Asia Pacific Healthcare CRM Market

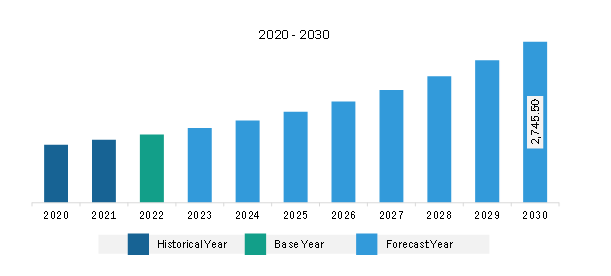

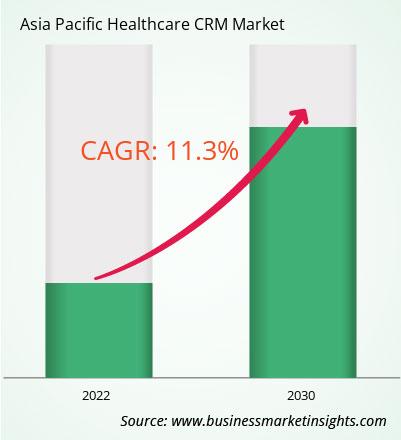

The Asia Pacific healthcare CRM market was valued at US$ 1,166.17 million in 2022 and is expected to reach US$ 2,745.50 million by 2030; it is estimated to register a CAGR of 11.3% from 2022 to 2030.

The demand for data-driven insights, analytics, and population health management is significantly promoting the development of the healthcare industry, which, in turn, propels the demand for healthcare CRM. This increase in demand can be related to the growing emphasis on value-based care and the demand for healthcare organizations to improve patient outcomes, lower costs, and improve overall care quality. Data-driven insights analytics are critical in healthcare CRM since they allow organizations to examine and evaluate large volumes of patient data to identify trends, patterns, and correlations. This enables healthcare practitioners to understand their patient population better, allowing them to make more accurate decisions about treatment plans, interventions, and resource allocation. Healthcare organizations may also identify high-risk patients, forecast prospective illnesses, and intervene proactively to prevent negative outcomes by employing data-driven analytics. Similarly, population health management is another significant driver of the growing demand for data-driven insights and analytics in the Asia Pacific healthcare CRM market. Population health management, focusing on improving the health outcomes of entire populations, necessitates healthcare organizations having an extensive understanding of their patient population and the factors that impact their health. Data-driven insights analytics allow healthcare professionals to segment their patient population based on criteria including demographics, clinical problems, and risk factors. This allows them to personalize medical services and treatment plans to the individual requirements of distinct patient groups.

Furthermore, healthcare CRM developers rapidly integrate advanced analytics and population health management capabilities into healthcare CRM platforms. These capabilities enable healthcare organizations to use data to enhance clinical and operational outcomes, resulting in better patient care and lower costs. Thus, the increasing demand for data-driven insights, analytics, and population health management propels the demand for healthcare CRM to improve patient outcomes, reduce costs, and enhance the overall quality of care, which fuels the growth of the Asia Pacific healthcare CRM market.

The market for healthcare CRM in China is expected to witness significant growth in the coming years due to the increasing adoption of digital technologies in the healthcare sector. The Chinese government is promoting digital health solutions to improve the quality and accessibility of healthcare services. Under the Healthy China 2030 plan, China plans to invest significantly in advancing its healthcare technology innovation in the coming years. This expenditure is intended to ensure health equity within China through technological advancements and improvements to the healthcare system.

Additionally, China is among the most densely populated countries across the world. The current population is ~1.41 billion. According to the Global Burden of Disease (GBD) study published in October 2020, the population in the country is prone to infectious, chronic, and acute diseases. China reports the incidence of many diseases such as stroke, cancer, Alzheimer's, and diabetes. The rising number of patients and the increasing demand for better healthcare services boost the Asia Pacific healthcare CRM market growth in China. Furthermore, according to data from the Future Health Index, 94% of Chinese healthcare professionals used digital health technology or mobile health apps. The growing presence of local key players is boosting the China healthcare CRM market growth. Manufacturers are focusing on expanding their strategic global presence and specialized expertise with exclusive technological capabilities, leading to the market growth in China. Aging population has become one of the major contributors to the increased demand for healthcare CRM software as they are unable to visit the hospital anytime due to physical stress and thus require a proper schedule for medical visits and a digital appointment for home care settings. In 2019, 12.6% of China's population was over 65. Also, as per WHO, by 2040, ~402 million people (i.e., 28% of the total population) will be over 60. Thus, China is facing pressures of an aging population and constant rise in the prevalence of diseases such as cancer, Alzheimer's disease, and diabetes. As a result, demand for hospital visits and online appointments will continue to rise, setting new requirements for healthcare CRM software in China.

Strategic insights for the Asia Pacific Healthcare CRM provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 1,166.17 Million |

| Market Size by 2030 | US$ 2,745.50 Million |

| Global CAGR (2022 - 2030) | 11.3% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Deployment Mode

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Healthcare CRM refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Asia Pacific healthcare CRM market is categorized into deployment mode, product type, application, and end user, and country.

Based on deployment mode, the Asia Pacific healthcare CRM market is bifurcated cloud based and on-premise. The cloud based segment held a larger market share in 2022.

In terms of product type, the Asia Pacific healthcare CRM market is categorized into operational CRM, analytical CRM, and collaborative CRM. The operational CRM segment held a larger market share in 2022.

By application, the Asia Pacific healthcare CRM market is segmented into relationship management, case management, case coordination, community outreach, and others. The relationship management segment held the largest market share in 2022. The case management segment is further subsegmented into disease management and clinical trials relationship management. The case coordination segment is further subsegmented into patient information management and pre-authorizations / eligibility. The community outreach segment is further services outreach/promotion and community health education.

By end user, the Asia Pacific healthcare CRM market is segmented into providers, payers, and others. The providers segment held the largest market share in 2022.

By country, the Asia Pacific healthcare CRM market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific healthcare CRM market share in 2022.

International Business Machines Corp, IQVIA Holdings Inc, Microsoft Corp, Oracle Corp, Pegasystems Inc, Sage Group Plc, Salesforce Inc, SAP SE, SugarCRM Inc, Veeva Systems Inc, and Zendesk Inc are among the leading companies operating in the Asia Pacific healthcare CRM market.

1. International Business Machines Corp

2. IQVIA Holdings Inc

3. Microsoft Corp

4. Oracle Corp

5. Pegasystems Inc

6. Sage Group Plc

7. Salesforce Inc

8. SAP SE

9. SugarCRM Inc

10. Veeva Systems Inc

11. Zendesk Inc

The Asia Pacific Healthcare CRM Market is valued at US$ 1,166.17 Million in 2022, it is projected to reach US$ 2,745.50 Million by 2030.

As per our report Asia Pacific Healthcare CRM Market, the market size is valued at US$ 1,166.17 Million in 2022, projecting it to reach US$ 2,745.50 Million by 2030. This translates to a CAGR of approximately 11.3% during the forecast period.

The Asia Pacific Healthcare CRM Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Healthcare CRM Market report:

The Asia Pacific Healthcare CRM Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Healthcare CRM Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Healthcare CRM Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Healthcare CRM Market

Get Free Sample For Asia Pacific Healthcare CRM Market