Asia Pacific Mining Explosives Market

Rare earth metals, also known as rare earth elements (REEs), are elements found in the earth's crust. These elements are known for their unique properties and have various applications across different industries, including electronics, renewable energy, automotive, defense & aerospace, and medical equipment. The growing demand for rare earth metals from these sectors has surged the need to explore new deposits of rare earth metals. According to the United States Geological Survey, global rare earth reserves estimated at Vietnam’s rare earth mine production jumped to 4,300 metric tons in 2022 from 400 metric tons in 2021.

Additionally, in April 2023, National Geophysical Research Institute (NGRI) discovered large deposits of 15 rare earth elements (REE) in Anantapur district, Andhra Pradesh, India. Successful exploration results and identifying economically viable rare earth metal deposits can lead to expansion operations. Before commencing mining operations, extensive site preparation and infrastructure development are required. This includes clearing vegetation, leveling terrain, constructing access roads, and establishing mining facilities. Mining explosives are employed in these activities to clear land, shape terrain, and build access routes, facilitating the development of mining sites for rare earth metals.

Further, rare earth metals are often embedded within hard rock formations, making their extraction challenging. The exploration activities for rare earth metals involve extensive drilling and blasting to extract mineral samples and access the viability of deposits. Mining explosives are crucial in breaking down rocks and facilitating access to mineral-rich areas. As companies move from exploration to production, the demand for mining explosives escalates to support larger-scale mining activities. Thus, the growing exploration activities of rare earth metals would offer lucrative opportunities for the Asia Pacific mining explosives market during the forecast period.

Asia Pacific marks the presence of ten major surface mining projects, namely, Green Mine (China), Sangatta Mine (Indonesia), Heidaigou Mine (China), Oyu Tolgoi Copper-Gold Mine (Mongolia), Gevra OC Mine (India), Letpadaung Copper Mine (Myanmar), Li Mine (Thailand), FTB Project (Thailand), and Pasir Mine (Indonesia). Asia is also home to leading mining companies such as Mitsubishi Materials Corporation, Jiangxi Copper Co Ltd, Aluminum Corporation of China Ltd, Coal India Limited, China Molybdenum Co Ltd, and BHP. According to Coal 2021 report published by the International Energy Agency, in 2020, the total coal consumption in China was more than 50% of the global coal consumption. The growing need for coal in the country is attributed to the rising electricity demand and strong presence of chemicals & materials industry.

According to the report published by the US Geological Survey in 2022, China was the largest supplier of twenty-five non-fuel mineral commodities to several other countries in 2021. Out of twenty-five listed minerals, China produced sixteen critical minerals. Moreover, China, Tajikistan, Australia, and Vietnam accounted for major antimony mine production and reserves. Further, India, China, and Australia were the leading countries in global mine production and reserves for garnets. According to the World Mining Data 2022 report released by the Federal Ministry Republic of Austria, Australia witnessed a rise of 142.2% in the mining production rate for minerals from 2000 to 2020. Mining, quarrying, and perforating operations involve the utilization of explosives. The demand for mining explosives is directly proportional to the region's mining operations and mineral reserves. Therefore, the high number of potential metal and nonmetal reserves and a rise in mining operations across the region is expected to boost the demand for mining explosives during the forecast period.

The Asia Pacific mining explosives market is segmented based on type, application, and country.

Based on type, the Asia Pacific mining explosives market is categorized into trinitrotoluene (TNT), ANFO, RDX, pentaerythritol tetranitrate (PETN), others. The ANFO segment held the largest share in 2023.

By application, the Asia Pacific mining explosives market is segmented into quarrying and non-metal mining, metal mining, and coal mining. The coal mining segment held the largest share in 2023.

Based on country, the Asia Pacific mining explosives market is segmented into Australia, China, India, Indonesia, Vietnam, and the Rest of Asia Pacific. China dominated the Asia Pacific mining explosives market in 2023.

Orica Ltd, Dyno Nobel, China Poly Group Corp Ltd, Hanwha Corp, Sasol Ltd, NOF Corp, Koryo Nobel Explosives Co Ltd, Solar Industries India Ltd, and Omnia Holding Ltd are some of the leading companies operating in the Asia Pacific mining explosives market.

Strategic insights for the Asia Pacific Mining Explosives provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 14,226.78 Million |

| Market Size by 2030 | US$ 19,342.89 Million |

| Global CAGR (2023 - 2030) | 4.5% |

| Historical Data | 2021-2022 |

| Forecast period | 2024-2030 |

| Segments Covered |

By Type

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Mining Explosives refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

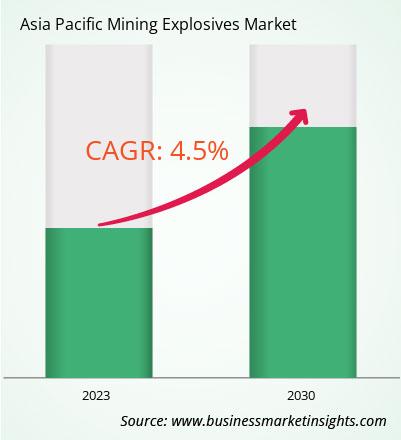

The Asia Pacific Mining Explosives Market is valued at US$ 14,226.78 Million in 2023, it is projected to reach US$ 19,342.89 Million by 2030.

As per our report Asia Pacific Mining Explosives Market, the market size is valued at US$ 14,226.78 Million in 2023, projecting it to reach US$ 19,342.89 Million by 2030. This translates to a CAGR of approximately 4.5% during the forecast period.

The Asia Pacific Mining Explosives Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Mining Explosives Market report:

The Asia Pacific Mining Explosives Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Mining Explosives Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Mining Explosives Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Mining Explosives Market

Get Free Sample For Asia Pacific Mining Explosives Market