Europe Gas Pipeline Infrastructure Market

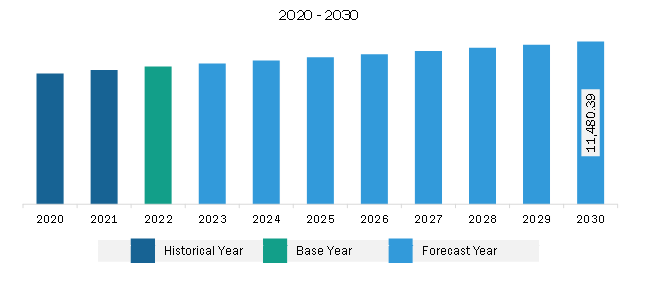

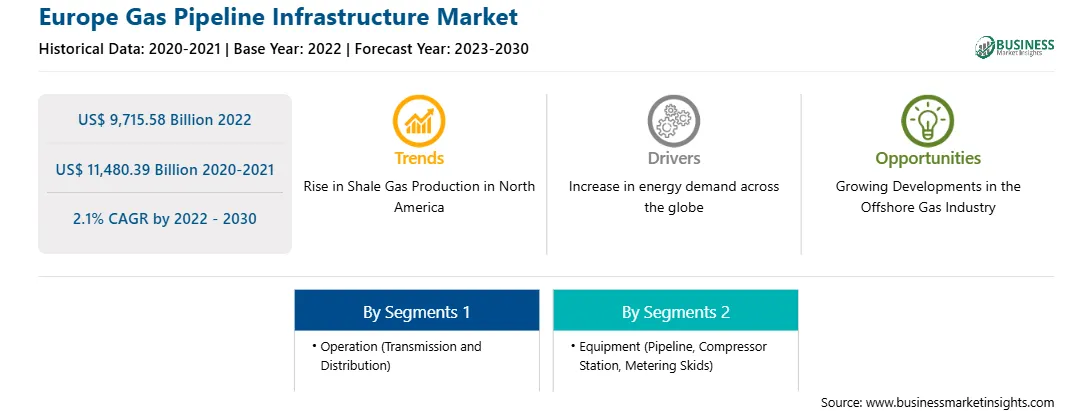

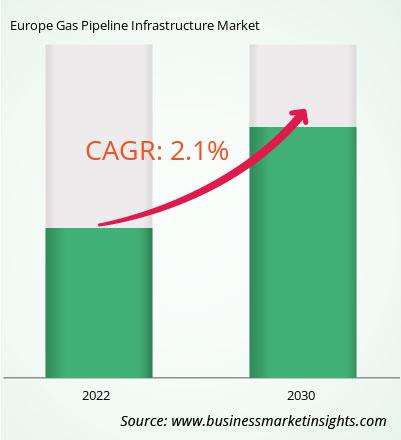

The Europe gas pipeline infrastructure market is expected to grow from US$ 9,715.58 billion in 2022 to US$ 11,480.39 billion by 2030. It is estimated to record a CAGR of 2.1% from 2022 to 2030. Integration with Renewable Energy Drives Europe Gas Pipeline Infrastructure Market

Integration with renewable energy involves leveraging natural gas pipelines to support the intermittent nature of renewable sources such as solar and wind power. This integration offers opportunities for pipeline operators to collaborate with renewable energy developers and invest in infrastructure that complements renewable energy generation. For example, gas-fired power plants can provide backup and grid stability during periods of low renewable energy output, reducing reliance on fossil fuels and carbon emissions. Additionally, advancements in technologies like power-to-gas allow excess renewable energy to be converted into hydrogen or synthetic natural gas, which can be stored in pipelines for later use. By integrating natural gas pipelines with renewable energy sources, companies can contribute to decarbonization efforts, enhance energy security, and support the transition to a more sustainable energy system.Europe Gas Pipeline Infrastructure Market Overview

