Analysis - By Type [Polyimide (PI), Polybenzoxazole (PBO), Benzocylobutene (BCB), and Others] and Application {Fan-Out Wafer Level Packaging (FOWLP) and 2.5D/3D IC Packaging [High Bandwidth Memory (HBM), Multi-Chip Integration, Package on Package (FOPOP), and Others]}

No. of Pages:

119

|

Report Code:

TIPRE00026108

|

Category:

Chemicals and Materials

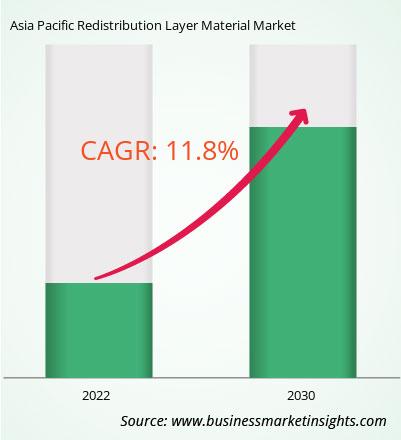

The Asia Pacific redistribution layer material market was valued at US$ 143.81 million in 2022 and is expected to reach US$ 351.93 million by 2030; it is estimated to grow at a CAGR of 11.8% from 2022 to 2030.

Increasing Demand from Automotive and Telecommunication Industries Drive Asia Pacific Redistribution Layer Material Market

The Asia Pacific redistribution layer material market is experiencing significant growth, driven primarily by the surging demand from two key industries: automotive and telecommunication.

The telecommunication sector is evolving rapidly, particularly with the deployment of 5G technology. There is a widespread rollout of 5G networks in across the globe, which has led to an increased demand for smartphones and other consumer electronics products. For instance, in October 2021, AIS and Samsung jointly launched a voice-over 5G radio service enabling voice calls on AIS's 5G standalone (SA) network in Thailand. In Vietnam, Samsung Electronics and Viettel announced the 5G commercial trials launched in Da Nang in December 2021. Viettel is piloting 5G services in 11 provinces and cities, namely, Ho Chi Minh City, Hanoi, Bac Ninh, Vinh Phuc, Bac Giang, Dong Nai, Ba Ria-Vung Tau, Binh Phuoc, Thua Thien-Hue, and Da Nang. In addition, according to Viavi Solutions Inc.'s report, over 92 countries across the world have launched 5G networks. A further 23 countries have underway pre-commercial 5G network trials, and 32 nations have announced their 5G rollout plans. The widespread rollout of 5G networks has led to an increased demand for smartphones and other consumer electronics products. This revolution is driving the development of high-frequency, high-performance devices and systems. These requirements extend to the material used in redistribution layers, which must meet stringent specifications to ensure seamless connectivity and signal integrity. In addition, the push for miniaturization is a common thread between these industries. This revolution is driving the development of high-frequency, high-performance devices and systems. These requirements extend to the material used in redistribution layers, which must meet stringent specifications to ensure seamless connectivity and signal integrity. In addition, the push for miniaturization is a common thread between these industries. Smaller, more powerful devices are in demand, necessitating thinner and more advanced redistribution layer materials. These materials play a critical role in enabling high-density interconnections within compact electronic packages.

The ever-expanding production needs of the automotive industry propel the growth of the market. According to the ISEAS-Yusof Ishak Institute, Southeast Asia is also an important automobile production base. Southeast Asia is the seventh largest automotive manufacturing hub worldwide, producing 3.5 million vehicles in 2021. Within the region, Thailand is the largest car producer, producing over 1.6 million motor vehicles in 2021, followed by Indonesia (1.1 million), Malaysia (0.48 million), and Vietnam (0.16 million). In addition, as per the data of the Organisation Internationale des Constructeurs d'Automobiles (OICA), countries in North America, South America, and Central America recorded production of over 16.1 million commercial & passenger cars in 2021, and the production has grown by 10% and registered over 17.7 million commercial & passenger car production in 2022. Numerous companies operating in the automotive market are investing heavily in automobile manufacturing to increase production and sales. In July 2021, Maruti Suzuki India Ltd. announced an investment worth US$ 2.42 billion in a new manufacturing facility in Haryana, India. The facility is expected to manufacture 1 million units annually. As vehicles become increasingly reliant on advanced electronics for safety, entertainment, and autonomous capabilities, the demand for semiconductors has soared. These automotive chips require intricate packaging solutions, often employing redistribution layers, to enable compact design and efficient interconnections.

