North America Industrial Starch Market

Traditionally, companies use polystyrene materials, which are generally extruded, or injection molded for packaging. Polystyrene packaging is nonrecyclable. Therefore, increasing awareness among companies about the environmental impact of polystyrene has encouraged companies to use biodegradable and recyclable packaging materials. Starch-based materials have the potential to be used as biodegradable food packaging materials that reduce environmental pollution. The usability of starch-based biodegradable materials can be improved or extended by adding other additives or biopolymers and using innovative preparation techniques. Additionally, the starch adhesive is most widely used in the corrugated board industry because of its abundant supply, low cost, renewability, biodegradable properties, and ease of chemical modifications. As participants in the packaging industry are becoming increasingly aware of the importance of shifting toward sustainable and greener options such as corn starch, the packaging is being recognized as more than just a public relations alternative. This significant growth of the e-commerce sector and the increasing adoption of eco-friendly packaging materials are expected to boost the demand for industrial starch across North America.

Vendors in the industrial starch market can attract new customers and expand their footprints in emerging markets by offering products with new features and technologies. This factor is likely to drive the market at a good CAGR during the forecast period.

Strategic insights for the North America Industrial Starch provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

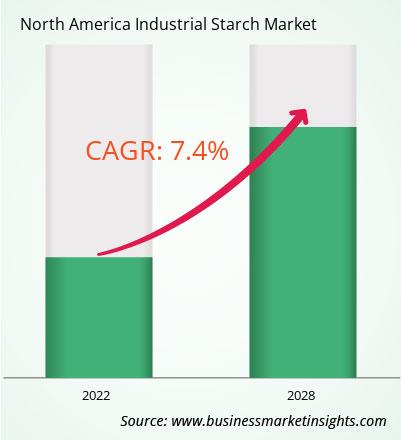

| Market size in 2022 | US$ 13,537.63 Million |

| Market Size by 2028 | US$ 20,752.10 Million |

| Global CAGR (2022 - 2028) | 7.4% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Flavor

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

The geographic scope of the North America Industrial Starch refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The North America industrial starch market is segmented on the basis of type, source, application, and country. Based on type, the market is bifurcated into native starch and starch derivatives and sweeteners. The starch derivatives and sweeteners segment dominated the market in 2022 and is expected to register a higher CAGR during the forecast period. Based on source, the market is segmented into potato, corn, wheat, cassava, and others. The wheat segment dominated the market in 2022, and the corn segment is expected to register the highest CAGR during the forecast period. Based on application, the North America industrial starch market is segmented into food and beverages, pulp and paper, animal feed, pharmaceuticals, and others. The food and beverages segment dominated the market in 2022, and the pulp and paper segment is expected to register the highest CAGR during the forecast period. Based on country, the North America industrial starch market is segmented into the US, Canada, and Mexico.

ADM; AGRANA Beteiligungs AG; Cargill, Incorporated; Grain Processing Corporation; Ingredion Incorporated; Roquette Frères; Royal Cosun; Tate & Lyle PLC; and Tereos Group are among the leading companies operating in the North America industrial starch market.

The North America Industrial Starch Market is valued at US$ 13,537.63 Million in 2022, it is projected to reach US$ 20,752.10 Million by 2028.

As per our report North America Industrial Starch Market, the market size is valued at US$ 13,537.63 Million in 2022, projecting it to reach US$ 20,752.10 Million by 2028. This translates to a CAGR of approximately 7.4% during the forecast period.

The North America Industrial Starch Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Industrial Starch Market report:

The North America Industrial Starch Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Industrial Starch Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Industrial Starch Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Industrial Starch Market

Get Free Sample For North America Industrial Starch Market