Competitive Analysis and Assessment, Define Business Strategies, Market Outlook and

Trends, Market Size and Share Analysis, Growth Driving Factors, Future Commercial

Potential, Identify Regional Growth Engines

Get Free Sample For North America Redistribution Layer Material Market

Get Free Sample For North America Redistribution Layer Material Market