North America Industrial Insulation Market

Insulation materials provide resistance to heat flow and it also helps in lowering heating and cooling costs. Strict regulations for the mandatory use of insulation materials for energy saving purposes are the major factor contributing to the growth of the industrial insulation market. Energy saving regulations and the need for insulation materials in end-use industries such as oil and gas, chemical and petrochemical, food and beverage are driving the market growth. Additionally, standards established by various associations apply to the design of equipment in the industry, to overhaul and implement to boost the growth of the industrial insulation market across the region.

Market Overview

The North America industrial insulation market is segmented into the US, Canada, and Mexico. The market in the region is driven by highly developed industrial and power generation sector. Industrial Insulation plays an important role in nuclear power plants, fossil fuel power plants, hydroelectric power plants, solar power plants, coal-fired power plants and wind power towers. It helps maintain the temperatures of boilers that generate steam. Pipes in these facilities require insulation to maintain temperatures. In recent years, renewable electricity generation from sources other than hydropower has steadily increased in the US due to the increasing to wind and solar generating capacities. According to the US Energy Information Administration, wind energy's share of total utility-scale electricity generating capacity in the US grew from 0.2% in 1990 to about 12% in 2021, and its share of total annual utility-scale electricity generation grew from less than 1% in 1990 to about 9% in 2021. In addition, solar energy's share of total utility-scale electricity generation in the US in 2021 was about 2.8%, up from less than 0.1% in 1990. The increasing electricity generation mainly drives the demand for industrial insulation products in the region. In the chemical & petrochemical industry, many of the products created within the facilities are potentially hazardous at some stage during their manufacture, production, and transportation. The manufacturing process involves high temperatures, high pressure, and chemical reactions. In various chemical plants, different processes contain thermal challenges that the industrial insulation industry addresses by using various insulation materials available in the market. In the US, the chemicals industry is a keystone of the country’s economy. The US is one of the top chemical producers in the world, accounting for the significant share of the world production. In Canada, the chemical industry has played an important role in the country’s economy. The industry in the country focuses mainly on crude petroleum and natural gas processing. Hence, the strong presence of the chemical & petrochemical industry in the region propels the demand for industrial insulation products. Further, in the food industry, thermal insulation products are used for pipework, boilers, fryers, storage tanks, and steam distribution systems. Therefore, the increasing use of insulation products in the food & beverage industry bolsters the industrial insulation market growth in North America.

Strategic insights for the North America Industrial Insulation provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market. The geographic scope of the North America Industrial Insulation refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas. Get more information on this report

Get more information on this report North America Industrial Insulation Strategic Insights

Get more information on this report

Get more information on this report North America Industrial Insulation Report Scope

Report Attribute

Details

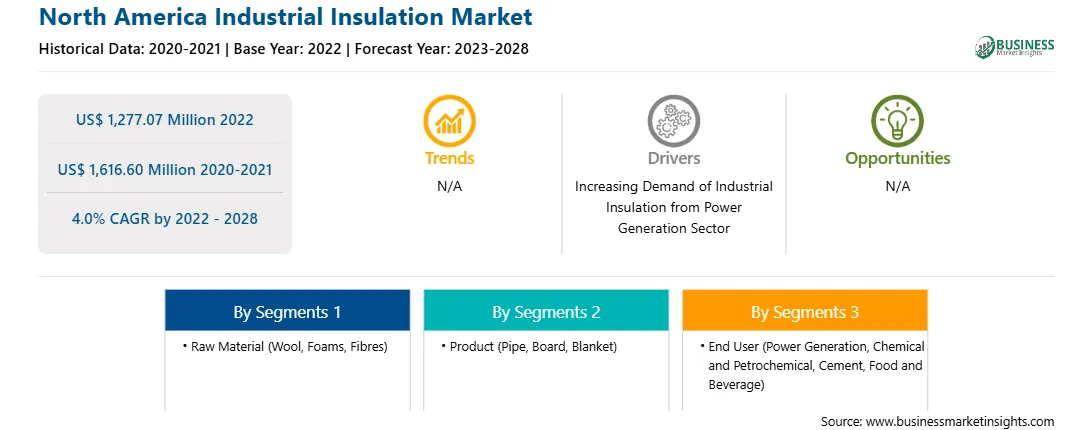

Market size in 2022

US$ 1,277.07 Million

Market Size by 2028

US$ 1,616.60 Million

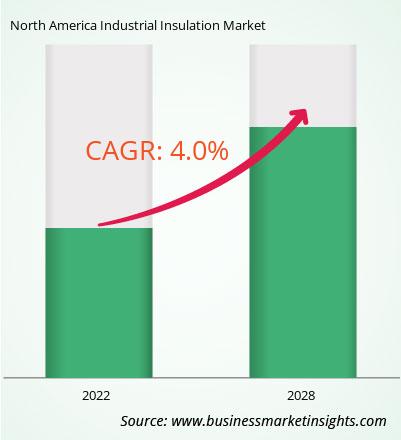

Global CAGR (2022 - 2028)

4.0%

Historical Data

2020-2021

Forecast period

2023-2028

Segments Covered

By Raw Material

By Product

By End User

Regions and Countries Covered

North America

Market leaders and key company profiles

Get more information on this report North America Industrial Insulation Regional Insights

Get more information on this report

Get more information on this report

North America Industrial Insulation Market Segmentation

The North America industrial insulation market is segmented based on raw material, product, end user, and country.

Based on raw material, the North America industrial insulation market is segmented into wool, foams, fibres, and others. The foams segment held the largest market share in 2022.

Based on product, the North America industrial insulation market is segmented into pipe, board, blanket, and others. The pipe segment held the largest market share in 2022.

Based on end user, the North America industrial insulation market is segmented into power generation, chemical and petrochemical, cement, food and beverage, and others. The power generation segment held the largest market share in 2022.

Based on country, the North America industrial insulation market has been categorized into the US, Canada, and Mexico. Our regional analysis states that the US dominated the market share in 2022.

Aspen Aerogels Inc., Cabot Corporation, Johns Manville, Kingspan Group, Knauf Insulation, McAllister Mills Inc., Nichias Corporation, ROCKWOOL A/S, Saint Gobain S.A., and Thomas Group are the leading companies operating in the North America industrial insulation market.

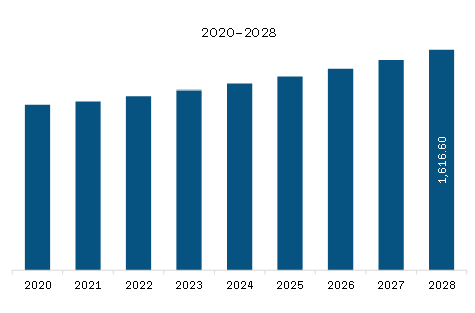

The North America Industrial Insulation Market is valued at US$ 1,277.07 Million in 2022, it is projected to reach US$ 1,616.60 Million by 2028.

As per our report North America Industrial Insulation Market, the market size is valued at US$ 1,277.07 Million in 2022, projecting it to reach US$ 1,616.60 Million by 2028. This translates to a CAGR of approximately 4.0% during the forecast period.

The North America Industrial Insulation Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Industrial Insulation Market report:

The North America Industrial Insulation Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Industrial Insulation Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Industrial Insulation Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Industrial Insulation Market

Get Free Sample For North America Industrial Insulation Market