Middle East & Africa Heart Transplant Market

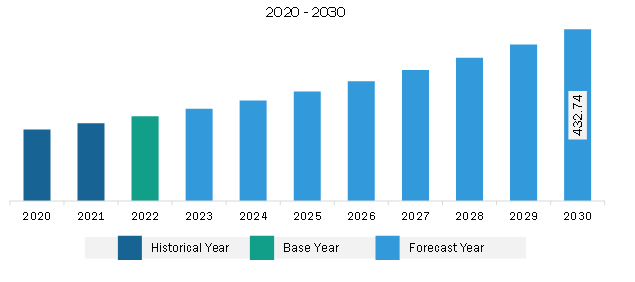

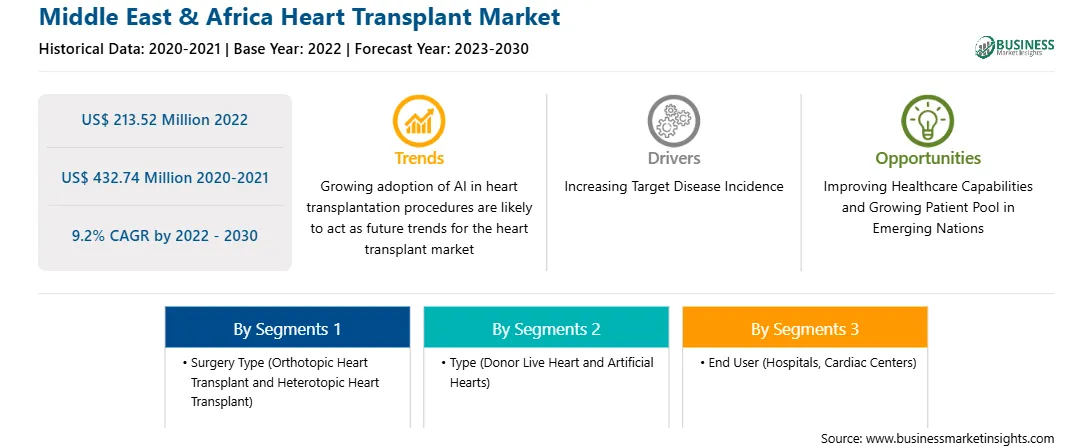

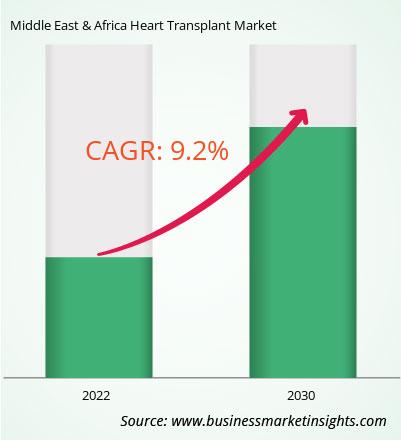

The Middle East & Africa heart transplant market is expected to grow from US$ 213.52 million in 2022 to US$ 432.74 million by 2030. It is estimated to grow at a CAGR of 9.2% from 2022 to 2030.

The World Health Organization (WHO) states cardiovascular disease (CVD) is one of the leading causes of death worldwide. A few of the major contributors to the rising prevalence of CVDs are ethnicity, family history, and age. Other notable factors include increasing tobacco consumption, high cholesterol, hypertension; and diseases such as obesity, dyslipidemia, and diabetes. According to the WHO, deaths due to CVDs across the world will rise from ~17 million in 2016 to 23.6 million by 2030. Moreover, the global cost burden of CVDs would reach US$ 1,044 billion by 2030 from US$ 863 billion in 2010. Since its opening in 2017, the multi-organ transplant centre Cleveland Clinic Abu Dhabi in the United Arab Emirates has completed 386 transplants. Additionally, as of 2023, more than 431 heart transplant procedures have been performed at the KFSHRC Saudi Arabia overall since the program's inception in 1989. Therefore, the rising incidence of CVDs and heart failure drives the growth of the heart transplant market.

