Asia Pacific Carbon Fiber-Based SMC BMC Market

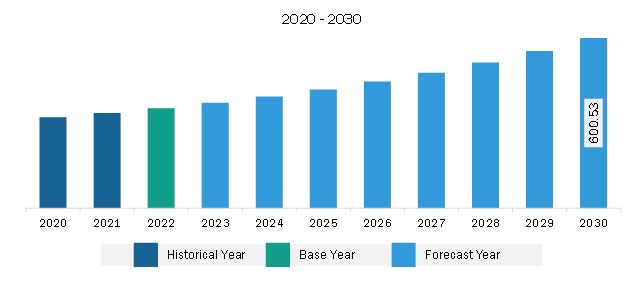

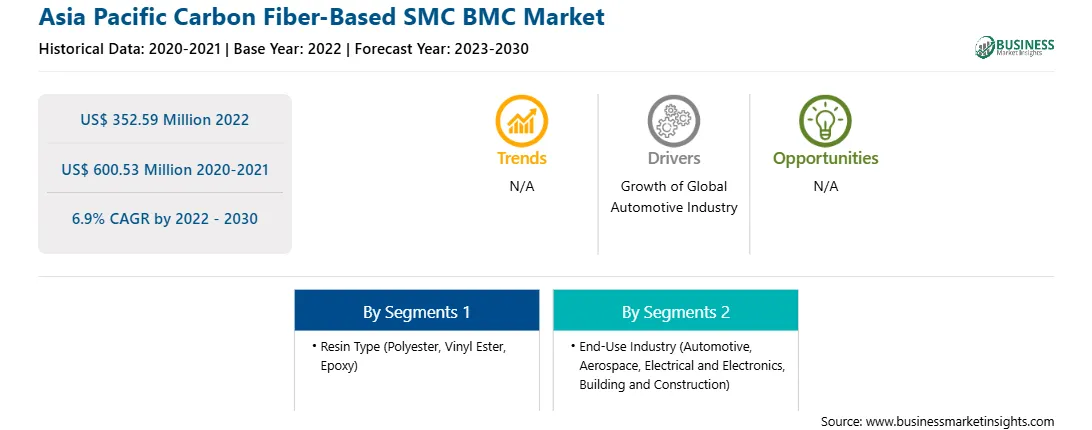

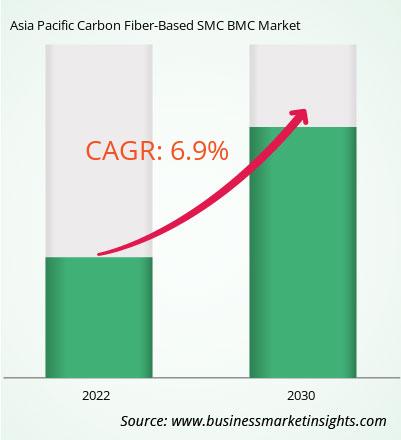

The Asia Pacific carbon fiber-based SMC BMC market was valued at US$ 352.59 million in 2022 and is expected to reach US$ 600.53 million by 2030; it is estimated to grow at a CAGR of 6.9% from 2022 to 2030.

According to a report published by the European Automobile Manufacturers' Association (ACEA), global motor vehicle production rose by 1.3% from 2020 to 2021, and 79.1 million motor vehicles, including 61.6 million passenger cars, were produced worldwide in 2021. According to a report by the Bureau of Transportation Statistics, China is one of the dominant markets for producing passenger cars and commercial vehicles. According to the China Passenger Car Association, ~2.17 million passenger cars were sold through retail channels in December 2022, an increase of 3% year-on-year. In the country, from January to December 2022, 20.54 million passenger cars were sold, a rise of 1.9% year-on-year. The China Passenger Car Association states that a car-purchase tax cut policy has massively contributed to vehicle sales since its launch in June 2022. The policy reduced the purchase tax by 50% for passenger cars that cost under 300,000 yuan (~US$ 43,103), have engine displacement below 2 liters, and are purchased between June 1 and December 31, 2022. Elsewhere, India has a strong automotive industry in terms of domestic demand and exports. The automotive industry in India is growing due to the rising income of middle-class people, increasing investments, and policy support from the government of India. In the country, the automobile sector received a cumulative equity FDI inflow of about US$ 34.11 billion between April 2000 and December 2022. Several automakers have started investing heavily in various segments of the industry in India to keep up with the growing demand. In February 2023, Nissan and Renault announced their plan to invest US$ 600 million in India over the next 3-5 years to expand their share in the passenger cars & electric vehicles market. All these factors are driving the growth of the automotive industry in India. As per the International Organization of Motor Vehicle Manufacturers report, in 2021, the countries in Asia Pacific produced ~46.73 million units of motor vehicles. According to the International Organization of Motor Vehicle Manufacturers, motor vehicle production in Japan reached 7.83 million units in 2022. Carbon fiber-based SMC and BMC are lightweight and offer durability, design flexibility, tolerance to temperature fluctuations, and chemical resistance. They have various applications such as automotive body panels, structural components, and insulating components. The demand for SMC and BMC for the production of automobiles has increased due to a high emphasis on reducing vehicle weight and enhancing fuel efficiency. The rise in electric and hybrid vehicles has further boosted the demand for lightweight materials for the insulation of electrical components. Thus, the growing automotive industry propels the demand for automotive components, subsequently boosting the carbon fiber-based SMC BMC market during the forecast period.

