North America Fill Finish Manufacturing Market

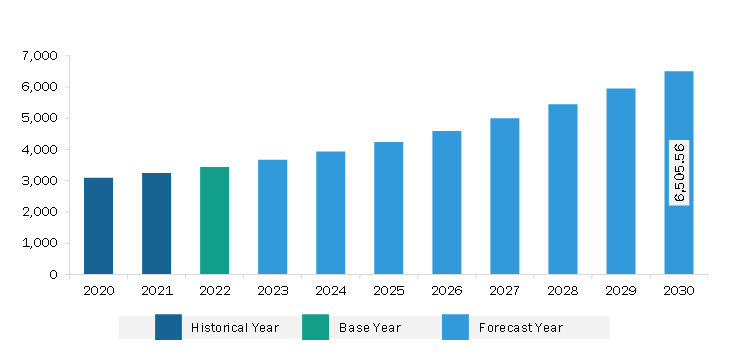

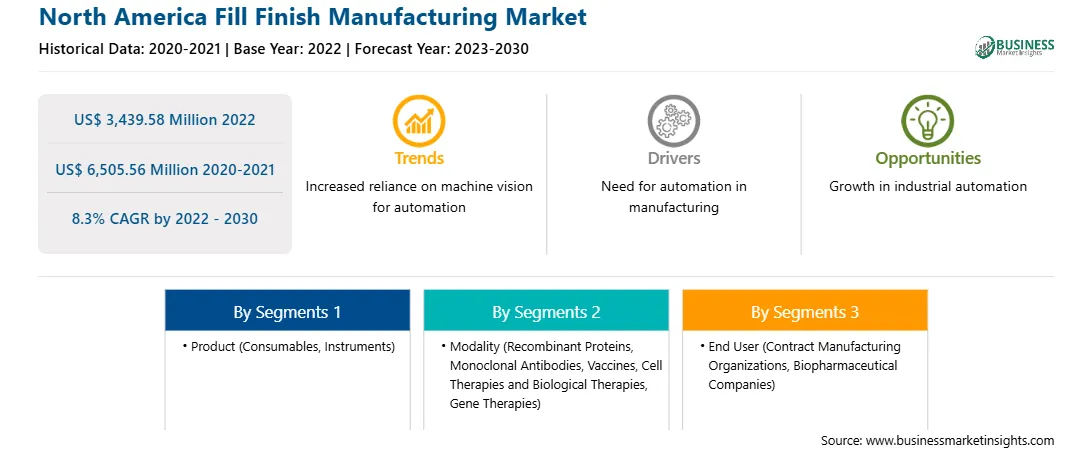

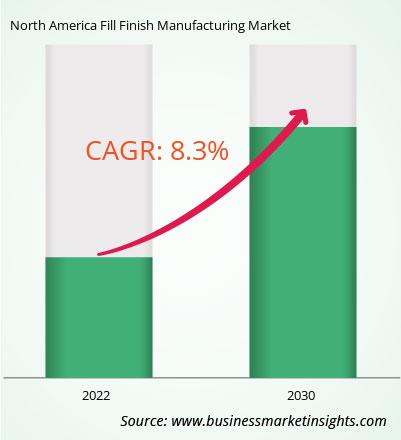

The North America fill finish manufacturing market was valued at US$ 3,439.58 million in 2022 and is expected to reach US$ 6,505.56 million by 2030; it is estimated to grow at a CAGR of 8.3% from 2022 to 2030.

Parenteral administration is one of the most prominent routes chosen to stimulate immediate immune response and ensure the complete bioavailability of pharmaceutical products. A steady rise in the development and market availability of parenteral drugs has propelled the demand for advanced, cost-effective drug delivery devices that promise ease of administration. The benefits of prefilled syringes over traditional delivery systems include easy administration, improved safety, accurate dosing, and reduced contamination risks. Among drug delivery devices, prefilled syringes represent one of the fastest-growing primary packaging formats, which are designed for dose administration. In the past ten years, there has been an evident increase in the development of parenteral drugs (especially with the introduction of several classes of biologics), which has resulted in approximately three-fold increase in the consumption of prefilled syringes. The sustained preference for the prefilled syringes is attributed to the safety and ease of use of these products. Recent variants are designed with provisions to reduce errors in dosing, risk of occlusions, leakage of fluids (i.e., extravasation), and inflammation of veins (phlebitis). Owing to the benefits mentioned above, several injectable drugs—Humira, Enbrel, Avastin, PREVNAR 13, ALPROLIX, and Benefix, among others—diluents and other products requiring parenteral administration are packaged in prefilled syringes.

Over the past seven years, ~90 drugs have been approved in the prefilled syringe packaging form across different geographies, including North America, Europe, and Asia Pacific. Several drugs in the clinical stages of drug development are being evaluated in combination with prefilled syringes.

