Asia Pacific Space Situational Awareness (SSA) Market

As per the International Astronomical Union (IAU), a satellite constellation consists of a number of satellites that are similar in type, function, and design in complementary orbits for a shared purpose under shared control. Satellite constellations have applications such as navigation and geodesy, satellite telephony, and Earth observation. Companies are planning large-scale satellite constellations in LEO and mid-Earth orbits to provide Internet of Things (IoT) or satellite internet to connect machines and systems directly. As per IAU, a constellation with thousands of individual units at low altitudes can reduce signal latency while maintaining high levels of coverage, especially in remote areas without developed ground infrastructure. Currently, nearly 2,000 active satellites are orbiting the Earth and the number is expected to increase manifold, as there are several planned satellite constellation deployments in the coming decades. In March 2023, OneWeb confirmed the successful deployment and contact of 40 satellites launched by a SpaceX vessel. The deployment led to a total count of 582 satellites in the company's constellation. The company anticipates being just one mission away from completing its Gen 1 constellation, after which it can activate its region broadband service. Elon Musk owned SpaceX has already built a network of more than 3,500 satellites for its Starlink constellation, and the number is expected to increase in the coming years. In March 2023, China Satellite Network Group Corp and the Chinese government announced their plans to launch their first satellite for China's first satellite constellation by September 2023. In November 2021, France successfully deployed three military signals intelligence satellites through an Arianespace Vega rocket as part of its CapacitÉ de Renseignement Électromagnétique Spatiale (CERES) constellation. As interest progresses for satellite constellation, it will also create space congestion and a higher amount of space debris. Such trends are thus expected to promote the growth of the space situational awareness market in the future.

The expanding space development initiatives in Asia Pacific are creating a profound shift in the understanding of the cosmos, boosting national security, and offering vital information, goods, and services that further support innovation. The growing space development activities by the collaborative efforts of different countries, such as China, India, Japan, and South Korea are catalyzing the demand for space situational awareness, which is subsequently propelling the market growth in the region. One of the world’s largest space projects is run by China. It either conducts the most or the second most orbital launches each year.

Strategic insights for the Asia Pacific Space Situational Awareness (SSA) provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

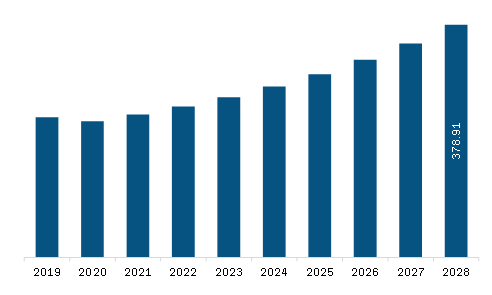

| Market size in 2022 | US$ 245.56 Million |

| Market Size by 2028 | US$ 378.91 Million |

| Global CAGR (2022 - 2028) | 7.5% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Offering

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Space Situational Awareness (SSA) refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Asia Pacific space situational awareness (SSA) market is segmented based on offering, object, end user, orbit range, and country. Based on offering, the Asia Pacific space situational awareness (SSA) market is bifurcated into software and services. The services segment held a larger market share in 2022.

Based on object, the Asia Pacific space situational awareness (SSA) market is segmented into mission-related debris, rocket bodies, fragmentation debris, functional spacecraft, and non-functional spacecraft. The fragmentation debris segment held the largest market share in 2022.

Based on source, the Asia Pacific space situational awareness (SSA) market is bifurcated into nuclear reactors and cyclotrons. The cyclotrons segment held a larger market share in 2022.

Based on end user, the Asia Pacific space situational awareness (SSA) market is bifurcated into commercial and government & military. The government & military segment held a larger market share in 2022.

Based on orbit range, the Asia Pacific space situational awareness (SSA) market is bifurcated into deep space and near earth. The near earth segment held a larger market share in 2022.

Based on country, the Asia Pacific space situational awareness (SSA) market is segmented into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific space situational awareness (SSA) market share in 2022.

Ansys Inc; GMV Innovating Solutions SL; L3Harris Technologies Inc.; Kratos Defense and Security Solutions Inc.; Lockheed Martin Corp; Parsons Corp; and Belcan LLC are the leading companies operating in the Asia Pacific space situational awareness (SSA) market.

1. Ansys Inc

2. ExoAnalytic Solutions Inc.

3. Globe Vision Inc.

4. GMV Innovating Solutions SL

5. L3Harris Technologies Inc.

6. Kratos Defense and Security Solutions Inc.

7. Lockheed Martin Corp

8. Parsons Corp

9. Belcan LLC

10. Spacenav LLC.

The Asia Pacific Space Situational Awareness (SSA) Market is valued at US$ 245.56 Million in 2022, it is projected to reach US$ 378.91 Million by 2028.

As per our report Asia Pacific Space Situational Awareness (SSA) Market, the market size is valued at US$ 245.56 Million in 2022, projecting it to reach US$ 378.91 Million by 2028. This translates to a CAGR of approximately 7.5% during the forecast period.

The Asia Pacific Space Situational Awareness (SSA) Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Space Situational Awareness (SSA) Market report:

The Asia Pacific Space Situational Awareness (SSA) Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Space Situational Awareness (SSA) Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Space Situational Awareness (SSA) Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Space Situational Awareness (SSA) Market

Get Free Sample For Asia Pacific Space Situational Awareness (SSA) Market