Europe Veterinary Diagnostics Market

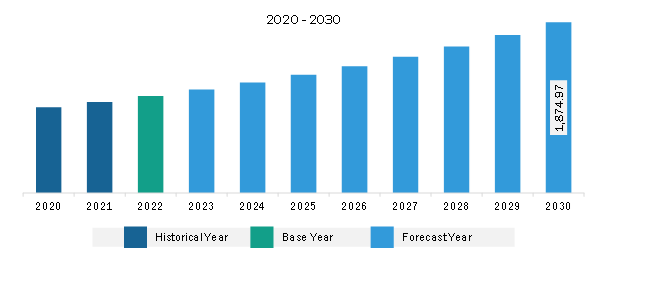

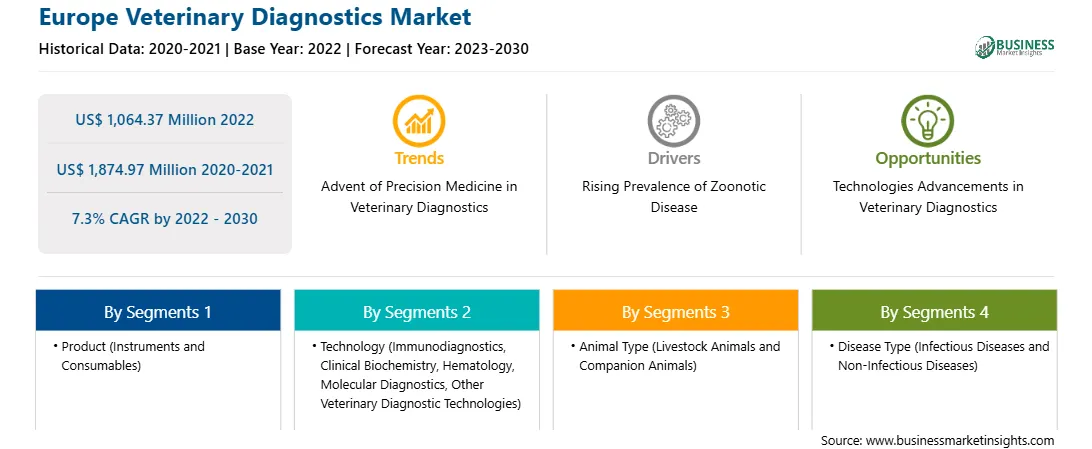

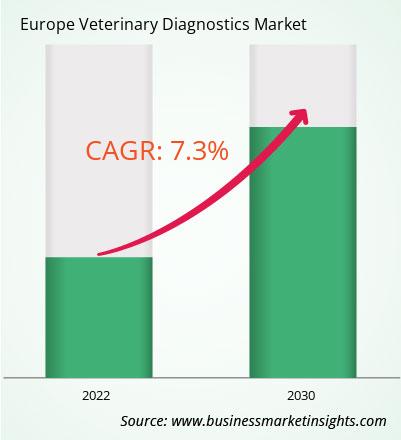

The Europe veterinary diagnostics market was valued at US$ 1,064.37 million in 2022 and is expected to reach US$ 1,874.97 million by 2030; it is estimated to grow at a CAGR of 7.3% from 2022 to 2030.

Rising Prevalence of Zoonotic Disease Fuels Europe Veterinary Diagnostics Market

Zoonotic diseases cause illnesses not only in animals but also in humans. These infections can cause from mild to severe conditions. As per the Council on Foreign Relations, zoonoses cause 2.5 billion illnesses and 2.7 million deaths each year globally, accounting for 60% of known infectious diseases and 75% of new or emerging infectious diseases. Also, according to Centers for Disease Control and Prevention, in 2023, 6 out of every 10 infectious diseases in humans are spread by animals, and 3 of 4 new or emerging infectious diseases are transferred by animals. Further, dogs contribute to 99% of all rabies transmissions to humans and are a major source of human rabies deaths. The economic burden due to dog-mediated rabies is estimated to be US$ 8.6 billion/year globally.

According to the European Centre for Disease Prevention and Control, campylobacteriosis was the most reported zoonotic disease, with 127,840 cases in 2021 compared to 120,946 cases in 2020. Salmonellosis was the second most common zoonotic disease, with 60,050 cases in 2021 compared to 52,702 cases in 2020. The other commonly reported zoonotic diseases are Yarniniosis with 6,789 cases, Shigatoxin-producing E. coli infections with 6,084 cases, and listeriosis with 2,183 cases. Thus, the rising rabies globally increases the need for diagnoses of the illnesses, contributing to the growth of the veterinary diagnostics market. Also, the rising prevalence of zoonotic diseases globally accelerates the demand for veterinary diagnostics.

