North America Lung Cancer Screening Market

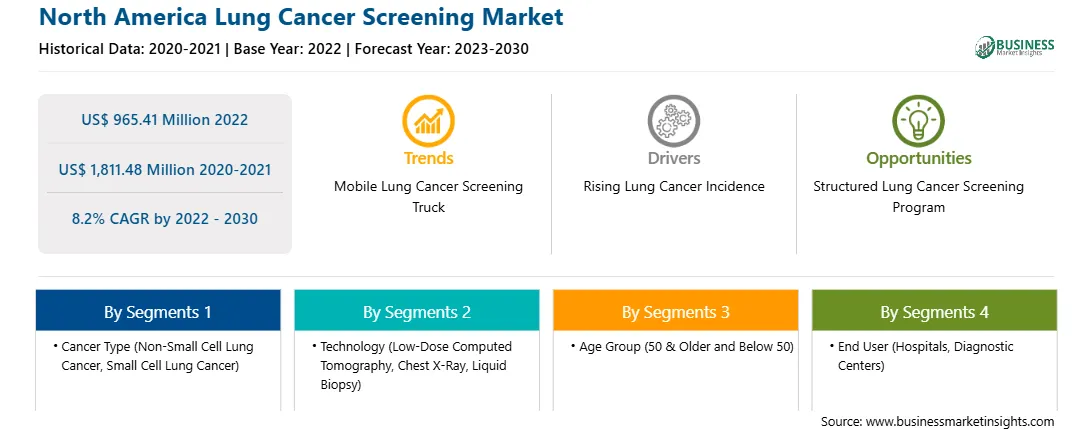

Lung cancer is among the main causes of mortality across the world. Lung cancer screening is a critical component of cancer prevention approaches. The prognosis for lung cancer patients is better when the disease is diagnosed early, so people at high risk of lung cancer are encouraged to undergo routine testing to detect the formation of cancerous growth in their lungs. According to estimates by the American Cancer Society for lung cancer in the US for 2023, about 238,340 new lung cancer cases were registered; of these, 120,790 in women and 117,550 in men were reported. Thus, the rising incidence of lung cancer worldwide is contributing to the initiation of lung cancer screening programs, which is, in turn, driving the market growth.

The North America, Lung Cancer Screening Market is segmented into the US, Canada, and Mexico. The regional growth is attributed to various factors, such as the increasing incidence of lung cancer and awareness of side effects of cigarette smoking among people. Also, rising government support for screening has led to the further growth of the market.

In North America, the US holds a significant share of the North America Lung Cancer Screening Market. The market growth in this country is primarily driven by the increasing incidence of lung cancer and government initiatives. Lung cancer is the second most common cancer in both men and women in the US. As per the American Cancer Society, Inc., as of 2023, approximately 238,340 adults (117,550 men and 120,790 women) in the US have been diagnosed with lung cancer, and ~127,070 (67,160 in men and 59,910 in women) have succumbed to death due to the disease. Lung Cancer accounts for 1 in 5 of all cancer death, making it a leading cause of cancer death in the US. These statistics include both small cell lung cancer and NSCLC. NSCLC is the most common type of lung cancer, accounting for 81% of all lung cancer diagnoses. For all types of lung cancer in the US, the 5-year relative survival rate is 23%, and for NSCLC, the 5-year relative survival rate for men and women is 23% and 33%, respectively. In the US, screening for lung cancer is recommended with a test called a low-dose helical or spiral computed tomography (CT or CAT) scan. Preventive Services Task Force (USPSTF) recommends that people aged 50–80, with a history of smoking 20 pack years or more, or who have quit within the past 15 years should go through screening for lung cancer with low-dose CT scans each year. As per the report published in the whitehouse.gov, the official website of the White House, managed by the Office of Digital Strategy in May 2023, the Association of Community Cancer Centers (ACCC) and AstraZeneca are entering into a partnership to develop and implement person-centered and sustainable approaches to increase lung cancer screening in rural America through the “Rural Appalachian Lung Cancer Screening Initiative.” The cancer mortality rate in the Appalachian region, including all of West Virginia and parts of 12 other states, is 10% higher than that in the rest of the US. The aim of this initiative is to double the five-year survival rate for lung cancer. Such initiatives are contributing to the North America Lung Cancer Screening Market growth in the US.