The loading of sterile drugs into prefilled syringes is considered one of the most crucial steps in the pharmaceutical production process. Proper fill-finish operations are necessarily carried out under aseptic conditions to maintain pharmacological efficacy and quality and to ensure the safety of end users. The prefilled syringe filling is a complex operation as it requires extremely close monitoring of both the syringe fill volume and the headspace between the liquid filled in the syringe and the bottom of the plunger. In addition, the rise in complexity of small molecule APIs and the increasing diversity of biological drugs contribute to the demand for advanced aseptic fill finish operations.

Companies, including small enterprises and large businesses, outsource their respective fill finish operations to contract service providers. Per the 10th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production, manufacturers of biological have been observed to outsource more than 30% of their fill finish operations. With the rise in the demand for prefilled syringes and the growing complexity of fill finish processes, outsourcing these operations is likely to increase in the future. Over 100 companies across the globe are providing fill finish services for prefilled syringe manufacturers. To cater to the growing demand of pharmaceutical products, service providers are actively investing in expanding their existing infrastructure and capabilities; they have also expanded their clientele through service agreements over the past few years. As injectables account for ~55% of drug candidates in the global R&D pipeline, the businesses of prefilled syringe manufacturers and associated service providers are also growing. Due to the emergence of the COVID-19 crisis, vaccine development initiatives have increased across the globe, which significantly boosted the demand for prefilled syringes. Thus, the rising adoption of prefilled syringes for parenteral administration drives the fill finish manufacturing market.

The fill finish manufacturing market in the US is anticipated to be the largest and fastest-growing market in the world. Several factors such as extensive research and development activities and advanced manufacturing of innovative biopharmaceutical and pharmaceutical products lead to the growth of the market. The other leading factor for market growth is sustained diversity and large-scale supply of biopharmaceutical and pharmaceutical products across the globe.

The biopharmaceutical industry is among the largest revenue-generating sector in the country. In 2023, it generated more than 1.3 million jobs in the US. Thus, the growth in the biopharmaceutical industry has assisted in maintaining the total economic balance in the country substantially. It generates ~US$ 550 million in revenue annually. Therefore, it is expected that the rise in research and product development will increase the demand for lyophilization services in the US.

Strategic insights for the North America Fill Finish Manufacturing provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market. The geographic scope of the North America Fill Finish Manufacturing refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas. Get more information on this report

Get more information on this report North America Fill Finish Manufacturing Strategic Insights

Get more information on this report

Get more information on this report North America Fill Finish Manufacturing Report Scope

Report Attribute

Details

Market size in 2022

US$ 3,439.58 Million

Market Size by 2030

US$ 6,505.56 Million

Global CAGR (2022 - 2030)

8.3%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Product

By Modality

By End User

Regions and Countries Covered

North America

Market leaders and key company profiles

Get more information on this report North America Fill Finish Manufacturing Regional Insights

Get more information on this report

Get more information on this report

The North America fill finish manufacturing market is segmented based on product, modality, end user, and country. Based on product, the North America fill finish manufacturing market is bifurcated into consumables and instruments. The consumables segment held a larger market share in 2022. Furthermore, the consumables is sub segmented into prefilled syringes, glass vial/plastic vials, cartridges, and others.

In terms of modality, the North America fill finish manufacturing market is segmented into recombinant proteins, monoclonal antibodies, vaccines, cell therapies and biological therapies, gene therapies, and others. The vaccines segment held the largest market share in 2022.

By end user, the North America fill finish manufacturing market is segmented into contract manufacturing organizations, biopharmaceutical companies, and others. The contract manufacturing organizations segment held the largest market share in 2022.

Based on country, the North America fill finish manufacturing market is segmented into the US, Canada, and Mexico. The US dominated the North America fill finish manufacturing market share in 2022.

Becton Dickinson and Co, Gerresheimer AG, Groninger and Co GmbH, IMA Industria Macchine Automatiche SpA, Maquinaria Industrial Dara SL, Nipro Medical Europe NV, NNE AS, Optima Packaging Group Gmbh, Schott AG, SGD SA, Stevanato Group SpA, Syntegon Technology GmbH, and West Pharmaceutical Services Inc are some of the leading players operating in the North America fill finish manufacturing market.

The North America Fill Finish Manufacturing Market is valued at US$ 3,439.58 Million in 2022, it is projected to reach US$ 6,505.56 Million by 2030.

As per our report North America Fill Finish Manufacturing Market, the market size is valued at US$ 3,439.58 Million in 2022, projecting it to reach US$ 6,505.56 Million by 2030. This translates to a CAGR of approximately 8.3% during the forecast period.

The North America Fill Finish Manufacturing Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Fill Finish Manufacturing Market report:

The North America Fill Finish Manufacturing Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Fill Finish Manufacturing Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Fill Finish Manufacturing Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Fill Finish Manufacturing Market

Get Free Sample For North America Fill Finish Manufacturing Market