North America Automotive Radar Market

The North America automotive radar market is driven by various factors such as increasing government regulations concerning vehicle safety, rising adoption of premium vehicles, as well as a growing number of radars used in a vehicle. Moreover, the rising production and adoption of electric vehicles (EV) are further expected to support the growth of the North America automotive radar market. It is anticipated that in the coming few years, autonomous driving will be the growing trend. To attain this, several vision technologies have increased intending to deliver functionality as well as safety to the vehicle's drivers and passengers. Radar systems are considered the most established and trusted technologies among the automotive industry's various vision technologies. Presently, several vehicle manufacturers provide 'level 3' automation wherein drivers are on standby for a certain time. These vehicles are integrated with nearly five radar systems, including SSR and LLR, for applications such as emergency braking or Adaptive Cruise Control. Also, growing road accidents is going to bolster the demand for automotive radar in the coming years, which is further anticipated to drive the North America automotive radar market.

The ongoing COVID-19 outbreak has severely impacted the North America region. North America is one of the most important regions for the adoption and growth of new technologies owing to favorable government policies to boost innovation, the presence of a high-tech companies, and high purchasing power, especially in developed countries such as the US and Canada. The US is the worst-hit country in North America, with thousands of infected individuals facing severe health conditions across the country. The North American region is greatly influenced by the US's strong presence owing to its considerable penetration of passenger vehicles per capita and large presence of automobile manufacturing capabilities in the region. Though the US witnessed a notable surge in the number of COVID-19 cases, the lack of stringent government measures and restrictions slightly impacted the overall automotive industry; hence the market saw a moderate impact from the pandemic. However, the ongoing US and China trade war did influence the availability of materials and components for various automotive OEMs following the pandemic. Whereas Mexico and Canada witnessed a decline in the demand for automotive sales and therefore witnessed a notable decline in their overall market growth for various automotive components, including radars. However, the impact of COVID-19 is short-term and is likely to decrease by 2021.

Strategic insights for the North America Automotive Radar provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2019 | US$ 982.2 Million |

| Market Size by 2027 | US$ 2,304.9 Million |

| Global CAGR (2020 - 2027) | 15.1% |

| Historical Data | 2017-2018 |

| Forecast period | 2020-2027 |

| Segments Covered |

By Range

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

The geographic scope of the North America Automotive Radar refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