Strategic insights for the North America Lung Cancer Screening provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market. The geographic scope of the North America Lung Cancer Screening refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas. Get more information on this report

Get more information on this report North America Lung Cancer Screening Strategic Insights

Get more information on this report

Get more information on this report North America Lung Cancer Screening Report Scope

Report Attribute

Details

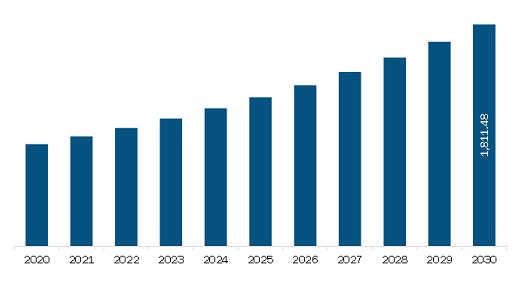

Market size in 2022

US$ 965.41 Million

Market Size by 2030

US$ 1,811.48 Million

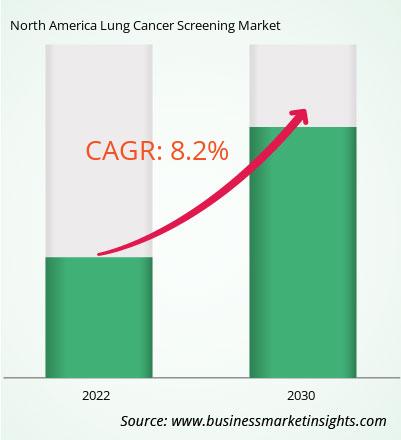

Global CAGR (2022 - 2030)

8.2%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Cancer Type

By Technology

By Age Group

By End User

Regions and Countries Covered

North America

Market leaders and key company profiles

Get more information on this report North America Lung Cancer Screening Regional Insights

Get more information on this report

Get more information on this report

North America Lung Cancer Screening Market Segmentation

The North America lung cancer screening market is segmented into cancer type, technology, age group, end user, and country.

Based on cancer type, the North America lung cancer screening market is segmented into non–small cell lung cancer (NSCLC), and small cell lung cancer. The non–small cell lung cancer (NSCLC) segment held a larger share of the North America lung cancer screening market in 2022.

Based on technology, the North America lung cancer screening market is segmented into chest X-ray, low dose computed tomography (LDCT), liquid biopsy, and others. Low dose computed tomography (LDCT) segment held the largest share of the North America lung cancer screening market in 2022.

Based on age group, the North America lung cancer screening market is segmented into 50 and older, and below 50. 50 and older segment held the larger share of the North America lung cancer screening market in 2022.

Based on end user, the North America lung cancer screening market is segmented into hospital, diagnostic centre, and others. Hospital segment held the largest share of the North America lung cancer screening market in 2022.

Based on country, the North America Lung Cancer Screening Market is segmented into the US, Canada, and Mexico. The US dominated the North America lung cancer screening market in 2022.

Siemens AG, Koninklijke Philips NV, Canon Inc, Medtronic, GE HealthCare, Nuance Communications Inc, LungLife AI, Inc, Intelerad Medical Systems, bioAffinity Technologies, Inc, and CSV Health are some of the leading companies operating in the North America lung cancer screening market.

The North America Lung Cancer Screening Market is valued at US$ 965.41 Million in 2022, it is projected to reach US$ 1,811.48 Million by 2030.

As per our report North America Lung Cancer Screening Market, the market size is valued at US$ 965.41 Million in 2022, projecting it to reach US$ 1,811.48 Million by 2030. This translates to a CAGR of approximately 8.2% during the forecast period.

The North America Lung Cancer Screening Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Lung Cancer Screening Market report:

The North America Lung Cancer Screening Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Lung Cancer Screening Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Lung Cancer Screening Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Lung Cancer Screening Market

Get Free Sample For North America Lung Cancer Screening Market