Asia Pacific Plastics for Composites Market

Mounting Demand for Lightweight Materials in Aerospace and Automotive Productions is Driving the Asia Pacific plastics for composites market

Advanced materials are crucial for boosting the fuel economy of modern automobiles while ensuring safety and performance. Since it takes less energy to accelerate lighter objects than heavier ones, lightweight materials offer excellent potential for increasing fuel efficiency. A 10% decrease in vehicle weight can result in a 6–8% improvement in fuel economy. Substituting cast iron and traditional steel components with lightweight materials such as high-strength steel, aluminum (Al) alloys, magnesium (Mg) alloys, carbon fiber, and polymer composites can reduce the weight of a vehicle body and chassis by up to 50%, thereby reducing the fuel consumption of a vehicle. The application of composites in the automotive sector is growing at a significant pace. In this sector, plastics are used in large quantities to produce composites. Plastic composites have excellent acoustic and thermal properties compared to composites of nonrenewable origin, which makes them ideal for vehicle interior parts. Moreover, they are suitable for the manufacturing of nonstructural interior components, including seat fillers, seat backs, headliners, interior panels, and dashboards. Therefore, a high demand for composites from the automotive industry for the manufacturing of fuel-efficient, lightweight vehicles drives the Asia Pacific plastics for composites market growth. The rising adoption of electric vehicles (EVs) is also driving the demand for plastics for composites. The increasing need for lighter-weight materials to construct aviation components and parts has been another significant factor contributing to the growth of the Asia Pacific plastics for composites market. Aircraft manufacturers are making efforts to enlarge primary thermoplastic structures in business jets and commercial aircraft. They have been the early adopters of long fiber-reinforced thermoplastics. Materials such as composites and polymers are significantly lighter than steel, brass, alloys, iron, etc. The use of these materials allows manufacturers to lower the weight of airplane parts, subsequently facilitating fuel cost reductions. These initiatives focus on creating lightweight materials and parts that will reduce fuel consumption and help adopt hybrid and electric planes in the future. This will help them strengthen the aerospace industry, along with achieving greener operations, as it adapts to more sustainable travel over the next few decades. Such initiatives are driving the demand for plastic-based composites.

Asia Pacific Plastics for Composites Market Overview

Asia Pacific is witnessing urbanization, along with the rising construction of residential and commercial projects. Moreover, the per capita income in the region has increased, coupled with the development of affordable residential buildings. This has resulted in rapid urbanization in Asia Pacific. The beneficial government policies related to residential property developments in several countries of the region propelled urbanization. Moreover, countries such as China and India are amongst the world’s top five countries with installed wind power. Asia Pacific is home to major semiconductor and automobile players across the world. Samsung Electronics Co., Ltd.; Sony Group Corporation; SK Hynix Inc.; Toyota Motor Corporation; Tata Motors Ltd.; Hyundai Motor Company; Nissan Motor Co., Ltd.; and Honda Motor Co., Ltd. are among the major players present in Asia Pacific. These companies are focused on expansion, research and development, and product innovation.

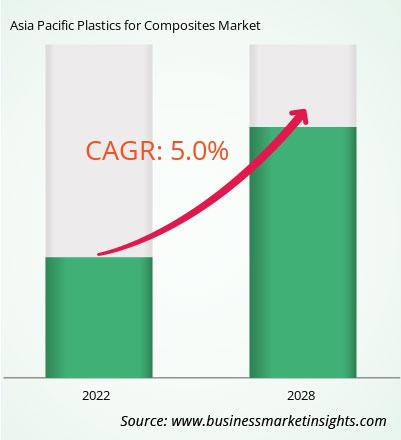

Asia Pacific Plastics for Composites

Market

Revenue and Forecast to 2028 (US$ Million)

Strategic insights for the Asia Pacific Plastics for Composites provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market. The geographic scope of the Asia Pacific Plastics for Composites refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas. Get more information on this report

Get more information on this report Asia Pacific Plastics for Composites Strategic Insights

Get more information on this report

Get more information on this report Asia Pacific Plastics for Composites Report Scope

Report Attribute

Details

Market size in 2022

US$ 10,120.73 Million

Market Size by 2028

US$ 13,525.08 Million

Global CAGR (2022 - 2028)

5.0%

Historical Data

2020-2021

Forecast period

2023-2028

Segments Covered

By Type

By Technology

Regions and Countries Covered

Asia-Pacific

Market leaders and key company profiles

Get more information on this report Asia Pacific Plastics for Composites Regional Insights

Get more information on this report

Get more information on this report

Asia Pacific Plastics for Composites

Market

Segmentation

The Asia Pacific plastics for composites market is segmented based on type, technology, and country. Based on type, the Asia Pacific plastics for composites market is bifurcated into thermoset and thermoplastic. The thermoset cylinders segment held a larger market share in 2022. Further, thermoset is segmented into polyester, vinyl ester, epoxy, polyurethane, and others. Further, thermoplastic is segmented into polypropylene, polyethylene, polyvinylchloride, polystyrene, polyethylene terephthalate, polycarbonate, and others.

Based on technology, the Asia Pacific plastics for composites market is segmented into injection molding, compression molding, pultrusion, resin infusion, and others. The others segment held the largest market share in 2022.

Based on country, the Asia Pacific plastics for composites market is segmented into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific plastics for composites market share in 2022.

Lanxess AG; Convestro AG; Celanese Corp; INEOS Group Holdings SA; Daicel Corp; Basf SE; Evonik Industries AG; Solvay SA; Saudi Basic Industries Corp; and Arkema SA are the leading companies operating in the Asia Pacific plastics for composites market.

The Asia Pacific Plastics for Composites Market is valued at US$ 10,120.73 Million in 2022, it is projected to reach US$ 13,525.08 Million by 2028.

As per our report Asia Pacific Plastics for Composites Market, the market size is valued at US$ 10,120.73 Million in 2022, projecting it to reach US$ 13,525.08 Million by 2028. This translates to a CAGR of approximately 5.0% during the forecast period.

The Asia Pacific Plastics for Composites Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Plastics for Composites Market report:

The Asia Pacific Plastics for Composites Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Plastics for Composites Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Plastics for Composites Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Plastics for Composites Market

Get Free Sample For Asia Pacific Plastics for Composites Market