Asia Pacific Aviation Headsets Market

The commercial aviation sector has maintained a strong fleet size over the years, with Airbus and Boeing are the two most notable aircraft manufacturers in terms of delivery statistics. The commercial aviation industry has witnessed tremendous growth in the past few years with the emergence of new low-cost carriers (LCCs) and fleet expansion strategies adopted by the full-service carriers (FSCs). Further, commercial aviation is foreseen to surge in the coming years owing to the mounting number of air travel passengers and aircraft procurement. According to Boeing Commercial Market Outlook (CMO) 2019–2039, the total number of existing aircraft fleet in 2019 accounted for 25,900, and it is expected to reach 48,400 by 2039. As per Airbus Global Market Forecast, 2019–2038, the commercial aircraft fleet is foreseen to account for 47,680 by 2038, rising from 22,680 recorded at the beginning of 2019. However, the emergence of COVID-19 decimated the demand for aircraft in 2020, resulting in a significantly lower number of deliveries.

The aviation industry was hit hard in APAC region during the first half 2020 leading to massive decline in revenues across the stakeholders. The tremendous spread of the virus across the region resulted in airport closures, aircraft movement shut down, decline in revenue passenger kilometer (RPK), and lower aircraft MRO visits. Coupling all the parameters showcased fall in demand for aviation headsets across the aviation industry in the APAC region. China, the largest aviation industry in the region recovered post Q1 of 2020 and reached pre-COVID levels by the end of Q3 of 2020 in terms of domestic travel. This helped the Chinese market players to earn decent amount of revenues; however, the aviation industry in India, Japan, Australia, and others remained shattered until Q1 of 2021. Owing to this, the aviation headsets manufacturers present in these countries witnessed limited procurement of their products as observed by the international aviation headset market players. Moreover, after the introduction of new variant of COVID (Omicron) has also led to closure of international borders and travel restriction for South African country passengers across the European & APAC countries. For instance, in 2021, Germany has allowed its airlines companies to allow fly its citizens from the “high risk” southern African countries. The country has also made it mandatory for travelers visiting the country to spend mandatory 14-day quarantine, provided they test positive or negative for the virus. Similarly, the countries such as India, China, Australia, and Southeast Asian countries have also put cross-border restrictions for flights coming from African & other high OMICRON variant regions.

With the new features and technologies, vendors can attract new customers and expand their footprints in emerging markets. This factor is likely to drive the Asia Pacific aviation headsets. The Asia Pacific aviation headsets is expected to grow at a good CAGR during the forecast period.

")

Strategic insights for the Asia Pacific Aviation Headsets provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

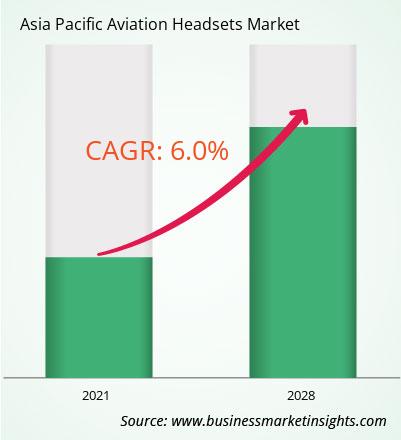

| Market size in 2021 | US$ 227.42 Million |

| Market Size by 2028 | US$ 342.01 Million |

| Global CAGR (2021 - 2028) | 6.0% |

| Historical Data | 2019-2020 |

| Forecast period | 2022-2028 |

| Segments Covered |

By Type

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Aviation Headsets refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Asia Pacific Aviation Headsets Market is valued at US$ 227.42 Million in 2021, it is projected to reach US$ 342.01 Million by 2028.

As per our report Asia Pacific Aviation Headsets Market, the market size is valued at US$ 227.42 Million in 2021, projecting it to reach US$ 342.01 Million by 2028. This translates to a CAGR of approximately 6.0% during the forecast period.

The Asia Pacific Aviation Headsets Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Aviation Headsets Market report:

The Asia Pacific Aviation Headsets Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Aviation Headsets Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Aviation Headsets Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Aviation Headsets Market

Get Free Sample For Asia Pacific Aviation Headsets Market