Asia Pacific Underwater Connector Market

The surging demand for bandwidth due to the emergence of 5G is the major factor driving the Asia Pacific underwater connector market. Internet bandwidth usage has been experiencing consistent growth in recent years. According to the data published by the International Telecommunications Union (ITU), the fixed broadband download speed [measured in megabits per second (Mb/s)] has significantly improved in Asia Pacific in the last decade. In Asia Pacific, the average number of fixed-broadband subscriptions with at least 10 Mb/s download speed increased from 2 million subscriptions in 2010 to 154 million subscriptions in 2019. In addition, the release of internet speed test data from Ookla in 2020 enabled more demand for higher speed in Asia Pacific. As the majority of the world’s population suddenly shifted to work from home due to the pandemic, e-learning and virtual communications increased dramatically, which increased fixed and mobile network use. Data-intensive applications, such as online gaming and video streaming, grew by 75% and 32% in the first quarter and second quarter of 2020, significantly contributing to network traffic. Thus, this expansion of broadband networks fueled the demand for connectors. For instance, The Economic and Social Commission for Asia and the Pacific (ESCAP), supported by regional cooperation, promoted digital cooperation and inclusive digitalization through the Asia Pacific Information Superhighway (AP-IS) Platform. The AP-IS Master Plan 2019–2022 has been implemented to promote digital cooperation and digital development with a focus on four pillars—connectivity (promoting fiber-optic broadband network expansion throughout the region), e-resilience (boosting ICT network resilience to support effective disaster management), Internet traffic and network management (strengthening of efficient traffic and network management for Internet reliability and redundancy), and broadband for all (promoting affordable broadband access for all). Thus, the growing trend of the adoption of high bandwidth due to the emergence of the 5G network is expected to positively impact the growth of the underwater connector market during the forecasted period.

With the new features and technologies, vendors can attract new customers and expand their footprints in emerging markets. This factor is likely to drive the Asia Pacific underwater connector market. The Asia Pacific underwater connector market is expected to grow at a good CAGR during the forecast period.

Strategic insights for the Asia Pacific Underwater Connector provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

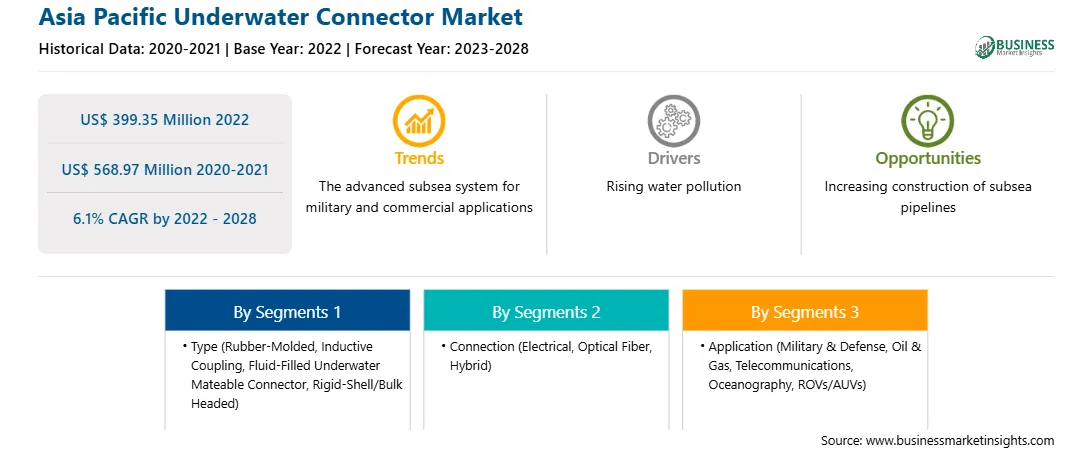

| Market size in 2022 | US$ 399.35 Million |

| Market Size by 2028 | US$ 568.97 Million |

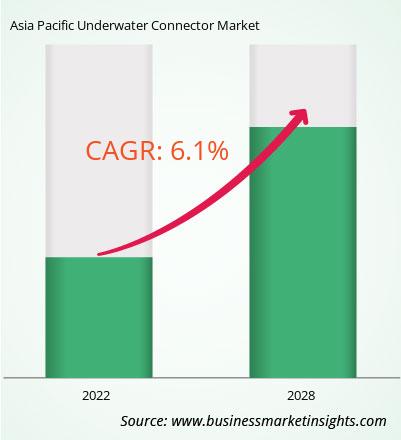

| Global CAGR (2022 - 2028) | 6.1% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Type

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Underwater Connector refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The North America underwater connector market is segmented into type, connection, application, and country.

In terms of connection, the North America underwater connector market is segmented into electrical, optical fiber, and hybrid. The electrical segment dominated the market in 2022.

Fischer Connectors SA, Gisma Steckverbinder GmbH, Glenair, Hydro Group Plc., TE Connectivity, and Teledyne Marine are among the leading companies operating in the Asia Pacific underwater connector market.

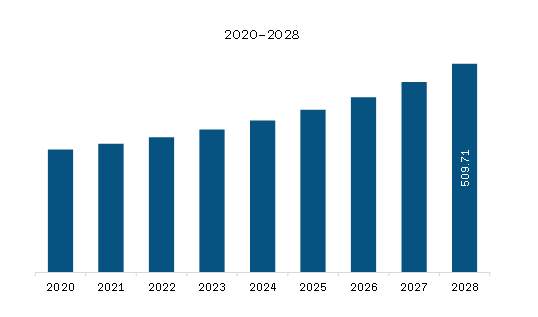

The Asia Pacific Underwater Connector Market is valued at US$ 399.35 Million in 2022, it is projected to reach US$ 568.97 Million by 2028.

As per our report Asia Pacific Underwater Connector Market, the market size is valued at US$ 399.35 Million in 2022, projecting it to reach US$ 568.97 Million by 2028. This translates to a CAGR of approximately 6.1% during the forecast period.

The Asia Pacific Underwater Connector Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Underwater Connector Market report:

The Asia Pacific Underwater Connector Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Underwater Connector Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Underwater Connector Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Underwater Connector Market

Get Free Sample For Asia Pacific Underwater Connector Market