Analysis - By Type [Polyimide (PI), Polybenzoxazole (PBO), Benzocylobutene (BCB), and Others] and Application {Fan-Out Wafer Level Packaging (FOWLP) and 2.5D/3D IC Packaging [High Bandwidth Memory (HBM), Multi-Chip Integration, Package on Package (FOPOP), and Others]}

No. of Pages:

108

|

Report Code:

TIPRE00026109

|

Category:

Chemicals and Materials

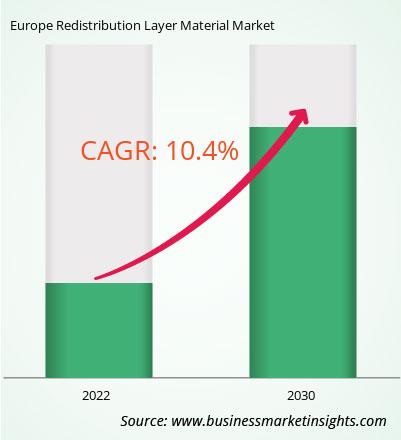

The Europe redistribution layer material market was valued at US$ 15.62 million in 2022 and is expected to reach US$ 34.45 million by 2030; it is estimated to grow at a CAGR of 10.4% from 2022 to 2030.

Advancements in the Packaging Technology Drive Europe Redistribution Layer Material Market

In the quest for cost reduction, the semiconductor industry has always been involved in developing innovative solutions. One approach currently considered by the leading semiconductor players is the migration from wafer and strip size to large-size panels dedicated to IC assembly. Efficiency and economies of scale are the added value of this path. Moving fan-out package manufacturing from a wafer, Fan-Out Wafer Level Packaging (FOWLP) to a large-scale panel, Fan-Out Panel Level Packaging (FOPLP), could be the solution for a wider adoption. As consumer electronics, automotive systems, and industrial devices become more compact and complex, there is a growing need for advanced semiconductor packaging technologies. Redistribution layers are integral to this process, it enables the creasing of smaller form factors, increases functionality and improves performance. Manufacturers in across the globe are positioned to capitalize on this trend by producing and supplying the necessary materials.

Advancements in the packaging industries, specifically the adoption of 2.5D and 3D packaging technologies, are poised to be significant drivers of the Europe redistribution layer material market. 2.5D and 3D packaging technologies significantly increase chip density and functionality. By stacking multiple semiconductors die on each other or side by side, these technologies allow for more robust and compact electronic devices. Redistribution layers are essential for creating interconnections between these stacked or adjacent dies, ensuring efficient data transfer and electrical connectivity.

These packaging technologies offer notable advantages in terms of improved performance and energy efficiency. With 2.5D and 3D packaging, shorter interconnect lengths and reduced signal paths contribute to faster data processing and lower power consumption. As a result, demand for redistribution layer materials capable of maintaining signal integrity and thermal management becomes even more crucial. Furthermore, the automotive industry is embracing 2.5D and 3D packaging to enable the integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies. These applications rely on tightly integrated, high-performance semiconductor packages that demand reliable redistribution layer materials.

Manufacturers across the globe are developing new packaging technologies. For instance, in May 2021, Samsung Electronics launched I-Cube4, for High-Performance Computing (HPC) to AI, 5G, cloud, and large data center, fast communication, and improving power efficiency between logic & memory through heterogeneous integration. In addition, in September 2023, Faraday Technology Corporation, an ASIC design service, and IP provider, announced the launch of its 2.5D/3D advanced package service. The 2.5D package technology is used for achieving the highest performance, targeting HPC such as AI accelerator, graph processing unit, and networking processor. Such advancements in packaging technology are expected to bolster the Europe redistribution layer material market growth.

Europe Redistribution Layer Material Market Overview

Europe has a wide presence of major manufacturing industries such as aerospace, machinery & equipment, automotive, shipbuilding, and military vehicles. The automotive industry of the EU is considered to be a crucial industry as it significantly contributes to the region's GDP. EU is the leading producer of motor vehicles across the globe, and many premium automotive manufacturers such as BMW, Volkswagen are based in the region. In the region, the vehicle manufacturing sector produces ~19.2 million cars, vans, buses, and trucks per year. Approximately 300 vehicle assembly and manufacturing facilities are located in ~26 countries across the region. According to the European Automobile Manufacturers' Association (ACEA), 21% of the cars across the world are manufactured in the EU by companies such as BMW, Volkswagen, Audi, and Aston Martin. Germany holds the largest share of the automotive market in the region, i.e., 30%. The rapid inclination of automotive manufacturers to include automotive electronics due to the emergence of autonomous driving and advanced driver-assist systems has resulted in increased demand for electronic integrations in automobiles. This factor propels the demand for semiconductor materials, including redistribution layer materials.

BYD Auto Co., Ltd, China, announced its plan in 2021 to establish a battery production plant in Europe. Furthermore, Hungary and the Czech Republic are among the key export markets for semiconductors owing to the presence of several electronic equipment manufacturers. With the growing demand for electronic equipment in Europe, the adoption of semiconductor packaging technology is also increasing. The 5G for Europe Action Plan of the EC is a blueprint for private as well as public investment in 5G infrastructure in the EU. The blueprint enumerates measures to ensure a synchronized approach among all EU Member States to make 5G available to all citizens by the end of 2020. This plan has propelled the Europe redistribution layer material market growth across Europe. Additionally, manufacturers are working on projects to launch highly efficient packaging of larger chips. For instance, in Germany, Fraunhofer IZM is leading a project to improve Fan-Out Panel Level Packaging technology for packaging larger chips with higher efficiency. Also, as a part of advanced packaging, the fan-out solutions are likely to become critical for boosting device performance and bandwidth. This factor is encouraging semiconductor players, R&D organizations, and chipmakers to promote the development of fan-out packaging solutions. All the above mentioned factors are anticipated to support the growth of the Europe redistribution layer material market during the forecast period.