Europe Veterinary Diagnostics Market Overview

As per the Understanding Animal Research 2023 report, animals have been widely used for research in the European Union (EU) and Norway. Animals such as mice, fish, rats, and birds account for almost 93% of the animals used, with cats, dogs, and primates accounting for 0.22%. Among the EU, Germany has the highest utility of animals for research. A total of 11,609,978 animals were used for research in the EU in 2019, among which 10,40,1673 animals (90%) were used for experimental purposes. Among 11,609,978, 10% (i.e., 1,208,305 animals) were utilized for producing genetically altered animals. As per the Understanding Animal Research 2023 report, less than 4% animals were utilized as compared to 2018 due to the high severity of diseases among animals. Therefore, the rising need for animal research propels the need for diagnostic testing of veterinary animals. The World Health Organization (WHO) reported that the goose/Guangdong lineage of H5N1 avian influenza viruses caused bird outbreaks in 2020. Also, since 2020, a variant of these viruses belonging to the H5 clade 2.3.4.4b resulted in unprecedented deaths among wild birds and poultry in many European countries. Also, the increase in the trade of animals and animal types in the EU results in spreading of diseases across the region. Therefore, overcoming disease outbreaks from animals is the need of the hour. As a result, the UK promotes high welfare standards for livestock across the EU. Furthermore, the UK is successfully implementing measures such as improving the general well-being of animals to be utilized in scientific testing.

Strategic insights for the Europe Veterinary Diagnostics provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 1,064.37 Million |

| Market Size by 2030 | US$ 1,874.97 Million |

| Global CAGR (2022 - 2030) | 7.3% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Product

|

| Regions and Countries Covered | Europe

|

| Market leaders and key company profiles |

The geographic scope of the Europe Veterinary Diagnostics refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

Europe Veterinary Diagnostics Market Segmentation

The Europe veterinary diagnostics market is segmented based on product, technology, disease type, animal type, end user, and country.

Based on product, the Europe veterinary diagnostics market is bifurcated into instruments and consumables. The instruments segment held a larger share in 2022.

By technology, the Europe veterinary diagnostics market is segmented into immunodiagnostics, clinical biochemistry, hematology, molecular diagnostics, and other veterinary diagnostic technologies. The immunodiagnostics segment held the largest share in 2022. The immunodiagnostics segment is further subsegmented into lateral flow assays, ELISA, immunoassay, allergen-specific immunodiagnostics test, and other immunodiagnostics. The clinical biochemistry segment is further subsegmented into clinical chemistry analysis, glucose monitoring, and blood gas and electrolyte.

By disease type, the Europe veterinary diagnostics market is segmented into infectious diseases and non-infectious diseases. The infectious diseases segment held the largest share in 2022.

By animal type, the Europe veterinary diagnostics market is bifurcated into livestock animals and companion animals. The companion animals segment held a larger share in 2022. The livestock animals segment is further subsegmented into cattle, pigs, poultry, and other livestock animals. The companion animals segment is further subsegmented into dogs, cats, horses, and other companion animals.

By end user, the Europe veterinary diagnostics market is segmented into veterinary hospitals and clinics, animal diagnostic laboratories, and veterinary research institutes and universities. The companion animals segment held the largest share in 2022.

Based on country, the Europe veterinary diagnostics market is segmented into Germany, France, the UK, Italy, Spain, and the Rest of Europe. Germany dominated the Europe veterinary diagnostics market in 2022.

FUJIFILM Holdings Corp, Heska Corp, Idexx Laboratories Inc, INDICAL BIOSCIENCE GmbH, Merck Animal Health, Neogen Corp, Randox Laboratories Ltd, Thermo Fisher Scientific Inc, Virbac SA, and Zoetis Inc are some of the leading companies operating in the Europe veterinary diagnostics market.

1. FUJIFILM Holdings Corp

2. Heska Corp

3. Idexx Laboratories Inc

4. INDICAL BIOSCIENCE GmbH

5. Merck Animal Health

6. Neogen Corp

7. Randox Laboratories Ltd

8. Thermo Fisher Scientific Inc

9. Virbac SA

10. Zoetis Inc

The Europe Veterinary Diagnostics Market is valued at US$ 1,064.37 Million in 2022, it is projected to reach US$ 1,874.97 Million by 2030.

As per our report Europe Veterinary Diagnostics Market, the market size is valued at US$ 1,064.37 Million in 2022, projecting it to reach US$ 1,874.97 Million by 2030. This translates to a CAGR of approximately 7.3% during the forecast period.

The Europe Veterinary Diagnostics Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Veterinary Diagnostics Market report:

The Europe Veterinary Diagnostics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Europe Veterinary Diagnostics Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Europe Veterinary Diagnostics Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Europe Veterinary Diagnostics Market

Get Free Sample For Europe Veterinary Diagnostics Market