Asia Pacific Electronic Toll Collection System Market

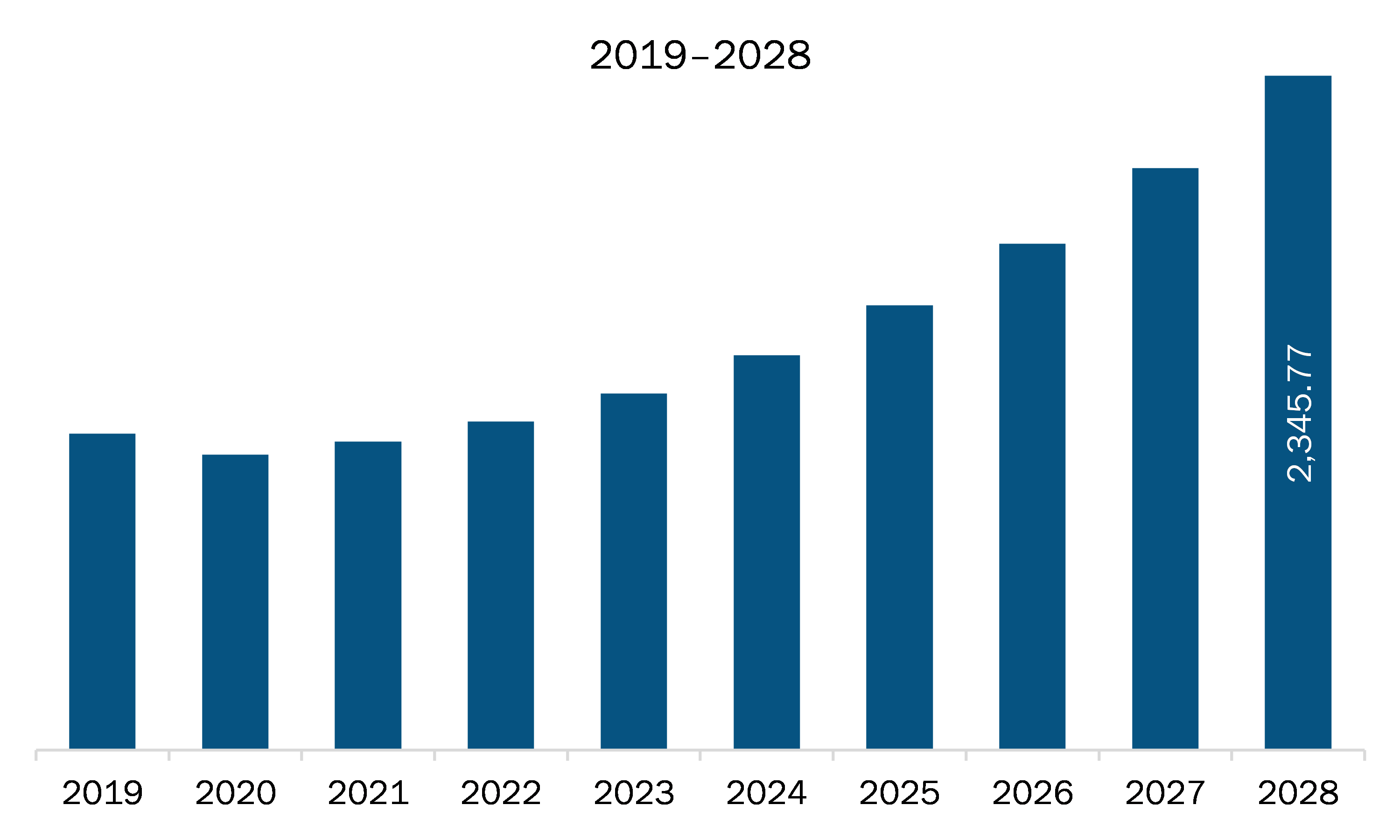

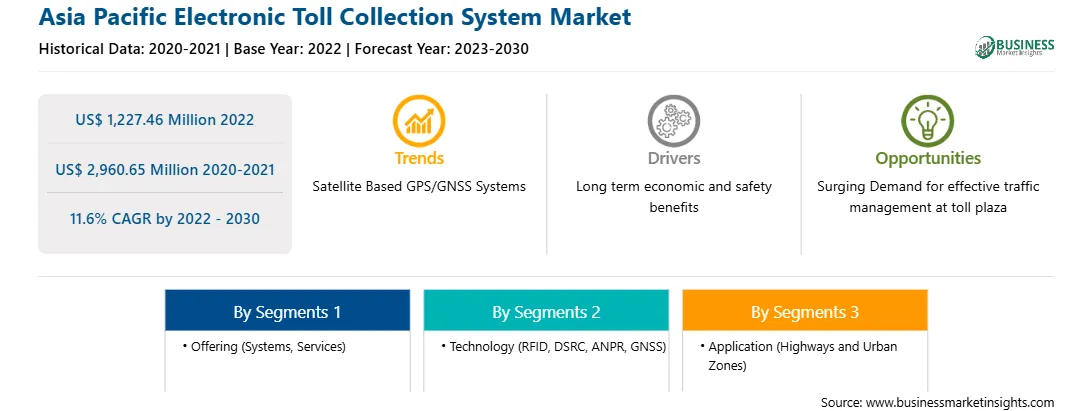

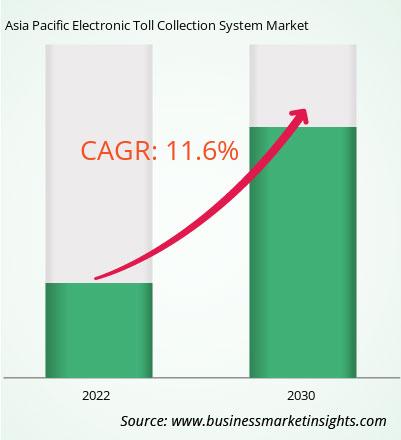

The Asia Pacific electronic toll collection system market was valued at US$ 1,227.46 million in 2022 and is expected to reach US$ 2,960.65 million by 2030; it is estimated to grow at a CAGR of 11.6% from 2022 to 2030.

