Asia Pacific Fiberglass Pipes Market

Metal, concrete, steel, plastics, and composites are used to produce pipes for several applications ranging from oil & gas transmission and wastewater treatment to chemical pipelines. Material type and size are major factors considered by the end-use industries while selecting pipe for specific applications. Due to their characteristics such as corrosion resistance, nontoxic nature, strong impact resistance, weathering resistance, hydraulic efficiency, long service life, lightweight, and low thermal & electrical conductivity, fiberglass pipes are preferred over conventional concrete, metal, or plastic pipes.

Fiberglass pipe manufacturers and suppliers offer a wide range of products for several corrosive and hazardous applications. Enduro Composites provide fiberglass pipes that meet plant specifications and industry standards. The portfolio comprises fiberglass pipes with properties such as less downtime, high strength, durability, resistance to 1,000 chemicals, and temperature tolerance from –40°F through 300°F. Steel and concrete pipes are susceptible to corrosion and negatively affect the structural integrity of pipes. Burgess Well Company Inc, provides nonconductive, torque resistant, and high-pressure resistant fiberglass pipes. The wide range of fiberglass pipes offered by manufacturers and the rising preference for composite pipes is expected to replace conventional pipes in several applications such as crude oil transmission, and chemicals and water sectors.

The fiberglass pipes market in Asia Pacific is segmented into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. This region is a prominent market for fiberglass pipes owing to growth in the chemical and oil & gas sectors and a rise in urbanization, leading to increased demand for sewage systems. Moreover, government initiatives and policies such as Make-in-India encourage the setup of various manufacturing plants in India. The rise in foreign direct investments also leads to regional economic growth, further bolstering industrialization in the region. The chemical manufacturing industry is an important part of manufactured exports for several Asian nations, including China, South Korea, India, and Japan. According to the International Council of Chemical Associations (ICCA), the Asia Pacific chemical industry is the largest contributor to the region’s GDP and employment, generating 45% of the industry's total annual economic value and 69% of all jobs supported.

Further, the demand for oil and gas is increasing in Asia Pacific. According to the International Energy Agency, the global oil demand rebounded in 2021, and Asia is expected to account for 77% of oil demand by 2025. Asian oil import requirements are expected to surpass 31 million barrels per day by 2025. All major Asian economies heavily depend on oil imports from the Middle East & Africa. Various countries in the region have initiated projects to cater to the growing demand for oil and gas. For instance, in April 2023, Asia's largest underwater hydro-carbon pipeline, below the river Brahmaputra connecting Jorhat and Majuli in Assam, India, was completed by the Indradhanush Gas Grid Limited (IGGL). Thus, the growing investments in such projects are expected to bolster the fiberglass pipes market during the forecast period.

The Asia Pacific fiberglass pipes market is segmented into resin type, end use, and country.

Based on resin type, the Asia Pacific fiberglass pipes market is segmented into polyester, epoxy, phenolic, and others. The polyester segment held a largest Asia Pacific fiberglass pipes market share in 2022.

Based on end use, the Asia Pacific fiberglass pipes market is segmented into oil and gas, sewage, chemicals, agriculture, and others. The oil and gas segment held the largest Asia Pacific fiberglass pipes market share in 2022.

Based on country, the Asia Pacific fiberglass pipes market has been categorized into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific fiberglass pipes market in 2022.

Amiblu Holding GmbH, Chemical Process Piping Pvt Ltd, EPP Composites Pvt Ltd, Fibrex FRP Piping Systems, Future Pipe Industries LLC, Gruppo Sarplast Srl, Lianyungang Zhongfu Lianzhong Composites Group Co Ltd, NOV Inc, Plasticon Germany GmbH, Poly Plast Chemi Plants (I) Pvt Ltd, Saudi Arabian Amiantit Co, and Sunrise Industries (India) Ltd are some of the leading companies operating in the Asia Pacific fiberglass pipes market.

Strategic insights for the Asia Pacific Fiberglass Pipes provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 1,457.17 Million |

| Market Size by 2028 | US$ 2,006.83 Million |

| Global CAGR (2022 - 2028) | 5.5% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Resin Type

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Fiberglass Pipes refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

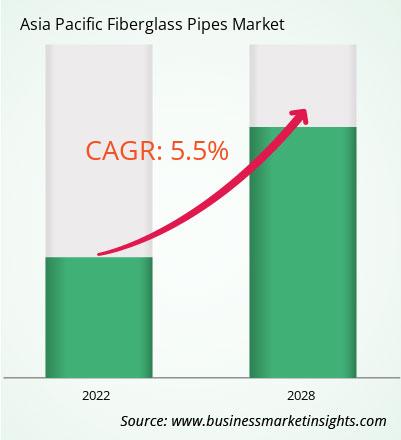

The Asia Pacific Fiberglass Pipes Market is valued at US$ 1,457.17 Million in 2022, it is projected to reach US$ 2,006.83 Million by 2028.

As per our report Asia Pacific Fiberglass Pipes Market, the market size is valued at US$ 1,457.17 Million in 2022, projecting it to reach US$ 2,006.83 Million by 2028. This translates to a CAGR of approximately 5.5% during the forecast period.

The Asia Pacific Fiberglass Pipes Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Fiberglass Pipes Market report:

The Asia Pacific Fiberglass Pipes Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Fiberglass Pipes Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Fiberglass Pipes Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Fiberglass Pipes Market

Get Free Sample For Asia Pacific Fiberglass Pipes Market