Asia-Pacific Plastic to Fuel Market

Increasing Energy Requirement

Electricity is at the heart of modern economies, and it accounts for an increasing proportion of energy services. As a result of increased family incomes, electrification of transportation and heat, and a rise in demand for digital linked gadgets and air conditioning, the energy demand is expected to rise even more. Based on the current stated policies Scenario, the global electricity consumption will grow at a rate of 2.1% per year until 2040, more than double the rate of primary energy demand. As a result, electricity's share of total final energy consumption will increase from 19% in 2018 to 24% in 2040. In emerging nations, the increase in energy consumption is projected to be particularly large. Government policies, market conditions, and available technology all work together in the Stated Policies Scenario to shift energy supply toward low-carbon sources, with their share growing from 36% (current share) to 52% in 2040. Furthermore, the rising electricity demand was one of the main reasons why global CO2 emissions from the power sector reached a new high in 2018. However, the commercial availability of a diverse range of low-emission generation technologies places electricity at the forefront of efforts to combat climate change and pollution, which is increasing the demand for alternate solutions, thereby resulting in PTF market expansion.

Market Overview

Australia, China, India, Japan, South Korea, and rest of Asia Pacific are the key contributors to the plastic to fuel market in the Asia Pacific. China alone produces 59,079,741 tons of plastic every year. These plastic wastes are either dumped into landfills or the ocean, thereby populating the environment and leaving long-term adverse impacts worldwide. Moreover, Asia Pacific accounts for the major share in marine plastic pollution with major contributors such as China, Indonesia, Sri Lanka, Vietnam, and the Philippines. Inefficient waste management infrastructure and the lack of awareness regarding the adverse impact of single-use plastic are the main reasons contributing to the rise in plastic waste across the region. The rising investments by both the governments and private organizations to promote recycling of plastic to further reusable materials are propelling the growth of the Asia Pacific plastic to fuel market across the region. In 2020, Circulate Capital, an investment management organization, announced its investment of US$ 19 million in four privately held Indian recycling companies – Srichakra Polyplast, Dalmia Polypro Industries, Deeya Panel Products, and Rapidue Technologies. Similarly, in 2020, Circulate Capital Ocean Fund (CCOF) invested US$ 39 million to create the largest investment portfolio devoted to fighting ocean plastic waste across India. Hence, constant investments by government and private companies to fight the adverse impact of plastic across countries in Asia Pacific are expected to contribute to the growth of the market. Owing to the rise in investments in plastic waste recycling across the region, plastic to fuel market players is also investing in expanding their business across the region. Moreover, local companies are investing in the market. For instance, Singapore-based Environmental Solutions (Asia) Pte Ltd offers plastic to fuel services in the country. Similarly, with the help of pyrolysis technology, newoil converts millions of tons of plastic every year. In 2020, the company announced its plan to convert 20,000 tons of plastic waste into diesel fuel for transportation applications across Singapore.

Strategic insights for the Asia-Pacific Plastic to Fuel provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market. The geographic scope of the Asia-Pacific Plastic to Fuel refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas. Get more information on this report

Get more information on this report Asia-Pacific Plastic to Fuel Strategic Insights

Get more information on this report

Get more information on this report Asia-Pacific Plastic to Fuel Report Scope

Report Attribute

Details

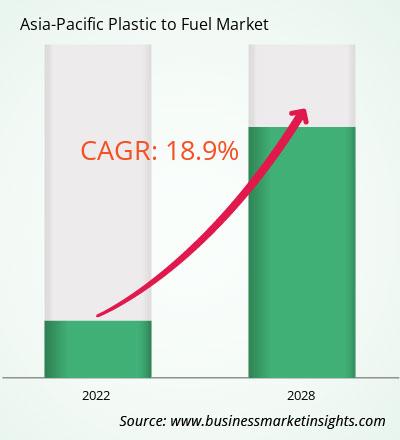

Market size in 2022

US$ 1,554.95 Million

Market Size by 2028

US$ 4,387.33 Million

Global CAGR (2022 - 2028)

18.9%

Historical Data

2020-2021

Forecast period

2023-2028

Segments Covered

By Technology

By End Product

Regions and Countries Covered

Asia-Pacific

Market leaders and key company profiles

Get more information on this report Asia-Pacific Plastic to Fuel Regional Insights

Get more information on this report

Get more information on this report

The Asia Pacific plastic to fuel market is segmented into technology, end product, and country.

Based on technology, the market is segmented into pyrolysis, gasification, and depolymerization. The pyrolysis segment registered the largest market share in 2022.

Based on end product, the market is segmented into crude oil, hydrogen, and others. The crude oil segment held a largest market share in 2022.

Based on country, the market is segmented into Australia, China, India, Japan, South Korea, and rest of APAC. China dominated the market share in 2022.

Agilyx; Klean Industries Inc; Plastic2Oil, Inc; Cassandra Oil AB; MK Aromatics Limited; and OMV Aktiengesellschaft are the leading companies operating in the Asia Pacific plastic to fuel market in the region.

The Asia-Pacific Plastic to Fuel Market is valued at US$ 1,554.95 Million in 2022, it is projected to reach US$ 4,387.33 Million by 2028.

As per our report Asia-Pacific Plastic to Fuel Market, the market size is valued at US$ 1,554.95 Million in 2022, projecting it to reach US$ 4,387.33 Million by 2028. This translates to a CAGR of approximately 18.9% during the forecast period.

The Asia-Pacific Plastic to Fuel Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia-Pacific Plastic to Fuel Market report:

The Asia-Pacific Plastic to Fuel Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia-Pacific Plastic to Fuel Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia-Pacific Plastic to Fuel Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia-Pacific Plastic to Fuel Market

Get Free Sample For Asia-Pacific Plastic to Fuel Market