The state of road infrastructure plays an essential role in the economy's growth as it connects important small cities, towns, and metropolitan cities for freight transportation by road. Moreover, the continuous maintenance, expansion, and improvement of expressways, highways, bridges, and tunnels ensure the continuous, uninterrupted movement of goods, which contribute toward the respective country's GDP. However, the administrators face the challenge of maintaining road infrastructure growth along with the number of registered vehicles. As a result, the central or state government agency deploys various tolls for fees and levy tax across strategic locations on roadways for financing new infrastructure, controlling traffic, maintenance, and management of congestion of vehicles.

Rapid urbanization has driven the demand for a robust network of roads connecting cities and towns across the countries globally. Subsequently, this has boosted the investment toward the development of highways, bridges, and expressways for improved freight transportation by road. As a result, this is increasing the demand for efficient toll collection systems in the region's economies owing to the surge in the number of registered vehicles.

Globally, many companies and government authorities have signed contracts for deploying ETC. A mentioned below is one of them:

In January 2022, the National Highways Authority of India (NHAI) tested the Advanced Traffic Management System (ATMS). This new system is expected to be soon installed on all the national highways and expressways across the country.

In 2021, two 30-year contracts for toll operation on India's National Highway NH-44 were awarded to Egis.

Therefore, numerous contracts contributing to the demand for effective traffic management at toll plazas are anticipated to create lucrative business opportunities for ETC manufacturers and providers in the coming years.

According to the Ministry of Transport, China had more than 181 million electronic toll collection (ETC) operators in December 2019. The country has experienced 100.34 million new ETC users since May 15, 2022. The Ministry of China issued a circular to universalize freeway ETC devices, aiming to install these devices on over 80% of registered vehicles by year-end. The policy is aimed at relieving freeway traffic congestion and reducing emissions and logistics costs. Furthermore, the government of China is constructing new roads. For instance, in July 2022, China announced its plans to construct a highway network of 461,000 kilometers by 2035 and further increase it to become world-class by 2050. Also, with rural revitalization high on the government's agenda, the country stepped up investment in rural infrastructure. Some 60,000 km of rural roads were constructed in the first half of 2022, up 17.7% and 9.2% year-on-year, respectively. Therefore, with such factors, the deployment of electronic toll collection systems is increasing in China, thereby boosting market growth.

Strategic insights for the Asia Pacific Electronic Toll Collection System provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 1,227.46 Million |

| Market Size by 2030 | US$ 2,960.65 Million |

| Global CAGR (2022 - 2030) | 11.6% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Offering

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Electronic Toll Collection System refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Asia Pacific electronic toll collection system market is segmented based on offering, technology, application, and country. Based on offering, the Asia Pacific electronic toll collection system market is bifurcated into systems and services. The systems segment held a larger market share in 2022.

In terms of technology, the Asia Pacific electronic toll collection system market is segmented into RFID, DSRC, ANPR, GNSS, and others. The RFID segment held the largest market share in 2022.

By application, the Asia Pacific electronic toll collection system market is bifurcated into highways and urban zones. The highways segment held a larger market share in 2022.

Based on country, the Asia Pacific electronic toll collection system market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific electronic toll collection system market share in 2022.

Conduent Inc, Kapsch TrafficCom AG, Thales SA, Toshiba Infrastructure Systems and Solutions Corp, Magnetic Autocontrol GmbH, P Square Solutions LLC, Sociedad Iberica de Construcciones Electricas SA, Verra Mobility Corp, Mitsubishi Heavy Industries Ltd., Mitsubishi Heavy Industries Machinery Systems Ltd, Cubic Transportation Systems Inc, and Q-Free ASA are some of the leading companies operating in the Asia Pacific electronic toll collection system market.

1. Conduent Inc

2. Kapsch TrafficCom AG

3. Thales SA

4. Toshiba Infrastructure Systems and Solutions Corp

5. Magnetic Autocontrol GmbH

6. P Square Solutions LLC

7. Sociedad Iberica de Construcciones Electricas SA

8. Verra Mobility Corp

9. Mitsubishi Heavy Industries Ltd.

10. Cubic Transportation Systems, Inc

11. Mitsubishi Heavy Industries Machinery Systems Ltd

12. Q-Free ASA.

The Asia Pacific Electronic Toll Collection System Market is valued at US$ 1,227.46 Million in 2022, it is projected to reach US$ 2,960.65 Million by 2030.

As per our report Asia Pacific Electronic Toll Collection System Market, the market size is valued at US$ 1,227.46 Million in 2022, projecting it to reach US$ 2,960.65 Million by 2030. This translates to a CAGR of approximately 11.6% during the forecast period.

The Asia Pacific Electronic Toll Collection System Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Electronic Toll Collection System Market report:

The Asia Pacific Electronic Toll Collection System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Electronic Toll Collection System Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Electronic Toll Collection System Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Electronic Toll Collection System Market

Get Free Sample For Asia Pacific Electronic Toll Collection System Market