Asia Pacific In-Vitro Diagnostics Market

IVD is used in clinical, laboratory, and outpatient settings with the aim specifically to help in the detection of diseases and, consequently, aid in the selection of appropriate treatment protocols. The integration of IVD technologies with digital health solutions is gaining traction globally. Data analytics, artificial Intelligence, and remote monitoring enhance the value of diagnostic tests, leading to better patient management and outcomes. IVD technologies integrated with digital health solutions can be incorporated into clinical decision support systems. As recognized by the WHO, digital health solutions could help detect diseases. Artificial intelligence health bots and similar other emerging solutions may present opportunities for patient care and address challenges such as high cost and time requirements. In diagnostics based on genomic testing, deep learning can identify cancer cells, determine their type, and predict what mutations may occur in a tumor from images of a specific sample. Artificial intelligence and machine learning (AI/ML) in in-vitro diagnostics are revolutionizing medical device development. These modern diagnostic systems facilitate diagnosis based on digital image analysis, thereby improving healthcare decision-making. Smart diagnostics are extremely scalable IVD solutions that use artificial intelligence to perform better than lab-based diagnostics at a fraction of the price. Additionally, this type of diagnostics can derive emergent features through unique chemical and biological signature detection and analysis. Thus, the integration of IVD with digital health technologies is likely to offer lucrative opportunities to the in-vitro diagnostics market in the coming years.

The Asia Pacific in-vitro diagnostics market has been segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. The market growth in China is high attributed to the rising awareness of the disease diagnosis. India holds third largest share in terms of in-vitro diagnostics owing to high prevalence of diseases across the country. The aforementioned factors are responsible for influential growth of in-vitro diagnostics market in the Asia Pacific region. There has been a growth in cancer incidence and mortality rates in China, which has made cancer the primary cause of death in the last decade in the country. The majority of the increasing cases are due to population growth (particularly an upsurge in the elderly population) and socio-demographic changes. Q2 Solutions, a clinical trial laboratory services organization, collaborated with Guangzhou KingMed Diagnostics to develop in-vitro diagnostics products and companion diagnostics (CDx) for the Chinese market. Moreover, several players are investing in the expansion of the cancer biomarkers market. In August 2018, Ipsos’ Healthcare Service Line launched the syndicated lab mapping study and oncology molecular diagnostics (MDx) monitor. These two studies will offer comprehensive oncology biomarker testing in China’s tier I and tier II cities.

The Asia Pacific in-vitro diagnostics market is segmented into product & services, technology, application, end user, and country.

Based on product & services, the Asia Pacific in-vitro diagnostics market is segmented into reagents & kits, instruments, and software & services. The reagents & kits segment held the largest share of the Asia Pacific in-vitro diagnostics market in 2022.

Based on technology, the Asia Pacific in-vitro diagnostics market is segmented into immunoassay/ immunochemistry, clinical chemistry, molecular diagnostics, microbiology, blood glucose self-monitoring, coagulation & hemostasis, hematology, urinalysis, and others. The immunoassay/ immunochemistry segment held the largest share of the Asia Pacific in-vitro diagnostics market in 2022.

Based on application, the Asia Pacific in-vitro diagnostics market is segmented into infectious diseases, diabetes, oncology, cardiology, autoimmune diseases, nephrology, and others. The infectious diseases segment held the largest share of the Asia Pacific in-vitro diagnostics market in 2022.

Based on end user, the Asia Pacific in-vitro diagnostics market is segmented into hospitals, laboratories, homecare, and others. The hospitals segment held the largest share of the Asia Pacific in-vitro diagnostics market in 2022.

Based on country, the Asia Pacific in-vitro diagnostics market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific in-vitro diagnostics market in 2022.

Abbott Laboratories, Becton Dickinson and Co, bioMerieux SA, Bio-Rad Laboratories Inc, Danaher Corp, F. Hoffmann-La Roche Ltd, Qiagen NV, Siemens AG, and Thermo Fisher Scientific Inc are some of the leading companies operating in the Asia Pacific in-vitro diagnostics market.

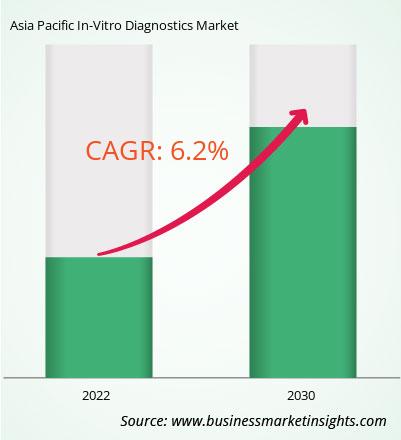

The Asia Pacific In-Vitro Diagnostics Market is valued at US$ 19,109.18 Million in 2022, it is projected to reach US$ 30,943.27 Million by 2030.

As per our report Asia Pacific In-Vitro Diagnostics Market, the market size is valued at US$ 19,109.18 Million in 2022, projecting it to reach US$ 30,943.27 Million by 2030. This translates to a CAGR of approximately 6.2% during the forecast period.

The Asia Pacific In-Vitro Diagnostics Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific In-Vitro Diagnostics Market report:

The Asia Pacific In-Vitro Diagnostics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific In-Vitro Diagnostics Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific In-Vitro Diagnostics Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific In-Vitro Diagnostics Market

Get Free Sample For Asia Pacific In-Vitro Diagnostics Market