Europe Redistribution Layer Material Market Revenue and Forecast to 2030 (US$ Million)

Europe Redistribution Layer Material Market Segmentation

The Europe redistribution layer material market is segmented based on type, application, and country.

Based on type, the Europe redistribution layer material market is segmented into polyimide (PI), polybenzoxazole (PBO), benzocylobutene (BCB), and others. The polyimide (PI) segment held the largest share in 2022.

By application, the Europe redistribution layer material market is segmented into fan-out wafer level packaging (FOWLP) and 2.5D/3D IC packaging. The 2.5D/3D IC packaging segment held the largest share in 2022. The 2.5D/3D IC packaging is further subsegmented into high bandwidth memory (HBM), multi-chip integration, package on package (FOPOP), and others.

Based on country, the Europe redistribution layer material market is segmented into Germany, Austria, Italy, and the Rest of Europe. Germany dominated the Europe redistribution layer material market in 2022.

SK Hynix Inc, Samsung Electronics Co Ltd, Infineon Technologies AG, DuPont de Nemours Inc, FUJIFILM Holdings Corp, Amkor Technology Inc, ASE Technology Holding Co Ltd, NXP Semiconductors NV, JCET Group Co Ltd, and Shin-Etsu Chemical Co Ltd are some of the leading companies operating in the Europe redistribution layer material market.

Europe Redistribution Layer Material Strategic Insights

Strategic insights for the Europe Redistribution Layer Material provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

Get more information on this report

Europe Redistribution Layer Material Report Scope

Report Attribute

Details

Market size in 2022

US$ 15.62 Million

Market Size by 2030

US$ 34.45 Million

Global CAGR (2022 - 2030)

10.4%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Type

Polyimide

Polybenzoxazole

Benzocylobutene

By Application

Fan-Out Wafer Level Packaging

2.5D/3D IC Packaging

Regions and Countries Covered

Europe

UK

Germany

France

Russia

Italy

Rest of Europe

Market leaders and key company profiles

Amkor Technology Inc

ASE Technology Holding Co Ltd

DuPont de Nemours Inc

FUJIFILM Holdings Corp

Infineon Technologies AG

JCET Group Co Ltd

NXP Semiconductors NV

Samsung Electronics Co Ltd

Shin-Etsu Chemical Co Ltd

SK Hynix Inc

Get more information on this report

Europe Redistribution Layer Material Regional Insights

The geographic scope of the Europe Redistribution Layer Material refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Europe Redistribution Layer Material Market

1. Amkor Technology Inc

2. ASE Technology Holding Co Ltd

3. DuPont de Nemours Inc

4. FUJIFILM Holdings Corp

5. Infineon Technologies AG

6. JCET Group Co Ltd

7. NXP Semiconductors NV

8. Samsung Electronics Co Ltd

9. Shin-Etsu Chemical Co Ltd

10. SK Hynix Inc

Frequently Asked Questions

How big is the Europe Redistribution Layer Material Market?

The Europe Redistribution Layer Material Market is valued at US$ 15.62 Million in 2022, it is projected to reach US$ 34.45 Million by 2030.

What is the CAGR for Europe Redistribution Layer Material Market by (2022 - 2030)?

As per our report Europe Redistribution Layer Material Market, the market size is valued at US$ 15.62 Million in 2022, projecting it to reach US$ 34.45 Million by 2030. This translates to a CAGR of approximately 10.4% during the forecast period.

What segments are covered in this report?

The Europe Redistribution Layer Material Market report typically cover these key segments-

Type (Polyimide, Polybenzoxazole, Benzocylobutene)

Application (Fan-Out Wafer Level Packaging, 2.5D/3D IC Packaging)

What is the historic period, base year, and forecast period taken for Europe Redistribution Layer Material Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Redistribution Layer Material Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2030

Who are the major players in Europe Redistribution Layer Material Market?

The Europe Redistribution Layer Material Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Amkor Technology Inc

ASE Technology Holding Co Ltd

DuPont de Nemours Inc

FUJIFILM Holdings Corp

Infineon Technologies AG

JCET Group Co Ltd

NXP Semiconductors NV

Samsung Electronics Co Ltd

Shin-Etsu Chemical Co Ltd

SK Hynix Inc

Who should buy this report?

The Europe Redistribution Layer Material Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Redistribution Layer Material Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Redistribution Layer Material Market

1. Complete the form

2. Check your inbox (and spam/junk folder)

3. Your Personal Data is Secure with us

GDPR + CCPA Compliant

Personal & transactional information is kept safe from unauthorized use.

WHAT'S INCLUDED IN FULL REPORT : Market Dynamics,

Competitive Analysis and Assessment, Define Business Strategies, Market Outlook and

Trends, Market Size and Share Analysis, Growth Driving Factors, Future Commercial

Potential, Identify Regional Growth Engines

Get Free Sample For Europe Redistribution Layer Material Market

Get Free Sample For Europe Redistribution Layer Material Market