The economic growth of the automotive and telecommunications sectors across the globe has a ripple effect on the entire supply chain. Investments in research and development, technology, and infrastructure are increasing, fostering an environment conducive to innovation and development in the field of redistribution layer materials. This trend is characterized by increased production, advanced packaging technologies, miniaturization requirements, the region's strategic supply chain position, and a positive economic impact on the entire ecosystem. These factors collectively propel the Asia Pacific redistribution layer material market.

Asia Pacific Redistribution Layer Material Market Overview

Many developing countries in Asia Pacific are witnessing significant growth in their manufacturing sectors. The region is considered a global manufacturing hub owing to the presence of diverse manufacturing industries. With China's evolution into a high-skilled manufacturing hub, developing countries such as India, South Korea, Taiwan, and Vietnam are attracting several businesses that plan to relocate their low to medium-skilled manufacturing facilities to neighboring countries, which results in reduced labor costs. As per the study by the Semiconductor Industry Association, ~75% of global semiconductor capacity is based in East Asia. Semiconductor companies will benefit from a cost advantage of 25% to 50% with the start of manufacturing activities in the region.

Further, governments of various countries in Asia Pacific are working to improve investment plans regarding semiconductor manufacturing. They are offering tax rebates, funds, and subsidies, among others, to attract manufacturing companies to set up plants in their respective countries. Further, several governments have taken initiatives such as Made in China 2025 and Make in India to propel the growth of the manufacturing sector. However, China, which is the largest manufacturing hub, is experiencing a rise in the country's labor cost owing to the rise in the aging population of the country. This has resulted in manufacturing companies investing in companies based in Southeast Asia. The improving infrastructure, rising domestic consumption, and reducing costs are a few factors attracting manufacturing companies.

The consumer electronics manufacturing industry in Asia Pacific is leading globally, which is anticipated to support the Asia Pacific redistribution layer material market across the region. Additionally, many countries across the region are increasingly adopting digital applications such as smart cities, autonomous vehicles, and IoT in a bid to become global powers.

The semiconductor manufacturing industry in Asia Pacific is the largest in the world. Ease of availability of raw materials for chip manufacturing, government incentives for the manufacturing sector, and inexpensive labor presence in APAC are a few factors driving the semiconductor manufacturing industries. RDL materials are directly sold to the semiconductor manufacturers as packaging is integral to semiconductor manufacturing processes. The growing penetration of consumer electronics, especially smartphones, is a major factor driving the revenues for the semiconductor industry. Also, owing to the rapid adoption of artificial intelligence and IoT in multiple business sectors, data center deployments in APAC are anticipated to grow in the coming years. The growth of network infrastructures is being strengthened with the rise in 5G deployments in various countries of APAC. All these factors are boosting the demand for sensors and other semiconductor-based devices.

The Industrial Revolution has transformed production in Australia, enabling improved productivity and increasing economic profit across the region. Thus, a rise in smart factories, value chain upgradation, data analytics, and connected machines are a few applications that require semiconductors. Furthermore, growing automation, 3D printing, and IoT, as well as emerging businesses, are accelerating the adoption of smart factories in Australia. The country's telecommunication industry contributes heavily to its GDP. The telco operators are seeking continued innovation for the implementation of advanced technologies such as 5G networks, which are projected to positively impact the use of RDL materials.

The large populations of China and India, including the expanding middle-class population in these countries, and well-established manufacturing sectors drive the semiconductor sector. China is the largest producer of passenger cars in the world; Japan, India, and South Korea are also major vehicle manufacturing countries in the region. The development of autonomous vehicles and smart infrastructure in Japan, China, and South Korea will further boost the demand for reliable semiconductor-based electronics devices. Countries such as Vietnam, Cambodia, and the Philippines plan to boost the production of semiconductors, thereby contributing to the revenue generation for the Asia Pacific redistribution layer material market. This factor is propelling the growth of semiconductor applications in the automotive sector in the region. Moreover, the region leads the consumer electronics manufacturing industry across the globe. Thus, the growing manufacturing activities in these industries is anticipated to boost the demand for semiconductors, which, in turn, is fueling the Asia Pacific redistribution layer material market across the region.

Exhibit: Asia Pacific Redistribution Layer Material Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Redistribution Layer Material Market Segmentation

The Asia Pacific redistribution layer material market is segmented based on type, application, and country.

Based on type, the Asia Pacific redistribution layer material market is segmented into polyimide (PI), polybenzoxazole (PBO), benzocylobutene (BCB), and others. The polyimide (PI) segment held the largest share in 2022.

By cooling fluid type, the Asia Pacific redistribution layer material market is segmented into fan-out wafer level packaging (FOWLP) and 2.5D/3D IC packaging. The 2.5D/3D IC packaging segment held a larger share in 2022. The 2.5D/3D IC packaging is further subsegmented into high bandwidth memory (HBM), multi-chip integration, package on package (FOPOP), and others.

