Europe Smart Hospital Beds Market

According to the United Nations, the global median age has changed notably in the last few decades; it increased from 24 in 1950 to 31 in 2020. This indicates that there has been a rise in the elderly population, along with the overall population, in every country. According to the World Health Organization (WHO) estimates published in October 2022, 1 in 6 people worldwide would be aged 60 or above by 2030; the number is further expected to surge from 1 billion in 2020 to 1.4 billion by 2030 and 2.1 billion by 2050. In addition, the number of people aged 80 and above is expected to reach 426 million by 2050.

According to Population Reference Bureau (PRB), Italy has 23% senior citizens followed by Finland, Portugal, and Greece, respectively, ranking among the top five European countries with the highest percentage of geriatric population. 22% of the total population in Finland, Portugal, and Greece, together, is geriatric population. Croatia, Greece, Italy, Malta, Portugal, Serbia, Slovenia, and Spain collectively accounted for 21% of the total elderly population in Europe.

The growing geriatric population can be associated with the growth of the Europe smart hospital beds market. These beds allow nurses and caregivers to take good care of elderly patients. Also, the demand for smart beds in homecare settings is soaring as installing smart beds in these setups helps reduce dependency on caregivers and nurses for changing positions of older patients on beds. Also, with smart beds, keeping a record of their vitals has become easier and simpler for caregivers.

The Europe smart hospital beds market in Europe has been sub-segmented into the UK, Germany, France, Italy, Spain, and the Rest of Europe. The surging geriatric population, innovations in smart hospital beds, increased government investments, and technological advancements in healthcare settings largely drive the market growth in this region. Germany has approximately 2,000 hospitals, 50% of which are public (30% of these are university hospitals) and the rest 50% are private. Germany is known for its healthcare engineering and technological performance for a long. Similarly, the rising prevalence of chronic diseases such as cardiovascular disease, diabetes, and cancer; and increasing geriatric population are the major factors driving the German Europe smart hospital beds market. The prevalence of diabetes is increasing among people of all ages in the country, majorly due to the growing overweight and obesity cases, unhealthy diets, and physical inactivity. According to the International Diabetes Federation (IDF) Europe, Germany recorded 7,476,800 cases of diabetes in 2021. Moreover, approximately 270,000 new cases are diagnosed each year. The percentage of the incidence of diabetes increases with growing age, and it is more in people above the age of 60.

According to Eurostat, among the EU Member States, Germany (12.8%) [as well as France (12.2%)] had the highest healthcare expenditure relative to GDP in 2020. The increasing demand for smart beds is due to the raised spending on healthcare, which empowers the country’s plans of technology adoption for the transformation of conventional health facilities into smart ones. Smart hospital beds help medical staff in their routine responsibilities, saving time and effort while maintaining the quality of medical service and patient care.

The Europe smart hospital beds market is segmented into patient weight, offering, application, end user, and country.

Based on patient weight, the Europe smart hospital beds market is segmented into less than 70 lb, 70 to 150 lb, 150 to 400 lb, 400 to 500 lb, and greater than 500 lb. The 400 to 500 lb segment held the largest share of the Europe smart hospital beds market in 2022.

Based on offering, the Europe smart hospital beds market is segmented into products & accessories, software & solutions, and services. The products & accessories segment held the largest share of the Europe smart hospital beds market in 2022.

Based on application, the Europe smart hospital beds market is segmented into fall prevention, pressure injury prevention, patient deterioration & monitoring, and others. The fall prevention segment held the largest share of the Europe smart hospital beds market in 2022.

Based on end user, the Europe smart hospital beds market is segmented into hospitals, clinics & nursing homes, ambulatory surgical centers, medical laboratories, long term care centers, and others. The hospitals segment held the largest share of the Europe smart hospital beds market in 2022.

Based on country, the Europe smart hospital beds market is segmented into the UK, Germany, France, Italy, Spain, and the Rest of Europe. Germany dominated the Europe smart hospital beds market in 2022.

Arjo AB, Favero Health Projects SpA, Hill-Rom Holdings Inc, Invacare Corp, LINET spol SRO, Malvestio SpA, Stiegelmeyer GmbH & Co. KG, and Stryker Corp are some of the leading companies operating in the Europe smart hospital beds market.

Strategic insights for the Europe Smart Hospital Beds provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 159.30 Million |

| Market Size by 2030 | US$ 455.57 Million |

| Global CAGR (2022 - 2030) | 14.0% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Patient Weight

|

| Regions and Countries Covered | Europe

|

| Market leaders and key company profiles |

The geographic scope of the Europe Smart Hospital Beds refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

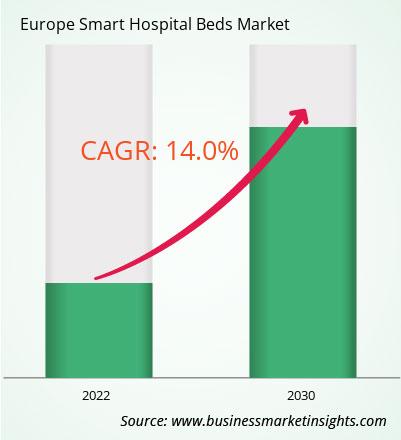

The Europe Smart Hospital Beds Market is valued at US$ 159.30 Million in 2022, it is projected to reach US$ 455.57 Million by 2030.

As per our report Europe Smart Hospital Beds Market, the market size is valued at US$ 159.30 Million in 2022, projecting it to reach US$ 455.57 Million by 2030. This translates to a CAGR of approximately 14.0% during the forecast period.

The Europe Smart Hospital Beds Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Smart Hospital Beds Market report:

The Europe Smart Hospital Beds Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Europe Smart Hospital Beds Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Europe Smart Hospital Beds Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Europe Smart Hospital Beds Market

Get Free Sample For Europe Smart Hospital Beds Market