North America Aircraft Ignition System Market

Growing Adoption of Fully Authority Digital Engine Control (FADEC) systems is Fueling the North America Aircraft Ignition System Market

The FADEC system is used in an aircraft to decrease pilot’s workload by providing details on mechanical problems, as well as portrays engine monitoring capability. This autonomous, self-monitoring, self-operating, and redundant system enables the pilot to monitor fuel economy. It also helps in diagnostic processes that require constant monitoring of crucial processes in an aircraft powerplant, increasing fuel efficiency, and reducing maintenance expenses. The FADEC system is developed to support both commercial and military aircraft. It is used in majority of aircraft engines, across different popular narrow-body and wide-body aircraft models. It is a safety-critical system wherein adequate redundancy is configured to provide necessary reliability and availability. As the demand for FADEC systems is increasing, several players are creating alliances. As FADEC system improves fuel efficiency, obtains redundancy in case of failure, provides care-free engine handling, and is used for better systems integration, its adoption in the market is increasing. Hence, all the above factors are propelling the adoption of FADEC systems, which will lead to the North America aircraft ignition system market growth during the forecast period.

North America Aircraft Ignition System Market Overview

The North America aircraft ignition system market is further segmented into the US, Canada, and Mexico. The demand for aircraft is high in the region due to the actively proliferating commercial, general, and defense aviation industries in the major countries. Boeing delivered 157 and 340 commercial aircraft in 2020 and 2021, respectively. With a surge in the manufacturing of aircraft, the demand for aircraft engines is also increasing, thereby propelling the need for engine components, such as ignition systems, cylinders, vacuum pumps, carburetors, and alternators. North America is home to several engine manufacturers involved in the manufacturing of turboprop, turbofan, turbojet, and piston engines. A few of the aircraft engine manufacturers headquartered in the region include General Electric Company, Honeywell International Inc., Williams International, and Pratt & Whitney. These companies are entering into several contracts for supplying engines to commercial and military aircraft manufacturers. For example, in November 2021, General Electric Company received a contract worth US$ 1.57 billion from the US Air Force to supply 29 USAF F-15EX jet engines, with the expected commencement of deliveries from 2023 onward. Additionally, per the contract, the engine manufacturer would supply 329 additional engines to the air force in the final delivery phase in 2031. Thus, a rise in engine manufacturing is bolstering the demand for ignition systems in North America. Many aircraft ignition system manufacturers have a notable presence in North America. A few of these include Champion Aerospace Inc., Kelly Aerospace Inc, Unison LLC, Tempest Aero Group, and FADEC International. These companies are adopting various organic and inorganic growth strategies to expand their geographic presence, strengthen their distribution channel, and enhance their product portfolios. Unison, LLC announced the launch of its new igniter plug in June 2019. The new igniter enabled by a patented technology is designed to improve spark life under extreme environmental conditions. In March 2020, Champion Aerospace appointed Airpart Supply Ltd as its authorized distributor in Europe. The partnership includes the distribution of slick magnetos, oil filters, harnesses, spark plugs, and spare parts, along with the turbine range, including exciter boxes, igniter plugs, and ignition leads.

Strategic insights for the North America Aircraft Ignition System provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

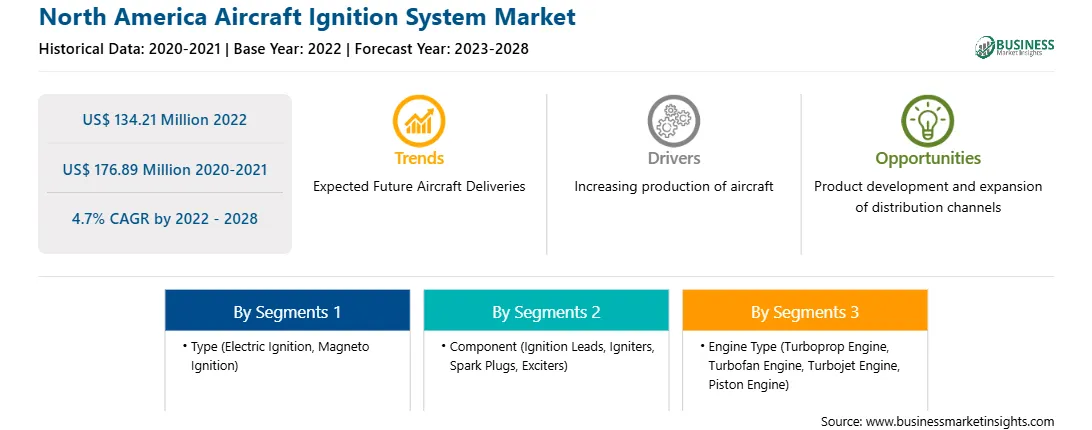

| Market size in 2022 | US$ 134.21 Million |

| Market Size by 2028 | US$ 176.89 Million |

| Global CAGR (2022 - 2028) | 4.7% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Type

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

The geographic scope of the North America Aircraft Ignition System refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

North America Aircraft Ignition System Market Segmentation

The North America aircraft ignition system market is segmented based on component, type, engine type, and country.

Based on component, the North America aircraft ignition system market is segmented into ignition leads, igniters, spark plugs, exciters, and others. The spark plugs segment held the largest market share in 2022.

Based on type, the North America aircraft ignition system market is bifurcated into electric ignition and magneto ignition. The electric ignition segment held a larger market share in 2022.

Based on engine type, the North America aircraft ignition system market is segmented into turboprop engine, turbofan engine, turbojet engine, and piston engine. The turbofan engine segment held the largest market share in 2022.

Based on country, the North America aircraft ignition system market has been categorized into the US, Canada, and Mexico. Our regional analysis states that the US dominated the market in 2022.

Champion Aerospace Inc, Continental Aerospace Technologies Inc, Electroair Acquisition Corp, FADEC International LLC, Kelly Aerospace Inc, PBS Group AS, Sonex LLC, Surefly Partners Ltd, Tempest Aero Group LLC, and Unison Industries LLC are the leading companies operating in the North America aircraft ignition system market.

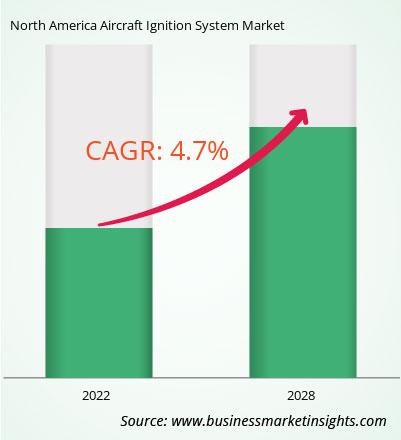

The North America Aircraft Ignition System Market is valued at US$ 134.21 Million in 2022, it is projected to reach US$ 176.89 Million by 2028.

As per our report North America Aircraft Ignition System Market, the market size is valued at US$ 134.21 Million in 2022, projecting it to reach US$ 176.89 Million by 2028. This translates to a CAGR of approximately 4.7% during the forecast period.

The North America Aircraft Ignition System Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Aircraft Ignition System Market report:

The North America Aircraft Ignition System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Aircraft Ignition System Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Aircraft Ignition System Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Aircraft Ignition System Market

Get Free Sample For North America Aircraft Ignition System Market