Asia Pacific Data Center Construction Market

No. of Pages: 88 | Report Code: TIPRE00005734 | Category: Technology, Media and Telecommunications

No. of Pages: 88 | Report Code: TIPRE00005734 | Category: Technology, Media and Telecommunications

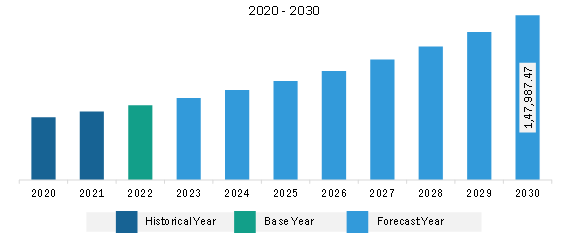

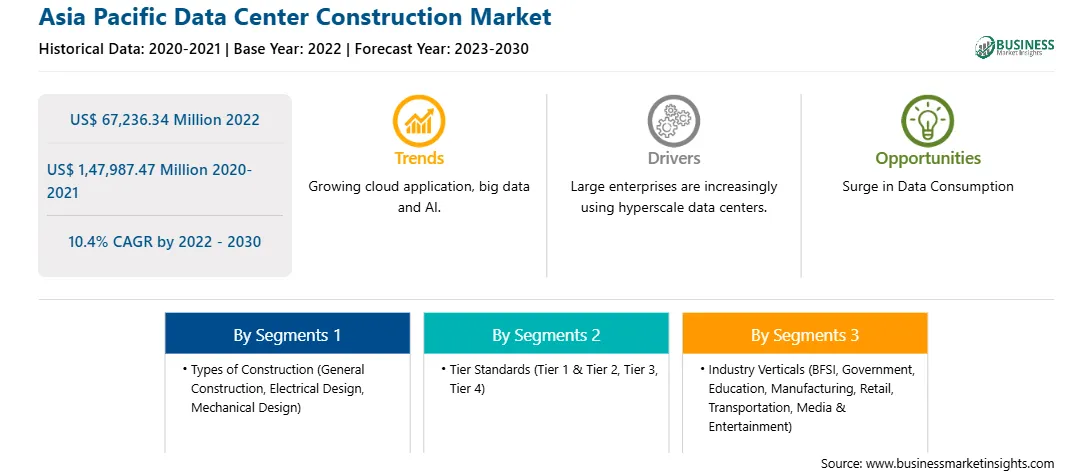

The Asia Pacific data center construction market was valued at US$ 67,236.34 million in 2022 and is expected to reach US$ 1,47,987.47 million by 2030; it is estimated to register at a CAGR of 10.4% from 2022 to 2030.

A hyperscale is a kind of large-scale data center that offers vast computing capabilities, often in the form of an elastic cloud platform. Organizations use them to manage and deliver extensive applications and services. The objective of hyperscalers is to expand their service offerings while maintaining better latency as well as improve availability in order to cover more ground. They face intense competition from colocation providers in addition to internal competitors. 37% of the capacity of data centers is owned by colocation providers such as Digital Realty, Equinix, CyrusOne, Chindata, and Global Switch; 32% by cloud service providers and hyperscalers; 20% by privately owned data centers; and 11% by telecoms.

Moreover, for small enterprises, constructing their data center involves huge capital. Since these enterprises have a limited budget or capital expenditure to construct a data center, the ROI is comparatively low. As a result, most of these enterprises are choosing colocation or cloud services. These companies do not require much storage space, and constructing their own data center is not feasible. Therefore, they depend on colocation or CSPs to store their data. Also, apart from the capital required to build a data center, other expenses and efforts such as maintenance and service become a burden for these companies. Moreover, the demand for colocation services and hyperscalers is leading to the rise in the construction of mega data centers as they offer economies of scale. Thus, the increasing implementation of hyperscalers and colocation is anticipated to create lucrative opportunities for the Asia Pacific data center construction market growth during the forecast period.

APAC comprises the majority of developing economies with the largest number of internet users. This factor presents significant opportunities for leading social media players and internet-based service providers to profit from the untapped APAC market. With the proliferation of cheap smartphones and tablets and increasing penetration of computing devices in businesses and households, the region accounts for the largest growing user base seeking internet-based services. Thus, the strong growth of internet-connected users coupled with good economic growth in the region are the factors encouraging the enterprise and cloud service providers to establish servers in proximity to the users, enabling them to access data with reduced latency and reaction time. This factor contributes to the growth of the Asia Pacific data center construction market in the region.

Strategic insights for the Asia Pacific Data Center Construction provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 67,236.34 Million |

| Market Size by 2030 | US$ 1,47,987.47 Million |

| Global CAGR (2022 - 2030) | 10.4% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Types of Construction

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Data Center Construction refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Asia Pacific data center construction market is segmented based on types of construction, tier standards, industry verticals, and country.

Based on types of construction, the Asia Pacific data center construction market is segmented into general construction, electrical design, and mechanical design. The electrical design segment held the largest share in 2022.

In terms of tier standards, the Asia Pacific data center construction market is segmented into tier 1 & tier 2, tier 3, and tier 4. The tier 3 segment held the largest share in 2022.

By industry verticals, the Asia Pacific data center construction market is segmented into IT & telecommunication, BFSI, government, education, manufacturing, retail, transportation, media & entertainment, and others. The IT & telecommunication segment held the largest share in 2022.

Based on country, the Asia Pacific data center construction market is categorized into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific data center construction market in 2022.

Rittal GmbH & Co KG, Schneider Electric SE, DPR Construction Inc, AECOM, Turner Construction Co, Eaton Corp Plc, and Nikom InfraSolutions Pvt. Ltd are some of the leading companies operating in the Asia Pacific data center construction market.

The Asia Pacific Data Center Construction Market is valued at US$ 67,236.34 Million in 2022, it is projected to reach US$ 1,47,987.47 Million by 2030.

As per our report Asia Pacific Data Center Construction Market, the market size is valued at US$ 67,236.34 Million in 2022, projecting it to reach US$ 1,47,987.47 Million by 2030. This translates to a CAGR of approximately 10.4% during the forecast period.

The Asia Pacific Data Center Construction Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Data Center Construction Market report:

The Asia Pacific Data Center Construction Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Data Center Construction Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Data Center Construction Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Data Center Construction Market

Get Free Sample For Asia Pacific Data Center Construction Market