North America Air Defense Radar Market

Changing modern warfare systems have been urging governments across the world to allocate higher funds toward respective military forces. The military budget allocation enables defense forces to procure advanced technologies and equipment from domestic or international manufacturers. On the same lines, soldier and military vehicle modernization practices are on the rise across numerous countries. With the need to strengthen military forces with advanced technologies, armaments, artilleries, and vehicles, among others, defense forces across the globe are investing substantial amounts in the products mentioned above. A continuous urge to procure new technologies for combat and noncombat operations by defense forces is further boosting defense spending across the world. Growing defense expenditure is stimulating the procurement of modern warfare technologies such as unmanned vehicles, lightweight radars, missile detection systems, and surveillance systems. Moreover, a higher defense budget allows countries to allocate resources for the modernization and upgrade of their existing air defense systems. This includes the replacement or enhancement of outdated radar systems with more advanced and capable ones. In April 2022, Canada announced an investment of over US$ 1 billion in a new radar system to protect major North American cities. This radar system would be constructed in southern Canada to monitor Arctic airspace and safeguard vital locations in both the US and Canada.

In North America, military expenditure is significantly increasing due to rising geopolitical tension. According to Stockholm International Peace Research Institute (SIPRI), the military expenditure of the region was US$ 809,723.4 million in 2020; it increased to US$ 840,273.3 million in 2021 and reached US$ 912,375.03 million in 2022. Hence, the adoption of combat aircraft, unmanned systems, various types of military ground vehicles, naval platforms, and other technologies and systems has increased. According to the World Directory of Modern Military Aircraft (WDMMA) and Global Fire Power Index (FPI), North America currently holds 466 fleets, including frigates, corvettes, destroyers, aircraft carriers, and submarines. Apart from these, in 2023, the region secured 72 fleets for future procurement. Air defense radar systems in surveillance and reconnaissance aircraft monitor and detect enemy aircraft, identify potential threats, and gather intelligence. These radars provide wide-area coverage, target identification, and tracking capabilities to support intelligence gathering and situational awareness. Further, air defense radar systems are critical components of naval surface combatants. These radars provide long-range detection, tracking, and engagement capabilities against airborne threats, including enemy aircraft, missiles, and unmanned aerial systems. They facilitate early warning, target acquisition, and support the deployment of air defense missiles and close-in weapon systems. Thus, the growing procurement of various military aircraft and naval platforms is expected to drive the North America Air Defense Radar Market.

The North America air defense radar market is segmented into function, range, system type, platform, application, and country.

Based on function, the North America air defense radar market is segmented into synthetic aperture radar and moving target indicator radar, surveillance radar, airborne early warning radar, multi-functional radar, weather radar, and others. The synthetic aperture radar and moving target indicator radar segment held a largest share of the North America air defense radar market in 2022.

Based on range, the North America air defense radar market is segmented into short range, medium range, and long range. The long-range segment held the largest share of the North America air defense radar market in 2022.

Based on system type, the North America air defense radar market is segmented into fixed radar, and portable radar. The fixed radar segment held the larger share of the North America air defense radar market in 2022.

Based on platform, the North America air defense radar market is segmented into ground-base, aircraft-mounted, and naval based. The ground-base segment held the largest share of the North America air defense radar market in 2022.

Based on application, the North America air defense radar market is segmented into ballistic missile defense, identification friend or foe, weather forecasting, and others. The identification friend or foe segment held the largest share of the North America air defense radar market in 2022.

Based on country, the North America air defense radar market is segmented into the US, Canada, and Mexico. The US dominated the North America air defense radar market in 2022.

BAE Systems Plc, General Dynamics Corp, Honeywell International Inc, Leonardo SpA, Lockheed Martin Corp, Northrop Grumman Corp, Raytheon Technologies Corp, Saab AB, and Thales SA are some of the leading companies operating in the North America air defense radar market.

Strategic insights for the North America Air Defense Radar provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 2,635.08 Million |

| Market Size by 2030 | US$ 3,841.02 Million |

| Global CAGR (2022 - 2030) | 4.8% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Range

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

The geographic scope of the North America Air Defense Radar refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

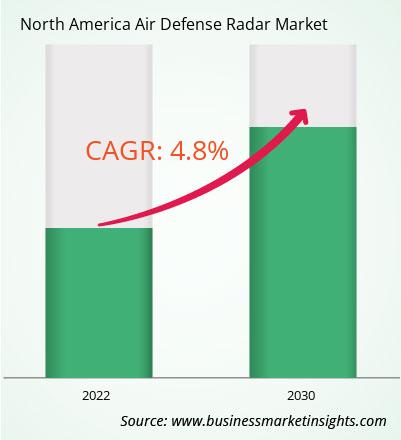

The North America Air Defense Radar Market is valued at US$ 2,635.08 Million in 2022, it is projected to reach US$ 3,841.02 Million by 2030.

As per our report North America Air Defense Radar Market, the market size is valued at US$ 2,635.08 Million in 2022, projecting it to reach US$ 3,841.02 Million by 2030. This translates to a CAGR of approximately 4.8% during the forecast period.

The North America Air Defense Radar Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Air Defense Radar Market report:

The North America Air Defense Radar Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Air Defense Radar Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Air Defense Radar Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Air Defense Radar Market

Get Free Sample For North America Air Defense Radar Market