Based on country, the Asia Pacific redistribution layer material market is segmented into China, Taiwan, Japan, South Korea, and the Rest of Asia Pacific. Taiwan dominated the Asia Pacific redistribution layer material market in 2022.

SK Hynix Inc, Samsung Electronics Co Ltd, Infineon Technologies AG, DuPont de Nemours Inc, FUJIFILM Holdings Corp, Amkor Technology Inc, ASE Technology Holding Co Ltd, NXP Semiconductors NV, JCET Group Co Ltd, and Shin-Etsu Chemical Co Ltd are some of the leading companies operating in the Asia Pacific redistribution layer material market.

Asia Pacific Redistribution Layer Material Strategic Insights

Strategic insights for the Asia Pacific Redistribution Layer Material provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

Get more information on this report

Asia Pacific Redistribution Layer Material Report Scope

Report Attribute

Details

Market size in 2022

US$ 143.81 Million

Market Size by 2030

US$ 351.93 Million

Global CAGR (2022 - 2030)

11.8%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Type

Polyimide

Polybenzoxazole

Benzocylobutene

By Application

Fan-Out Wafer Level Packaging

2.5D/3D IC Packaging

Regions and Countries Covered

Asia-Pacific

China

India

Japan

Australia

Rest of Asia-Pacific

Market leaders and key company profiles

SK Hynix Inc

Samsung Electronics Co Ltd

Infineon Technologies AG

DuPont de Nemours Inc

FUJIFILM Holdings Corp

Amkor Technology Inc

ASE Technology Holding Co Ltd

NXP Semiconductors NV

JCET Group Co Ltd

Shin-Etsu Chemical Co Ltd

Get more information on this report

Asia Pacific Redistribution Layer Material Regional Insights

The geographic scope of the Asia Pacific Redistribution Layer Material refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Asia Pacific Redistribution Layer Material Market

1. SK Hynix Inc

2. Samsung Electronics Co Ltd

3. Infineon Technologies AG

4. DuPont de Nemours Inc

5. FUJIFILM Holdings Corp

6. Amkor Technology Inc

7. ASE Technology Holding Co Ltd

8. NXP Semiconductors NV

9. JCET Group Co Ltd

10. Shin-Etsu Chemical Co Ltd

Frequently Asked Questions

How big is the Asia Pacific Redistribution Layer Material Market?

The Asia Pacific Redistribution Layer Material Market is valued at US$ 143.81 Million in 2022, it is projected to reach US$ 351.93 Million by 2030.

What is the CAGR for Asia Pacific Redistribution Layer Material Market by (2022 - 2030)?

As per our report Asia Pacific Redistribution Layer Material Market, the market size is valued at US$ 143.81 Million in 2022, projecting it to reach US$ 351.93 Million by 2030. This translates to a CAGR of approximately 11.8% during the forecast period.

What segments are covered in this report?

The Asia Pacific Redistribution Layer Material Market report typically cover these key segments-

Type (Polyimide, Polybenzoxazole, Benzocylobutene)

Application (Fan-Out Wafer Level Packaging, 2.5D/3D IC Packaging)

What is the historic period, base year, and forecast period taken for Asia Pacific Redistribution Layer Material Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Redistribution Layer Material Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2030

Who are the major players in Asia Pacific Redistribution Layer Material Market?

The Asia Pacific Redistribution Layer Material Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

SK Hynix Inc

Samsung Electronics Co Ltd

Infineon Technologies AG

DuPont de Nemours Inc

FUJIFILM Holdings Corp

Amkor Technology Inc

ASE Technology Holding Co Ltd

NXP Semiconductors NV

JCET Group Co Ltd

Shin-Etsu Chemical Co Ltd

Who should buy this report?

The Asia Pacific Redistribution Layer Material Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Asia Pacific Redistribution Layer Material Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Asia Pacific Redistribution Layer Material Market

1. Complete the form

2. Check your inbox (and spam/junk folder)

3. Your Personal Data is Secure with us

GDPR + CCPA Compliant

Personal & transactional information is kept safe from unauthorized use.

WHAT'S INCLUDED IN FULL REPORT : Market Dynamics,

Competitive Analysis and Assessment, Define Business Strategies, Market Outlook and

Trends, Market Size and Share Analysis, Growth Driving Factors, Future Commercial

Potential, Identify Regional Growth Engines

Get Free Sample For Asia Pacific Redistribution Layer Material Market

Get Free Sample For Asia Pacific Redistribution Layer Material Market