Middle East & Africa Lignin Market

Carbon fibers are high-performance materials with superior properties such as high stiffness, high flexibility, good tensile strength, low thermal expansion, high-temperature tolerance, lightweight, and high fatigue resistance. These properties make carbon fibers essential in producing advanced composites for various industrial applications, including aerospace, transportation, wind energy, construction, and automotive. Most carbon fibers are manufactured from polyacrylonitrile, a petroleum-based, non-renewable, and unsustainable chemical at a relatively higher price. However, lignin is a renewable, inexpensive, and highly accessible resource that can fabricate lignin-based carbon fibers. The constant diminishing of petroleum resources and associated environmental issues are major factors expected to boost the demand for lignin for carbon fiber production.

Manufacturers in the carbon fiber industry increasingly use lignin as a raw material to produce carbon fiber to cater to the increasing demand. For instance, in July 2021, Stora Enso Oyj, a manufacturer of pulp, paper, and other forest products, established a pilot plant for lignin-based carbon materials for batteries. According to Stora Enso Oyj, the demand for batteries is expected to rise tremendously over the next decade as battery producers require more sustainable materials for the electrification of mobility and reduction of carbon emissions. The company projects that carbon-based-anode materials, produced from converted lignin separated from wood, can be a more sustainable replacement for graphite-based battery anodes. Thus, the adoption of lignin for carbon fiber production will likely offer lucrative opportunities for the market players during the forecast period.

Lignin is a byproduct of bioethanol, pulp and paper, and compressed biogas plants. It is also used as a bitumen extender in the production of asphalt mixtures that are used in the development of sustainable infrastructure, including roadways. In addition, it is widely used as a grinding agent in cement production, cement substitute materials, water-reducing admixtures, and set retarders. Governments of several countries in the Middle East & Africa focus on investing in the construction and infrastructure sector. Based on a report by the International Trade Administration in 2022, the 2020–2025 development plan by the Government of Kuwait focuses on economic reforms and megaprojects, encompassing infrastructure projects worth US$ 124 billion. According to the same report, the UAE has lined-up transportation and road infrastructure projects—including the Etihad rail project worth US$ 11 billion, the hyperloop project valued at US$ 5.9 billion (connecting Dubai and Abu Dhabi), and the Sheikh Zayed double-deck road project with a valuation of US$ 2.7 billion. In 2021, Abu Dhabi National Oil Company (UAE) announced its plans to develop a large-scale seawater treatment and transmission pipeline project in Abu Dhabi. The UAE government plans to achieve 50% of its total construction via sustainable operations by 2030. Therefore, an upsurge in the construction industry and various government initiatives promoting sustainable construction boost the demand for lignin in the Middle East & Africa.

Strategic insights for the Middle East & Africa Lignin provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market. The geographic scope of the Middle East & Africa Lignin refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas. Get more information on this report

Get more information on this report Middle East & Africa Lignin Strategic Insights

Get more information on this report

Get more information on this report Middle East & Africa Lignin Report Scope

Report Attribute

Details

Market size in 2022

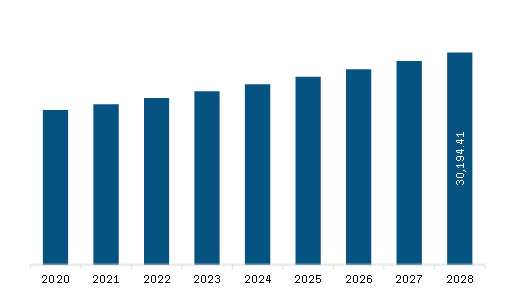

US$ 23,684.38 thousand

Market Size by 2028

US$ 30,194.41 thousand

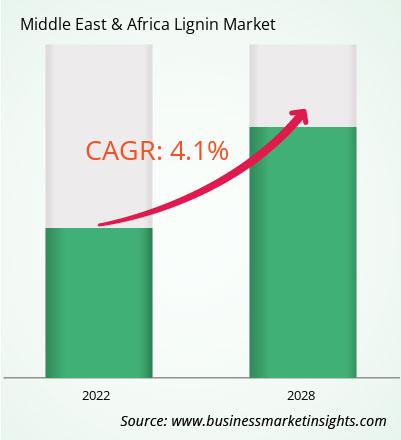

Global CAGR (2022 - 2028)

4.1%

Historical Data

2020-2021

Forecast period

2023-2028

Segments Covered

By Type

By Form

By Application

Regions and Countries Covered

Middle East and Africa

Market leaders and key company profiles

Get more information on this report Middle East & Africa Lignin Regional Insights

Get more information on this report

Get more information on this report

Middle East & Africa Lignin Market Segmentation

The Middle East & Africa lignin market is segmented based on type, form, application, and country. Based on type, the Middle East & Africa lignin market is segmented into lignosulfonates, kraft lignin, high purity lignin, and others. The lignosulfonates segment held the largest Middle East & Africa lignin market share in 2022.

Based on form, the Middle East & Africa lignin market is bifurcated into solid and liquid. The solid segment held a larger market share in 2022.

Based on application, the Middle East & Africa lignin market is segmented into concrete additives, plastics and polymers, bitumen, water treatment, dyes and pigments, activated carbon, carbon fiber, and others. The dyes and pigments segment held the largest market share in 2022.

Based on country, the Middle East & Africa lignin market is segmented into Saudi Arabia, South Africa, the UAE, and the Rest of Middle East & Africa. Saudi Arabia dominated the Middle East & Africa lignin market share in 2022.

Nippon Paper Industries Co Ltd; Borregaard ASA; Burgo Group SpA; Domsjo Fabriker AB; Sappi Ltd; Stora Enso Oyj; Suzano SA; and The Dallas Group of America Inc are the leading companies operating in the Middle East & Africa lignin market.

The Middle East & Africa Lignin Market is valued at US$ 23,684.38 thousand in 2022, it is projected to reach US$ 30,194.41 thousand by 2028.

As per our report Middle East & Africa Lignin Market, the market size is valued at US$ 23,684.38 thousand in 2022, projecting it to reach US$ 30,194.41 thousand by 2028. This translates to a CAGR of approximately 4.1% during the forecast period.

The Middle East & Africa Lignin Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East & Africa Lignin Market report:

The Middle East & Africa Lignin Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Middle East & Africa Lignin Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Middle East & Africa Lignin Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Middle East & Africa Lignin Market

Get Free Sample For Middle East & Africa Lignin Market