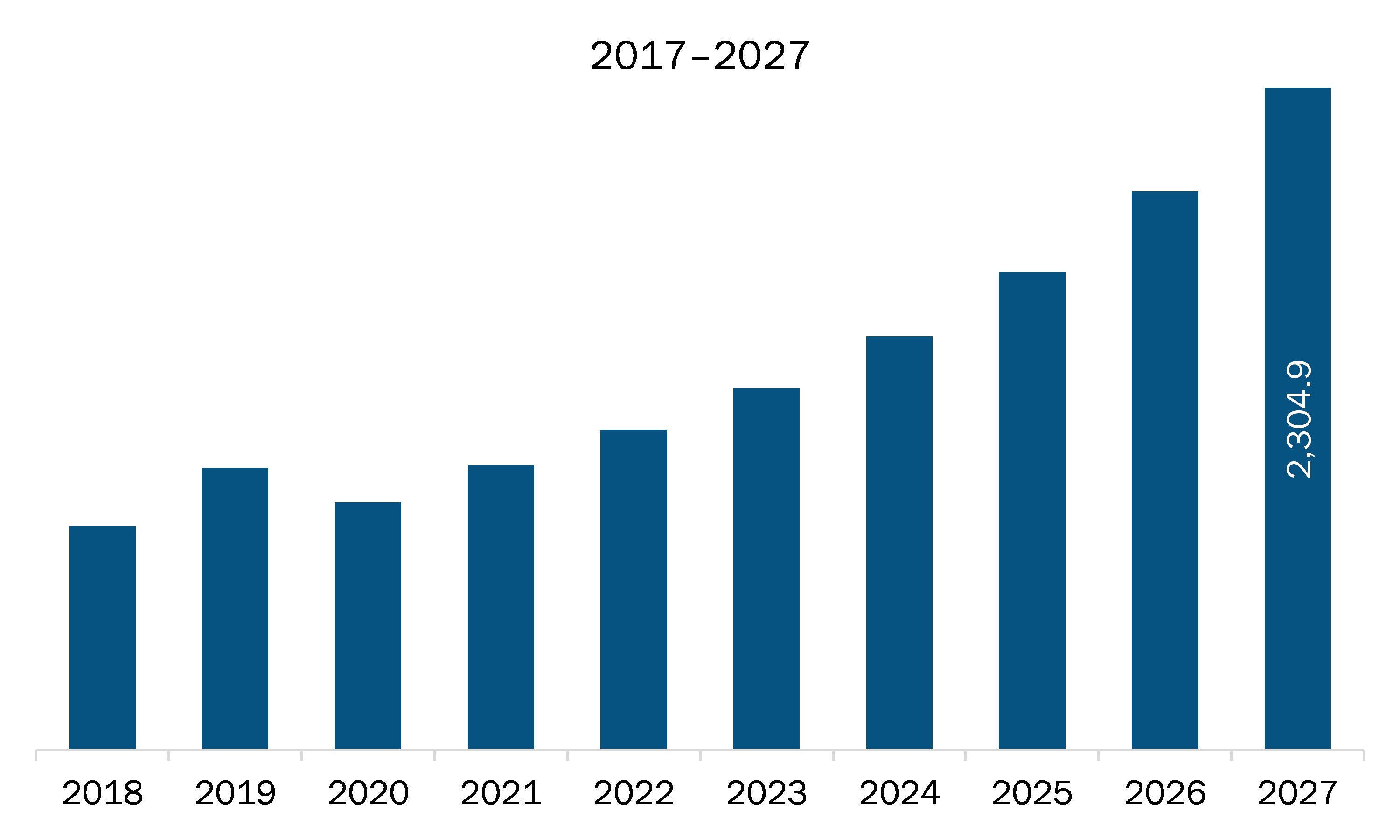

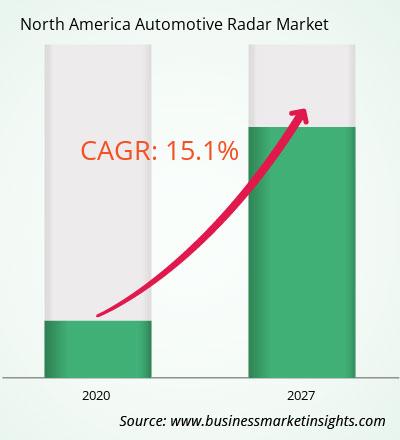

The automotive radar market in North America is expected to grow from US$ 982.2 million in 2019 to US$ 2,304.9 million by 2027; it is estimated to grow at a CAGR of 15.1% from 2020 to 2027. With the mounting number of level 2+ vehicles on road, the need for advanced and more accurate automotive radar sensors is increasing. This acts as a huge opportunity for OEMs offering basic-level radar sensors. For instance, Xilinx and Continental announced the first production-ready 4D imaging radar. Theoretically, 4D imaging radar uses echolocation (mechanism that is observed in dolphins, bats, and several humans) and the time-of-flight measurement principle to capture a space in 3D. Furthermore, these radar systems are designed fulfill the imaging requirements within the time scale of a fast-moving automobile or a zooming drone. Therefore, the fourth dimension enhances the overall accuracy in a self-driving system. The 4D imaging radar is operational in all types of whether/environment conditions, including fog, darkness, and heavy rains. Numerous companies are investing in R&D to introduce such advanced radar-based imaging technologies and gain a maximum share in the North America automotive radar market.

Based on range, the short range radar segment is expected to lead the market throughout the forecast period. By frequency, 24 GHz is expected to dominate the market in 2019; however, the 77 GHz is anticipated to attain the highest market share by frequency by 2027. By Application, the adaptive cruise control segment is anticipated to dominate the market by 2027. The passenger cars segment is expected to hold over 70% of the market share based on vehicle type from 2019 to 2027.

A few major primary and secondary sources referred to for preparing this report on the automotive radar market in North America are company websites, annual reports, financial reports, national government documents, and statistical database, among others. Major companies listed in the report are North America automotive radar market. Aptiv Plc; Continental AG; Denso Corporation; HELLA KGaA Hueck & Co.; Infineon Technologies AG; Nidec Corporation; Robert Bosch GmbH; Valeo; Veoneer Inc; ZF Friedrichshafen AG.

The North America Automotive Radar Market is valued at US$ 982.2 Million in 2019, it is projected to reach US$ 2,304.9 Million by 2027.

As per our report North America Automotive Radar Market, the market size is valued at US$ 982.2 Million in 2019, projecting it to reach US$ 2,304.9 Million by 2027. This translates to a CAGR of approximately 15.1% during the forecast period.

The North America Automotive Radar Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Automotive Radar Market report:

The North America Automotive Radar Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Automotive Radar Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Automotive Radar Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Automotive Radar Market

Get Free Sample For North America Automotive Radar Market