North America In-Vitro Diagnostics Market

Point-of-care testing (POCT) is a pivotal opportunity in the in vitro diagnostics market, revolutionizing healthcare delivery with its potable and rapid diagnostic capabilities. These tests, conducted at or near the patient’s location, offer immediate results, enabling timely clinical decision-making. Several factors drive the growth of POCT.

Firstly, the demand for convenient and swift diagnostic solutions in healthcare settings, such as emergency rooms, clinics, and home care, propels the expansion of POCT. Secondly, technological advancements have led to the development of compact and user-friendly POCT devices.

Moreover, the COVID-19 pandemic underscored the significance of rapid and accessible diagnostics. The pandemic accelerated the deployment and utilization of point-of-care COVID-19 tests, showcasing the relevance and potential of POCT in managing infectious diseases on a global scale. This experience accelerated research and development on POCT, further driving innovation and investment in portable testing solutions.

IVDs that are used in the diagnosis of infectious diseases include immunoassays, and molecular assays. Diagnostics companies also focus on making rapid advancements in their offerings to manage COVID-19. Further, regulatory authorities introduced temporary amendments or modifications to their standards, which favored the launches of new IVDs during the pandemic. The demand for molecular diagnostics and immunoassays surged due to these government initiatives. Thus, the COVID-19 pandemic has benefitted the in-vitro diagnostics market due to the rising demand for point-of-care (POC) diagnostics and laboratory testing procedures.

North America region includes the US, Canada, and Mexico. It holds the largest share of the in-vitro diagnostics market by geography. All three countries in the region are witnessing considerable demand for in-vitro diagnostics. Certain factors, such as the increasing prevalence of chronic & infectious diseases, focus on efficient disease diagnosis, and a higher need for advanced healthcare systems are boosting the adoption of in-vitro diagnostics in the region. The US held the largest share of the North America in-vitro diagnostics market. Chronic diseases such as cancer and cardiovascular diseases are the major causes of disability and death in the US. Per the National Center for Chronic Disease Prevention and Health Promotion, 6 in 10 people in the country have at least one chronic disease. According to the Centers for Disease Control and Prevention (CDC), in 2021, ~18.2 million adults aged 20 and above had coronary artery disease (CAD) in the US. Heart disease is the leading cause of death among people in the country. Additionally, the American Hospital Association estimates ~133 million people have at least one chronic disease, and that number is expected to reach 170 million by 2030. The high incidence of chronic diseases results in a huge demand for diagnostic procedures, which, in turn, drives the in-vitro diagnostics market in the US. Growing emphasis on preventive care coupled with enhanced access to healthcare facilities would further boost the market growth in the coming years.

With the exponentially rising need for in-vitro diagnostics tools with the growing patient pool, the market players focus on developing advanced diagnostic systems enabling rapid examinations. For instance, in February 2019, Grail, a US-based player in diagnostic services, received financial aid of US$ 1.5 billion from Microsoft and Amazon with an aim to develop new technologies for rapid cancer detection. Additionally, extensive technological advancements due to developed healthcare infrastructure and rising expenditure are generating lucrative opportunities for the growth of the in-vitro diagnostics market in the country. For instance, in July 2019, Sysmex America, Inc., one of the prominent players in the in-vitro diagnostics market, showcased its new integrated in-vitro diagnostic machine named PS-10 at the 71st AACC Annual Scientific Meeting & Clinical Lab Expo organized in Anaheim, California. The machine is designed to perform complex laboratory tests, routine cytometry, and hematology assessments. Similarly, in May 2020, Bio-Rad Laboratories Inc. received Emergency Use Authorization (EUA) for its SARS-CoV-2 Droplet Digital PCR (ddPCR) test kit from the US Food and Drug Administration (FDA). The SARS-CoV-2 ddPCR test runs on Bio-Rad's QX200 and QXDx ddPCR systems.

North America In-Vitro Diagnostics Market Segmentation

The North America in-vitro diagnostics market is segmented into product & services, technology, application, end user, and country.

Based on product & services, the North America in-vitro diagnostics market is segmented into reagents & kits, instruments, and software & services. The reagents & kits segment held the largest share of the North America in-vitro diagnostics market in 2022.

Based on technology, the North America in-vitro diagnostics market is segmented into immunoassay/ immunochemistry, clinical chemistry, molecular diagnostics, microbiology, blood glucose self-monitoring, coagulation & hemostasis, hematology, urinalysis, and others. The immunoassay/ immunochemistry segment held the largest share of the North America in-vitro diagnostics market in 2022.

Based on application, the North America in-vitro diagnostics market is segmented into infectious diseases, diabetes, oncology, cardiology, autoimmune diseases, nephrology, and others. The infectious diseases segment held the largest share of the North America in-vitro diagnostics market in 2022.

Based on end user, the North America in-vitro diagnostics market is segmented into hospitals, laboratories, homecare, and others. The hospitals segment held the largest share of the North America in-vitro diagnostics market in 2022.

Based on country, the North America in-vitro diagnostics market is segmented into the US, Canada, and Mexico. The US dominated the North America in-vitro diagnostics market in 2022.

Abbott Laboratories, Becton Dickinson and Co, bioMerieux SA, Bio-Rad Laboratories Inc, Danaher Corp, F. Hoffmann-La Roche Ltd, Qiagen NV, Siemens AG, Sysmex Corp, and Thermo Fisher Scientific Inc are some of the leading companies operating in the North America in-vitro diagnostics market.

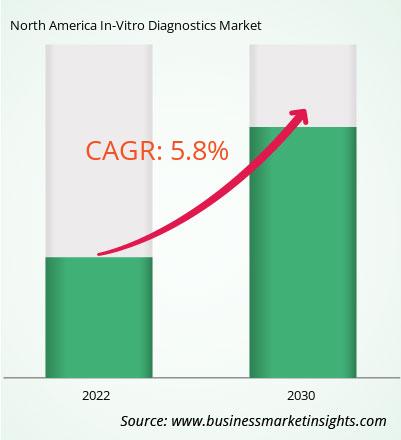

The North America In-Vitro Diagnostics Market is valued at US$ 21,207.07 Million in 2022, it is projected to reach US$ 33,183.41 Million by 2030.

As per our report North America In-Vitro Diagnostics Market, the market size is valued at US$ 21,207.07 Million in 2022, projecting it to reach US$ 33,183.41 Million by 2030. This translates to a CAGR of approximately 5.8% during the forecast period.

The North America In-Vitro Diagnostics Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America In-Vitro Diagnostics Market report:

The North America In-Vitro Diagnostics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America In-Vitro Diagnostics Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America In-Vitro Diagnostics Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

UK+442030260021, US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America In-Vitro Diagnostics Market

Get Free Sample For North America In-Vitro Diagnostics Market