Europe Edge Computing Market

The advent of IoT has enabled more than millions of devices to be connected over the internet. The proliferation of IoT has led to a significant surge in data, due to which industries increasingly rely on centralized cloud computing and storage solutions. Edge computing is on the location where data is collected or used, allowing IoT data to be gathered and processed at the edge rather than sending the data back to a datacenter or cloud. This exponential growth in data traffic over the internet is attributed to the growing penetration of smartphones and other consumer electronic devices that can be connected over the internet due to the growing popularity of IoT. A few advantages of edge computing, including efficient data management, low connectivity costs, and better security practices, accelerate its usage across industries such as automotive, agriculture, oil & gas, healthcare and among other industries.

Strong internet infrastructural deployments in the advanced countries coupled with the rolling out of advanced infrastructures, such as 5G and fiber optic cables, enable the establishment of new use cases, such as Fixed Wireless Access, Massive IoT, and Critical IoT. Such advancements in internet technology are driving individuals and businesses to harness the best out of the presented opportunity and maximize the revenue generation streams. Additionally, the government initiatives toward the digitalization of economies is leading to the exponential growth of data traffic over the internet in various countries and also on a Europe scale for other developing economies.

The edge computing market in Europe is segmented into Germany, France, Italy, the UK, Russia, and the Rest of Europe. Germany, the UK, and the Netherlands are leading adopters of IoT in the region, wherein IoT is being primarily implemented in the manufacturing, residential, health, and finance sectors. Although the retail and agriculture sectors slightly lag behind these sectors in terms of IoT adoption, they are perceived to emerge as prime consumers of IoT devices in the coming years. IoT is closely associated with big data, Machine Learning (ML), 5G connectivity, and artificial intelligence (AI). The higher bandwidths associated with the 5G network allow the connection of a greater number of devices to the Internet, which, in turn, results in the generation of greater data volumes and requirements for better processing capacities. As data availability continues to increase with the growing popularity of ML and AI, the edge computing market would continue to grow at a notable pace. Under the Digital Europe program, the European Commission is investing in the deployment of common European data spaces for sectors such as agriculture, energy, healthcare, manufacturing, and transport to ensure that more data becomes available for use across European economies and societies, along with regulating the companies and individuals generating these data.

Strategic insights for the Europe Edge Computing provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 12,221.47 Million |

| Market Size by 2028 | US$ 37,651.59 Million |

| Global CAGR (2022 - 2028) | 20.6% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Component

|

| Regions and Countries Covered | Europe

|

| Market leaders and key company profiles |

The geographic scope of the Europe Edge Computing refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

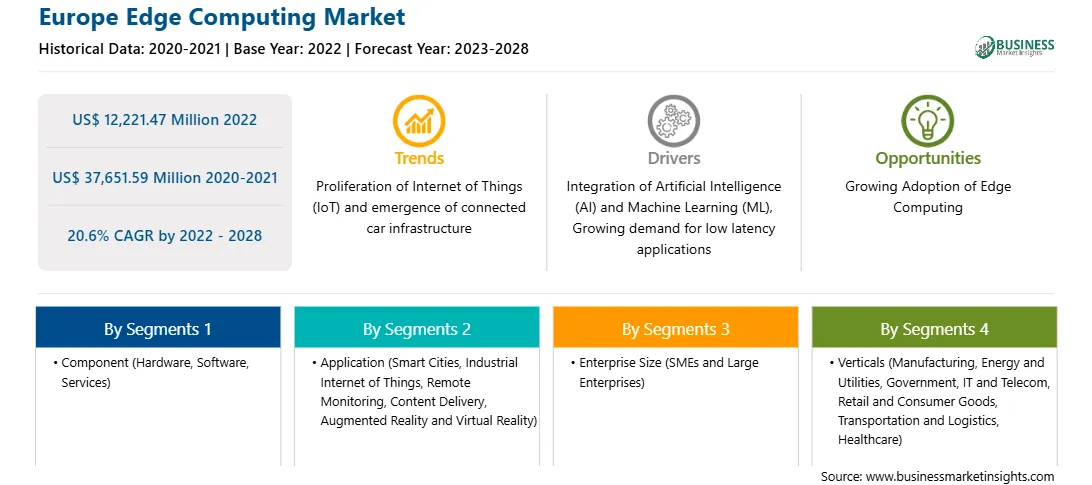

The Europe edge computing market is segmented into component, applications, enterprise size, verticals, and country.

Based on component, the Europe edge computing market is segmented into hardware, software, and services. The hardware segment registered the largest Europe edge computing market share in 2022.

Based on organization Size, the Europe edge computing market is segmented into SMEs and large enterprises. The large enterprises segment held a larger Europe edge computing market share in 2022.

Based on application, the Europe edge computing market is segmented into smart cities, industrial internet of things (IIOT), remote monitoring, content delivery, augmented reality and virtual reality, and others. The smart cities segment held the largest Europe edge computing market share in 2022.

Based on verticals, the Europe edge computing market is segmented into manufacturing, energy and utilities, government, IT and telecom, retail and consumer goods, transportation and logistics, healthcare, and others. The IT and telecom segment held the largest Europe edge computing market share in 2022.

Based on country, the Europe edge computing market has been categorized into the Germany, France, Italy, the UK, Russia, and the Rest of Europe. The UK dominated the Europe edge computing market share in 2022.

ADLINK Technology Inc; Amazon Web Services; Dell Technologies; EdgeConnex Inc.; Hewlett Packard Enterprise Development LP (HPE); IBM Corporation; and Microsoft Corporation are the leading companies operating in the Europe edge computing market.

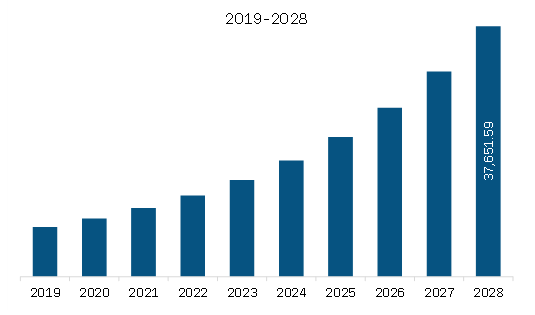

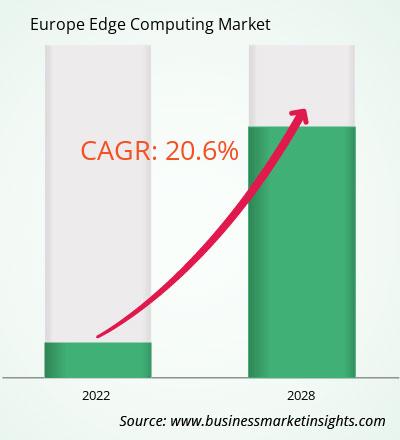

The Europe Edge Computing Market is valued at US$ 12,221.47 Million in 2022, it is projected to reach US$ 37,651.59 Million by 2028.

As per our report Europe Edge Computing Market, the market size is valued at US$ 12,221.47 Million in 2022, projecting it to reach US$ 37,651.59 Million by 2028. This translates to a CAGR of approximately 20.6% during the forecast period.

The Europe Edge Computing Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Edge Computing Market report:

The Europe Edge Computing Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Europe Edge Computing Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Europe Edge Computing Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Europe Edge Computing Market

Get Free Sample For Europe Edge Computing Market