Asia Pacific Aircraft Turbine Fuel System Market

The APAC is market consists of Australia, China, India, Japan, South Korea, and rest of APAC. The Asia Pacific is characterized by the presence of an emerging nations with significant military expenditure and defense R&D investments, and favorable government initiatives, which boost the growth of the respective defense sector. According to Boeing, the region is expected to receive ~17,390 deliveries between 2019 and 2038. The total fleet is expected to increase to ~19,420 aircraft by 2038. In 2020, China, India, Japan, South Korea, and Australia were among the countries with the largest military spending in APAC, with the military expenditure of US$ 252 billion, US$ 65.86 billion, US$ 55 billion, US$ 44 billion, and US$ 27 billion, respectively. The increasing spending on military aircraft in China, Japan, and India through significant contracts to leading military aircraft manufacturers is expected to propel the adoption of aircraft turbine fuel system in the coming years. Further, the growing demand for aircrafts, particularly in developing countries such as China and India, drives the growth of the aircraft turbine fuel system market. The growth of the commercial aviation in APAC is attributed to rising middle class income, robust economic growth, and favorable government policies. For instance, government of India in March 2020, reduced GST (Goods and Service Tax) from 18% to 5% for MRO services in India. Further, the opening of Boeing and Airbus manufacturing/assembly plants, and upcoming indigenous commercial and regional aircraft such as COMAC C919 and Mitsubishi MRJ will boost the Asia Pacific aircraft turbine fuel system market in the coming years.

The COVID-19 outbreak has resulted in a massive financial loss to APAC countries. The governments of these countries have been continuously taking possible steps to reduce the intensity of the pandemic by announcing lockdown and rolling out physical distancing measures (post lockdown). China is one of the leading aerospace manufacturing countries in the region and has been one of worst-affected countries in the Q1 and Q2 of 2020. The Airbus and Boeing manufacturing facilities in China were shut down for a longer period, which resulted in substantially low demand for various components and systems, including turbine fuel systems. Similarly, COMAC, China’s indigenous aircraft manufacturer, halted its production of C919 during Q1. India, Japan, and South Korea are still combating the virus. However, the countries have eased the lockdown measures, which is reflecting the resumption of manufacturing facilities. Nonetheless, the remarkable lower volumes of air travel passengers have slowed down the demand for various components among the OEMs regionally and internationally. This has been negatively affecting the aircraft turbine fuel system market in APAC.

Strategic insights for the Asia Pacific Aircraft Turbine Fuel System provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