The Middle East & Africa heart transplant market is categorized into the UAE, Saudi Arabia, South Africa, and the Rest of the Middle East & Africa. The increase in prevalence of heart failure in geriatric population of the region and improving healthcare facilities is fueling the growth of heart transplant market in Middle East & Africa. Saudi Arabia is estimated to register considerable growth in the heart transplant market. The country has a large obese and geriatric population prone to cardiovascular disorders. According to the WHO, coronary heart disease deaths in Saudi Arabia reached 39,037 in 2020, accounting for 29.13% of total deaths. A report published in the Journal of Nature and Science of Medicine states the estimated number of heart failure in the country was 455,222 in 2021, with 37,935 new cases arising every year. Coronary heart disease is characterized by the build-up of fatty substances in the arteries leading to heart block or blood flow interruption to the heart; treating this condition needs heart transplant intervention. Olive oil consumption also poses a risk of cardiovascular-related deaths and all-cause deaths.

Public organizations and the government have initiated programs to enhance healthcare services in the country. In the last few years, the private sector has been playing an important role in the healthcare system in Saudi Arabia, owing to the rising investments. The government of Saudi Arabia has launched the Saudi Vision 2030 program to reduce oil dependence and diversify the economy. This has led to significant developments in healthcare services and the high adoption rate of advanced technologies. In January 2023, Saudi doctors performed a heart transplant on an eight-month-old girl, claiming she was the youngest patient in the Middle East to have undergone the procedure. Hence, the rising prevalence of cardiovascular disorders and heart failure in the country, developments in healthcare services, and increasing investments by government and private organizations are expected to boost the growth of the heart transplant market in Saudi Arabia in the future.

Strategic insights for the Middle East & Africa Heart Transplant provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 213.52 Million |

| Market Size by 2030 | US$ 432.74 Million |

| Global CAGR (2022 - 2030) | 9.2% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Surgery Type

|

| Regions and Countries Covered | Middle East and Africa

|

| Market leaders and key company profiles |

The geographic scope of the Middle East & Africa Heart Transplant refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Middle East & Africa heart transplant market is segmented into surgery type, type, end user, and country.

Based on surgery type, the Middle East & Africa heart transplant market is bifurcated into orthotopic heart transplantation and heterotopic heart transplantation. The orthotopic heart transplantation segment held a larger share of the Middle East & Africa heart transplant market in 2022.

In terms of type, the Middle East & Africa heart transplant market is bifurcated into donor live heart and artificial heart. The donor live heart segment held a larger share of the Middle East & Africa heart transplant market in 2022. Further, artificial heart segment is categorized into ventricular assisted device and total artificial heart.

Based on end user, the Middle East & Africa heart transplant market is segmented into hospitals, cardiac centres, and others. The hospitals segment held the largest share of the Middle East & Africa heart transplant market in 2022.

Based on country, the Middle East & Africa heart transplant market is segmented into Saudi Arabia, South Africa, the UAE, and Rest of Middle East & Africa. Saudi Arabia dominated the Middle East & Africa heart transplant market in 2022.

Terumo Corp, Abbott Laboratories, SynCardia Systems LLC, and LivaNova Plc are some of the leading companies operating in the Middle East & Africa heart transplant market.

1. Terumo Corp

2. Abbott Laboratories

3. SynCardia Systems LLC

4. LivaNova Plc

The Middle East & Africa Heart Transplant Market is valued at US$ 213.52 Million in 2022, it is projected to reach US$ 432.74 Million by 2030.

As per our report Middle East & Africa Heart Transplant Market, the market size is valued at US$ 213.52 Million in 2022, projecting it to reach US$ 432.74 Million by 2030. This translates to a CAGR of approximately 9.2% during the forecast period.

The Middle East & Africa Heart Transplant Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East & Africa Heart Transplant Market report:

The Middle East & Africa Heart Transplant Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Middle East & Africa Heart Transplant Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Middle East & Africa Heart Transplant Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Middle East & Africa Heart Transplant Market

Get Free Sample For Middle East & Africa Heart Transplant Market