Europe Industrial Automation Market

Machine vision users and systems integrators have exploited better imaging, optics, illumination, and software for nearly 40 years. Even though machine vision is a somewhat mature technology, lower component, software, and engineering costs and increased simplicity of use and application expansion continue to drive machine vision acceptance across industries.

In 2021, due to the COVID-19 pandemic, manufacturers accelerated the deployment of machine vision technology for industrial automation to keep operations running as effectively as possible and keep up with the increasing demand as businesses scrambled to bolster digital infrastructure, supporting remote workers.

Additionally, logistics-related apps experienced a rise due to a surge in online purchase volumes. Imaging systems in retail distribution centers and automated warehouse storage and retrieval systems, and manufacturers of PPE-related items, such as face masks, face shields, protective garments, and respirators were among them. Other factors influencing the uptake of machine vision systems for industrial automation include predictive maintenance, packaging inspection, automated barcode reading, product and component assembly, defect reduction, and 3D vision inspection.

Moreover, the rise in investment by companies to develop new products through machine vision technology for industrial automation is further propelling the market. For instance, in January 2022, the Khronos Group launched a new initiative with the European Machine Vision Alliance (EMVA) to produce an open, royalty-free API standard to regulate camera system runtimes in embedded, mobile, industrial, XR, automotive, and scientific industries. Thus, the rise in investments by companies is boosting the uptake of machine vision systems for industrial automation.

Europe is one of the early adopters of robotics systems across manufacturing facilities. Furthermore, the ongoing developments in IoT-based technologies are propelling the adoption of robots in the region. The European Commission (EC) is primarily focusing on R&D funding in automation to boost the competitiveness of its manufacturing sector and continue dominance in global technological leadership. EC sanctioned a budget of US$ 780 million for R&D in robotics and other technologies, such as AI and Cobots, from 2018 to 2020.

The automotive sector invests extensively in new production capabilities and the industry 4.0 infrastructure. The automotive sector is a leading end-use industry for robotic applications, accounting for half of the robot shipments in Europe. Automotive assembly automation involves streamlining repetitive processes, such as material handling, welding, and assembling auto body components. Automotive manufacturers can save on rework and labor costs and improve quality and repeatability with vision, robotics, and software integration. Europe is home to many prominent car manufacturers, including BMW, Volkswagen, Renault, and Peugeot. Thus, the robust automotive industry is boosting the adoption of automated solutions in the region, which is driving the market growth.

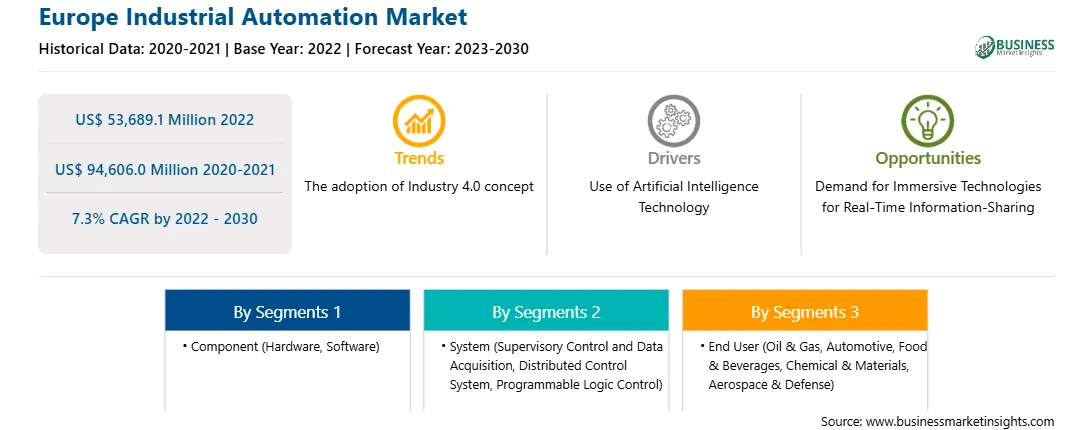

The Europe industrial automation market is segmented into component, system, end user, and country.

Based on component, the Europe industrial automation market is segmented into hardware and software. The hardware segment held a larger share of the Europe industrial automation market in 2022. The hardware is further sub segmented into motors and drives, robots, sensors, machine vision systems, and others.

Based on system, the Europe industrial automation market is segmented into supervisory control and data acquisition, distributed control system, programmable logic control, and other. The distributed control system segment held the largest share of the Europe industrial automation market in 2022.

Based on end user, the Europe industrial automation market is segmented into oil & gas, automotive, food & beverage, chemical & materials, aerospace & defense, and others. The automotive segment held the largest share of the Europe industrial automation market in 2022.

Based on country, the Europe industrial automation market is segmented into France, Germany, the UK, Italy, Russia, and the Rest of Europe. Germany dominated the Europe industrial automation market in 2022.

ABB Ltd, Bosch Rexroth AG, Emerson Electric Co, Hitachi Ltd, Honeywell International Inc, Mitsubishi Electric Corp, OMRON Corp, Rockwell Automation Inc, Schneider Electric SE, and Siemens AG are some of the leading companies operating in the Europe industrial automation market.

Strategic insights for the Europe Industrial Automation provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 53,689.1 Million |

| Market Size by 2030 | US$ 94,606.0 Million |

| Global CAGR (2022 - 2030) | 7.3% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Component

|

| Regions and Countries Covered | Europe

|

| Market leaders and key company profiles |

The geographic scope of the Europe Industrial Automation refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

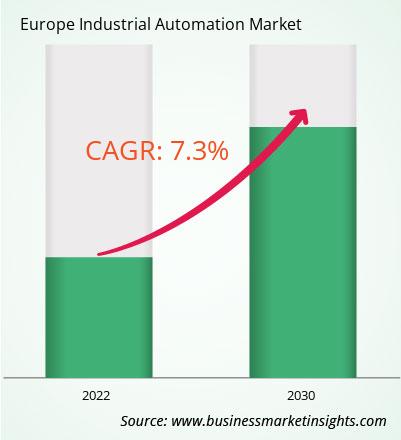

The Europe Industrial Automation Market is valued at US$ 53,689.1 Million in 2022, it is projected to reach US$ 94,606.0 Million by 2030.

As per our report Europe Industrial Automation Market, the market size is valued at US$ 53,689.1 Million in 2022, projecting it to reach US$ 94,606.0 Million by 2030. This translates to a CAGR of approximately 7.3% during the forecast period.

The Europe Industrial Automation Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Industrial Automation Market report:

The Europe Industrial Automation Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Europe Industrial Automation Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Europe Industrial Automation Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Europe Industrial Automation Market

Get Free Sample For Europe Industrial Automation Market