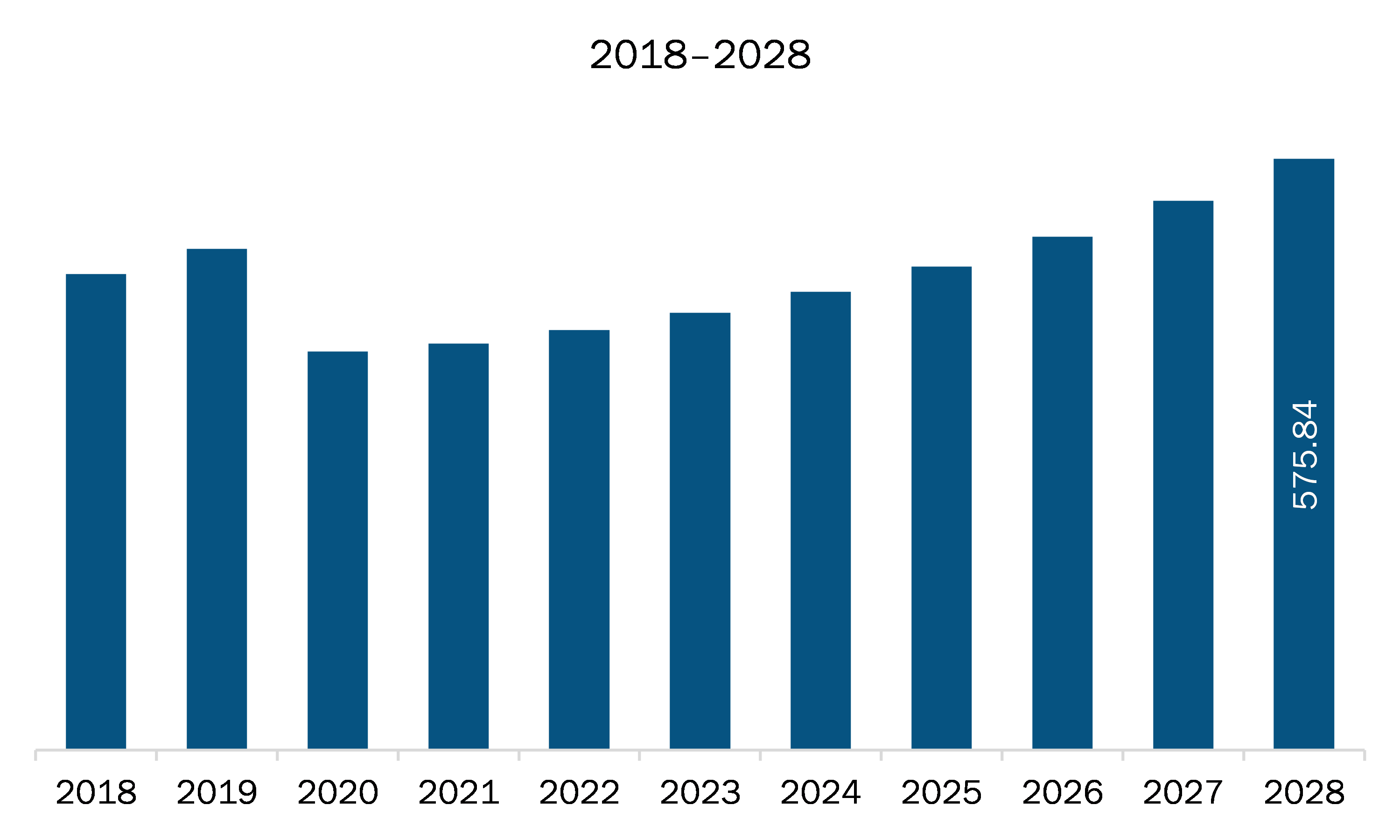

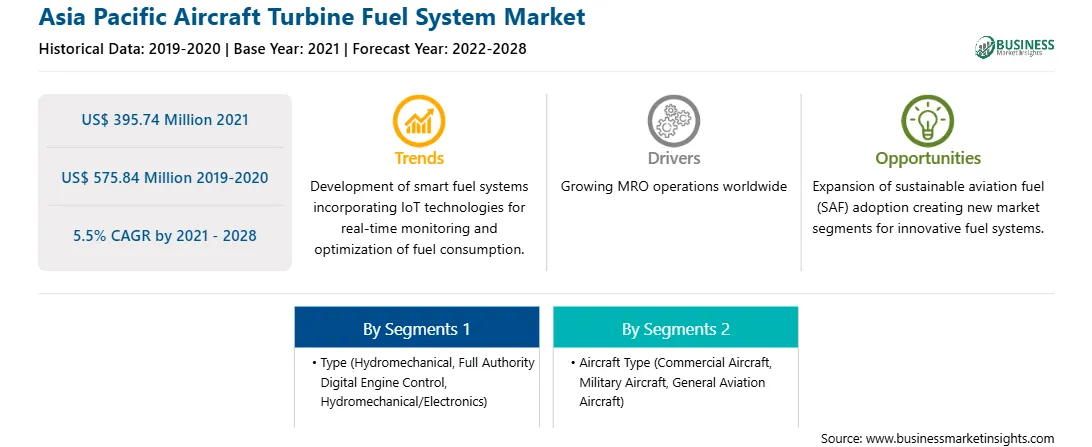

| Market size in 2021 | US$ 395.74 Million |

| Market Size by 2028 | US$ 575.84 Million |

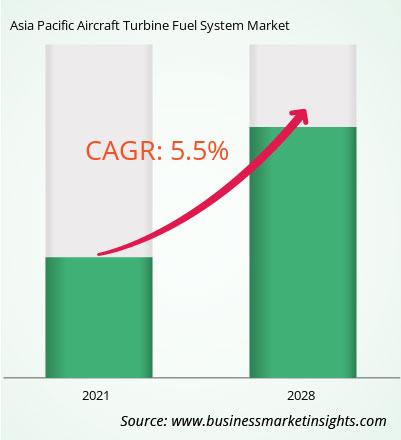

| Global CAGR (2021 - 2028) | 5.5% |

| Historical Data | 2019-2020 |

| Forecast period | 2022-2028 |

| Segments Covered |

By Type

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Aircraft Turbine Fuel System refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The aircraft turbine fuel system market in APAC is expected to grow from US$ 395.74 million in 2021 to US$ 575.84 million by 2028; it is estimated to grow at a CAGR of 5.5% from 2021 to 2028. Local manufacturers such as Hindustan Aeronautics Limited, Aviation Corporation of China, and Kawasaki Heavy Industries are also investing significantly to strengthen their position in the aviation industry. Thus, the growth of the aircraft turbine fuel system market in APAC is majorly attributed to the increasing aircraft fleet owing to the rising passenger traffic, mounting procurement of military aircraft with rising defense budget, and the ongoing projects of development of indigenous commercial and regional aircraft.

The APAC aircraft turbine fuel system market is segmented into type and aircraft type. Based on type, the aircraft turbine fuel system market is segmented into hydromechanical, full authority digital engine control (FADEC), and hydromechanical/electronics. The full authority digital engine control (FADEC) segment held the largest share in 2020 based on type. Based on aircraft type, the APAC aircraft turbine fuel system market is segmented as commercial aircraft, military aircraft, and general aviation aircraft. The military aircraft segment held the largest share in 2020.

A few major primary and secondary sources referred to for preparing this report on the aircraft turbine fuel system market in APAC are company websites, annual reports, financial reports, national government documents, and statistical database, among others. Major companies listed in the report are Collins Aerospace; Eaton Corporation plc; Honeywell International Inc.; Parker-Hannifin Corporation; Safran; Triumph Group, Inc.; and Woodward, Inc.

The Asia Pacific Aircraft Turbine Fuel System Market is valued at US$ 395.74 Million in 2021, it is projected to reach US$ 575.84 Million by 2028.

As per our report Asia Pacific Aircraft Turbine Fuel System Market, the market size is valued at US$ 395.74 Million in 2021, projecting it to reach US$ 575.84 Million by 2028. This translates to a CAGR of approximately 5.5% during the forecast period.

The Asia Pacific Aircraft Turbine Fuel System Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Aircraft Turbine Fuel System Market report:

The Asia Pacific Aircraft Turbine Fuel System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Aircraft Turbine Fuel System Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Aircraft Turbine Fuel System Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Aircraft Turbine Fuel System Market

Get Free Sample For Asia Pacific Aircraft Turbine Fuel System Market