Middle East and Africa Offshore Pipeline Market

The offshore pipeline, often known as, submarine or subsea pipeline is used for the transportation of oil, gas, and refined products. The MEA offshore pipeline market is increasingly gaining traction on account of higher efficiency and large capacity. In addition to this, the offshore pipeline provides faster, safer, and more reliable connectivity for oil and gas transportation. The MEA region includes countries such as South Africa, Saudi Arabia, and the UAE. The MEA region is projected to have a rapid rise in urbanization and industrialization, which would further drive the growth of the entire economy. The Gulf countries are economically advanced, while the African countries are yet to balance the economic conditions. Similarly, the boost in per capita income, recovering economic conditions, and government spending toward infrastructure development of the region are among the factors anticipated to drive the adoption of offshore pipeline. The MEA offshore pipeline market is expected to witness considerable growth during the forecast period owing to the escalation in the number of natural gas projects as well as the finding of new oil fields, particularly in remote locations. Factors such as discovery of new oil and gas reserves across MEA region and improvements and developments in flexible pipe technology are also expected to drive the MEA offshore pipeline market.

Moreover, in case of COVID-19, MEA is highly affected specially the Saudi Arabia and Iran. The COVID-19 pandemic has negatively affected the overall oil & gas industry owing to considerable disruption in the industry supply chain activities coupled with the several countries across MEA region sealing off their international trade in wake of the pandemic. The MEA region especially the GCC countries witnessed a notable decline in their oil & gas sector owing to sharp decline in demand of oil from major end-user countries across Asia, Europe and North American regions as a result, the countries registered a lowered volume of oil production as well as construction of oil & gas related projects and subsequently the demand for offshore pipelines. Countries such as Saudi Arabia, UAE, Qatar and selected other members of OPEC countries also observed similar trends during the early months of the pandemic outbreak. The coronavirus outbreak's impact is anticipated to be quite severe in the year 2020 and likely in 2021. Hence, the ongoing COVID-19 crisis and critical situation in the countries like the Saudi Arabia and Iran will impact the offshore pipeline market growth of the MEA region negatively for the next few quarters.

Strategic insights for the Middle East and Africa Offshore Pipeline provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