The Asia Pacific carbon fiber-based SMC and BMC market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. The market growth in Asia Pacific is driven by the strong presence of the automotive, building & construction, electronics, wind energy, and other industries. Asia Pacific is a hub for automotive manufacturing with a large presence of international and domestic players operating in the region. According to a report published by the China Passenger Car Association, Tesla Inc delivered 83,135 made-in-China electric vehicles in 2022, indicating growth in sales of electric vehicles compared to 2021. The International Organization of Motor Vehicle Manufacturers report states that various countries in Asia Pacific produced ~46.73 million units of motor vehicles in 2021. In the production of cars, trucks, buses, and agricultural vehicles, SMC and BMC products offer advantages such as parts consolidation, corrosion resistance, low weight, and others. Benefits of SMC and BMC products, coupled with the growing automotive industry, propel the market growth in Asia Pacific. The strong growth of the building & construction industry in Asia Pacific due to the growing population, rising residential construction activities, and increasing investments in commercial and industrial construction fuels the carbon fiber-based SMC and BMC market growth in the region. Further, China, Japan, and South Korea are among the major nations in the shipbuilding sector. According to The States Council of The People's Republic of China, the shipbuilding output of China was 9.61 million deadweight tons (dwt) in 2022, accounting for 46.2% of the world's total, up 2.8% year-on-year. SMC and BMC products find application in shipbuilding. Marine fiber-reinforced plastic has great potential for reducing structural weight due to its lightweight and high strength. Thus, the growing shipbuilding activities in the region fuel the carbon fiber-based SMC and BMC market growth in Asia Pacific. Furthermore, Asia Pacific experiences demand for sustainable energy resources, which has propelled the growth of wind energy projects in the region. According to the report by International Energy Agency, in 2021, China registered 70% of the world's wind generation growth. Moreover, as per the 14th Five-Year Plan published by China in June 2022, the country is expected to account for a target of 33% of electricity generation from renewables by 2025, including an 18% target for solar and wind technologies. Hence, the growing wind energy sector increases the demand for carbon fiber-based SMC and BMC products in Asia Pacific.

Strategic insights for the Asia Pacific Carbon Fiber-Based SMC BMC provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 352.59 Million |

| Market Size by 2030 | US$ 600.53 Million |

| Global CAGR (2022 - 2030) | 6.9% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Resin Type

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Carbon Fiber-Based SMC BMC refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Asia Pacific carbon fiber-based SMC BMC market is segmented based on resin type, end-use industry, and country.

Based on resin type, the Asia Pacific carbon fiber-based SMC BMC market is segmented into polyester, vinyl ester, epoxy, and others. The polyester segment held the largest share in 2022.

By end-use industry, the Asia Pacific carbon fiber-based SMC BMC market is categorized into automotive, aerospace, electrical and electronics, building and construction, and others. The automotive segment held the largest share in 2022.

Based on country, the Asia Pacific carbon fiber-based SMC BMC market is segmented into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific carbon fiber-based SMC BMC market in 2022.

Industrial Dielectrics Inc, LyondellBasell Industries NV, Menzolit GmBH, Mitsubishi Chemical Group Corp, Polynt SpA, Teijin Carbon Europe GmbH, Toray TCAC Holding BV, and YS ACC Co Ltd are some of the leading companies operating in the Asia Pacific carbon fiber-based SMC BMC market.

1. Industrial Dielectrics Inc

2. LyondellBasell Industries NV

3. Menzolit GmBH

4. Mitsubishi Chemical Group Corp

5. Polynt SpA

6. Teijin Carbon Europe GmbH

7. Toray TCAC Holding BV

8. YS ACC Co Ltd

The Asia Pacific Carbon Fiber-Based SMC BMC Market is valued at US$ 352.59 Million in 2022, it is projected to reach US$ 600.53 Million by 2030.

As per our report Asia Pacific Carbon Fiber-Based SMC BMC Market, the market size is valued at US$ 352.59 Million in 2022, projecting it to reach US$ 600.53 Million by 2030. This translates to a CAGR of approximately 6.9% during the forecast period.

The Asia Pacific Carbon Fiber-Based SMC BMC Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Carbon Fiber-Based SMC BMC Market report:

The Asia Pacific Carbon Fiber-Based SMC BMC Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Carbon Fiber-Based SMC BMC Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Carbon Fiber-Based SMC BMC Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Carbon Fiber-Based SMC BMC Market

Get Free Sample For Asia Pacific Carbon Fiber-Based SMC BMC Market