Russia, Germany, France, and Spain are some of the major countries aiding to the overall growth of the gas pipeline infrastructure market in Europe. The government policies and mandates in line with the net zero carbon emission and clean energy targets are creating the demand for sustainable infrastructure, including gas pipeline networks. In the European Union, the carbon dioxide ratio in the power sector intensified substantially in 2022. A few countries resumed operations at coal-driven power plants, while outages at nuclear plants and low hydropower production fueled the dependability of natural gas. In line with the Paris Agreement, which involved 196 participants at the UN Climate Change Conference (COP21) in Paris, France, in 2015-the government is establishing net zero emission and green energy policies. The growing share of low-carbon emission energy resources in the power mix and the industrial sector are major driving factors for the gas pipeline infrastructure market in the region. The development of new pipeline infrastructure and the advancement of the capacity of existing gas pipelines are also likely to fuel the growth of the gas pipeline infrastructure market in Europe over the forecast period. Germany experienced slow growth in gas production until the end of 2022 due to the scarcity of gas resources across the country's mining areas. The country relies majorly on imports from different countries, such as the US, Italy, the UK, and Norway. It imports approximately 70% of its energy requirements as its domestic production caters to only ~6% of its gas consumption. In 2023, the governments of Germany and Italy collaborated to form a projected gas pipeline. The proposed pipeline is a 3,300 km project and is anticipated to incorporate four European transmission system operators, including Trans Austria Gasleitung, Snam, Bayernets, and Gas Connect Austria in Germany. Thus, the development of the new pipeline and maintenance of the existing gas network is anticipated to boost the development of gas pipeline infrastructure in Germany over the forecast period.

Europe Gas Pipeline Infrastructure Market Revenue and Forecast to 2030 (US$ Billion)

Strategic insights for the Europe Gas Pipeline Infrastructure provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market. The geographic scope of the Europe Gas Pipeline Infrastructure refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas. Get more information on this report

Get more information on this report Europe Gas Pipeline Infrastructure Strategic Insights

Get more information on this report

Get more information on this report Europe Gas Pipeline Infrastructure Report Scope

Report Attribute

Details

Market size in 2022

US$ 9,715.58 Billion

Market Size by 2030

US$ 11,480.39 Billion

Global CAGR (2022 - 2030)

2.1%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Operation

By Equipment

Regions and Countries Covered

Europe

Market leaders and key company profiles

Get more information on this report Europe Gas Pipeline Infrastructure Regional Insights

Get more information on this report

Get more information on this report

Europe Gas Pipeline Infrastructure Market Segmentation

The Europe gas pipeline infrastructure market is segmented into operation, equipment, application, and country.

Based on operation, the Europe gas pipeline infrastructure market is bifurcated into transmission and distribution. The distribution segment held a larger share of Europe gas pipeline infrastructure market in 2022.

In terms of equipment, the Europe gas pipeline infrastructure market is categorized into pipeline, compressor station, metering skids, and valves. The pipeline segment held the largest share of Europe gas pipeline infrastructure market in 2022.

Based on application, the Europe gas pipeline infrastructure market is bifurcated into onshore and offshore. The onshore segment held a larger share of Europe gas pipeline infrastructure market in 2022.

Based on country, the Europe gas pipeline infrastructure market is segmented into Germany, France, Italy, Spain, Russia, the UK, and the Rest of Europe. The Rest of Europe dominated the Europe gas pipeline infrastructure market in 2022.

Enbridge Inc, Berkshire Hathaway Inc, Kinder Morgan Inc, Beltps, Enagas SA, and Saipem SpA are some of the leading companies operating in the Europe gas pipeline infrastructure market.

1. Enbridge Inc

2. Berkshire Hathaway Inc

3. Kinder Morgan Inc

4. Beltps

5. Enagas SA

6. Saipem SpA

The Europe Gas Pipeline Infrastructure Market is valued at US$ 9,715.58 Billion in 2022, it is projected to reach US$ 11,480.39 Billion by 2030.

As per our report Europe Gas Pipeline Infrastructure Market, the market size is valued at US$ 9,715.58 Billion in 2022, projecting it to reach US$ 11,480.39 Billion by 2030. This translates to a CAGR of approximately 2.1% during the forecast period.

The Europe Gas Pipeline Infrastructure Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Gas Pipeline Infrastructure Market report:

The Europe Gas Pipeline Infrastructure Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Europe Gas Pipeline Infrastructure Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Europe Gas Pipeline Infrastructure Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Europe Gas Pipeline Infrastructure Market

Get Free Sample For Europe Gas Pipeline Infrastructure Market