Middle East & Africa Ferroalloys Market

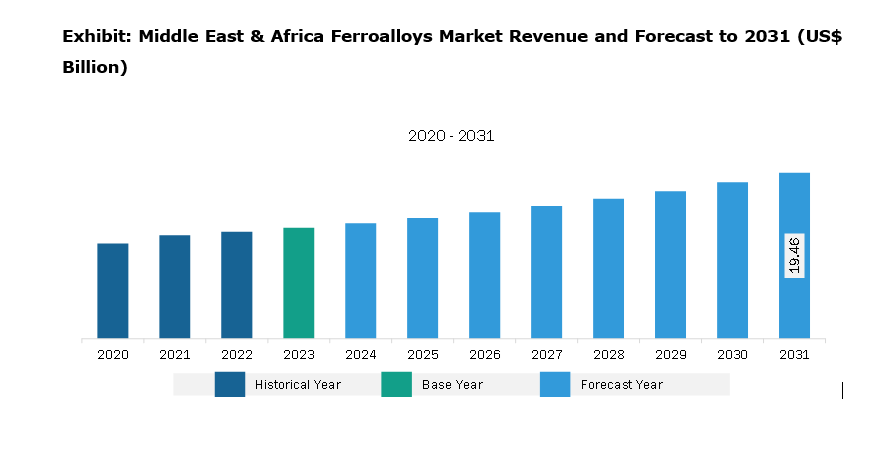

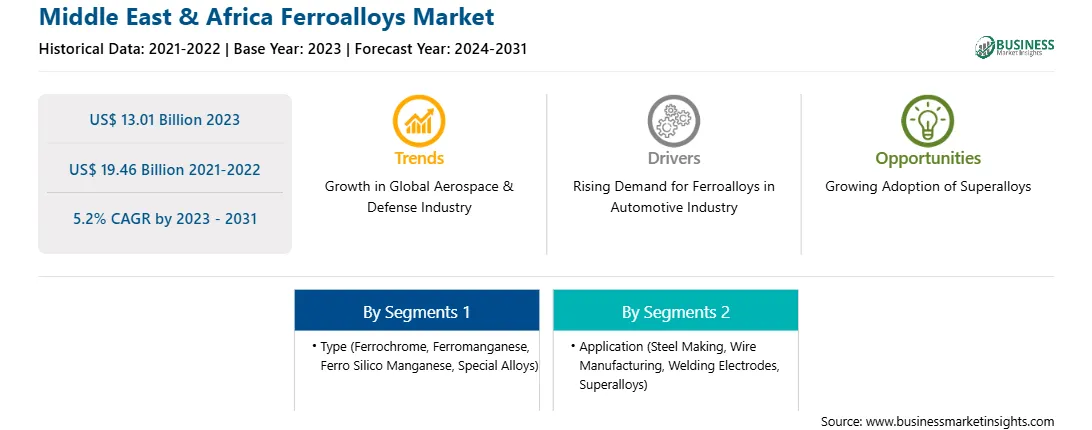

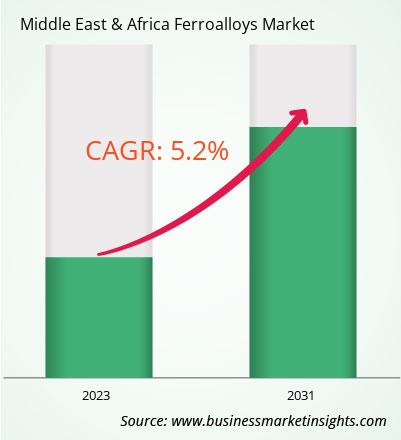

The Middle East & Africa ferroalloys market was valued at US$ 13.01 billion in 2023 and is expected to reach US$ 19.46 billion by 2031; it is estimated to register a CAGR of 5.2% from 2023 to 2031.

Growing Adoption of Superalloys Boosts Middle East & Africa Ferroalloys Market

Superalloys are high-performance materials engineered to withstand extreme temperatures, corrosion, and mechanical stress, making them ideal for applications in harsh operating conditions. In the aerospace industry, superalloys play a critical role in the production of aircraft engines, gas turbines, and components subjected to high temperatures and mechanical loads. These alloys offer exceptional strength and oxidation resistance, allowing the efficient and reliable operation of jet engines and other propulsion systems. In the energy industry, superalloys are used in gas and steam turbines, and oil and gas exploration equipment. The infrastructure development of renewable energy sources, such as wind and solar power, also boosts the utilization of superalloys in the manufacturing of turbine blades, generator components, and heat exchangers-supporting the transition to clean and sustainable energy sources.