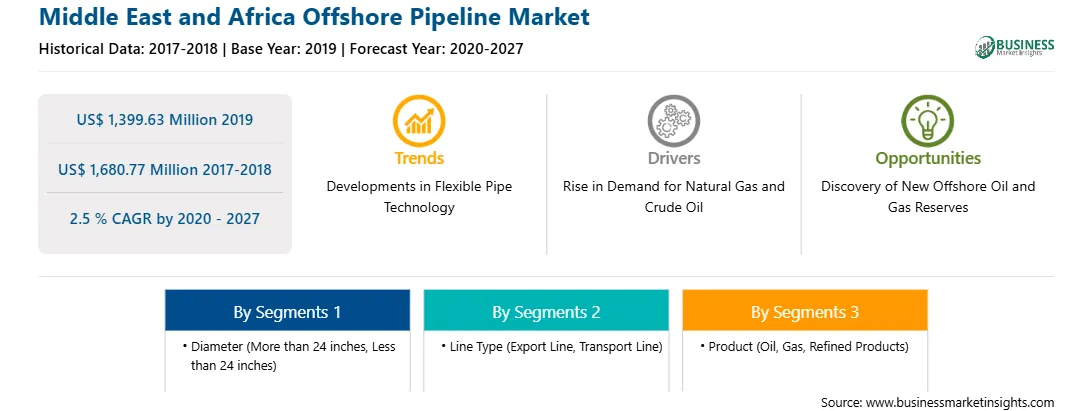

| Market size in 2019 | US$ 1,399.63 Million |

| Market Size by 2027 | US$ 1,680.77 Million |

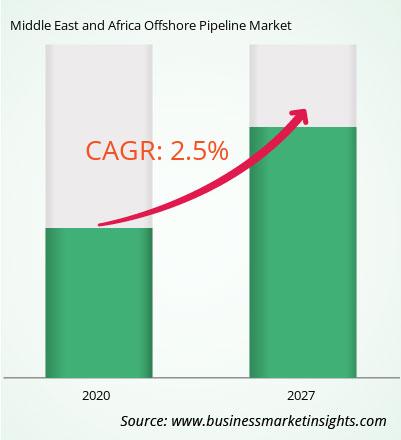

| Global CAGR (2020 - 2027) | 2.5 % |

| Historical Data | 2017-2018 |

| Forecast period | 2020-2027 |

| Segments Covered |

By Diameter

|

| Regions and Countries Covered | Middle East and Africa

|

| Market leaders and key company profiles |

The geographic scope of the Middle East and Africa Offshore Pipeline refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

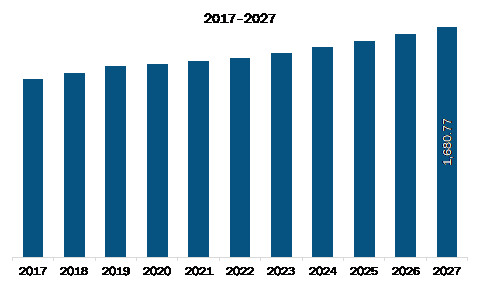

The MEA offshore pipeline market is expected to grow from US$ 1,399.63 million in 2019 to US$ 1,680.77 million by 2027; it is estimated to grow at a CAGR of 2.5 % from 2020 to 2027. Escalation in demand for natural gas and crude oil across MEA region is expected to upsurge MEA offshore pipeline market. The demand for natural gas and crude oil is witnessing a constant increase across the MEA region. The robust increase in petrochemical demand in the MEA region resulted in increased consumption. Surge in industrial production along with high demand for trucking services are boosting the need for petrochemicals, thereby fueling the growth of the market across MEA region. Rise in demand for oil & gas across MEA region is attributed to increasing industrialization and urbanization. Several oil & gas companies in MEA region are focused on increasing their offshore exploration & production (E&P) activities to fulfil the constantly increasing energy demand. Some of the significant oil & gas pipeline projects across MEA region expected in 2020 are Al Zour Refinery (Kuwait) and South Pars Phases 13-14 (Iran). Rising demand for oil & gas due to rise in industrialization and urbanization has resulted in increased E&P activities, which, in turn, is supporting the growth of the MEA offshore pipeline market.

In terms of diameter, the more than 24 inches’ segment accounted for the largest share of the MEA offshore pipeline market in 2019. In terms of line type, the transport line segment held a larger market share of the MEA offshore pipeline market in 2019. Further, the refined products segment held a larger share of the MEA offshore pipeline market based on product in 2019.

A few major primary and secondary sources referred to for preparing this report on the MEA offshore pipeline market are company websites, annual reports, financial reports, national government documents, and statistical database, among others. Major companies listed in the report are Bechtel Corporation; Fugro; John Wood Group PLC; Larsen & Toubro Limited; McDermott International, Inc.; Petrofac Limited; Saipem S.p.A; Sapura Energy Berhad; Subsea 7 S.A.; TechnipFMC plc.

Some of the leading companies are:

The Middle East and Africa Offshore Pipeline Market is valued at US$ 1,399.63 Million in 2019, it is projected to reach US$ 1,680.77 Million by 2027.

As per our report Middle East and Africa Offshore Pipeline Market, the market size is valued at US$ 1,399.63 Million in 2019, projecting it to reach US$ 1,680.77 Million by 2027. This translates to a CAGR of approximately 2.5 % during the forecast period.

The Middle East and Africa Offshore Pipeline Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East and Africa Offshore Pipeline Market report:

The Middle East and Africa Offshore Pipeline Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Middle East and Africa Offshore Pipeline Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Middle East and Africa Offshore Pipeline Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Middle East and Africa Offshore Pipeline Market

Get Free Sample For Middle East and Africa Offshore Pipeline Market