The adoption of superalloys is driven by the ongoing research and development efforts aimed at improving the material properties, manufacturing processes, and cost-effectiveness. Advances in alloy design and processing techniques enable the development of a new generation of superalloys with superior performance characteristics. Ferroalloys are used in the production of superalloys that find application in various end-use industries. For instance, vacuum-grade Ferro-niobium alloy is used for superalloy additions in turbine blade applications in jet engines and land-based turbines. Thus, the growing adoption of superalloys is expected to positively influence the ferroalloys market in the coming years.

Middle East & Africa Ferroalloys Market Overview

Infrastructure projects, steel production, and natural resource availability drive the ferroalloy market in the Middle East & Africa. Countries such as Oman, Saudi Arabia, and the UAE have been focusing on diversifying their economies beyond oil and gas through investments in several industries, including steel production and alloy manufacturing. The Saudi government's Vision 2030 plan has placed a strong emphasis on infrastructure development, which has driven significant growth in the steel sector. As per the International Trade Administration, the construction sector's value in the UAE is expected to grow by 4.7% per annum in the next five years. The growth can be attributed to the increasing construction initiatives.

The region also marks the presence of several steel companies such as Al-Ittefaq Steel Products Company (ISPC), Saudi Iron & Steel Co, Zamil Steel Holding Company Limited, Aasia Steel Factory Co Ltd, Shaaban Steel, Modern Factory for Steel Industries, Alssad Steel for Industry Co, Abdulkarim Alrajhi Steel Company, Al Tilal Al Saudi Steel Industrial Factory, and Al Gaswa Steel Company Limited. According to the World Steel Association, in Saudi Arabia and the UAE, the total production of crude steel stood at 9.94 million metric tons and 3.77 million metric tons, respectively, in 2023. Thus, developments in the end-use industries fuel the demand for ferroalloys in the Middle East & Africa.

Strategic insights for the Middle East & Africa Ferroalloys provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market. The geographic scope of the Middle East & Africa Ferroalloys refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas. Get more information on this report

Get more information on this report Middle East & Africa Ferroalloys Strategic Insights

Get more information on this report

Get more information on this report Middle East & Africa Ferroalloys Report Scope

Report Attribute

Details

Market size in 2023

US$ 13.01 Billion

Market Size by 2031

US$ 19.46 Billion

Global CAGR (2023 - 2031)

5.2%

Historical Data

2021-2022

Forecast period

2024-2031

Segments Covered

By Type

By Application

Regions and Countries Covered

Middle East and Africa

Market leaders and key company profiles

Get more information on this report Middle East & Africa Ferroalloys Regional Insights

Get more information on this report

Get more information on this report

Middle East & Africa Ferroalloys Market Segmentation

The Middle East & Africa ferroalloys market is categorized into type, application, and country.

Based on type, the Middle East & Africa ferroalloys market is segmented into ferrochrome, ferromanganese, ferro silico manganese, special alloys, and others. The ferro silico manganese segment held the largest market share in 2023.

In terms of application, the Middle East & Africa ferroalloys market is categorized into steel making, wire manufacturing, welding electrodes, superalloys, and others. The steel making segment held the largest market share in 2023.

By country, the Middle East & Africa ferroalloys market is segmented into South Africa, Saudi Arabia, the UAE, and the Rest of Middle East & Africa. The Rest of Middle East & Africa dominated the Middle East & Africa ferroalloys market share in 2023.

Glencore Plc, Samancor Chrome, Brahm Group, Tata Steel Ltd, and Nava Ltd, are some of the leading companies operating in the Middle East & Africa ferroalloys market.

The Middle East & Africa Ferroalloys Market is valued at US$ 13.01 Billion in 2023, it is projected to reach US$ 19.46 Billion by 2031.

As per our report Middle East & Africa Ferroalloys Market, the market size is valued at US$ 13.01 Billion in 2023, projecting it to reach US$ 19.46 Billion by 2031. This translates to a CAGR of approximately 5.2% during the forecast period.

The Middle East & Africa Ferroalloys Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East & Africa Ferroalloys Market report:

The Middle East & Africa Ferroalloys Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Middle East & Africa Ferroalloys Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Middle East & Africa Ferroalloys Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Middle East & Africa Ferroalloys Market

Get Free Sample For Middle East & Africa Ferroalloys Market