Asia Pacific Aircraft Isothermal Forging Market

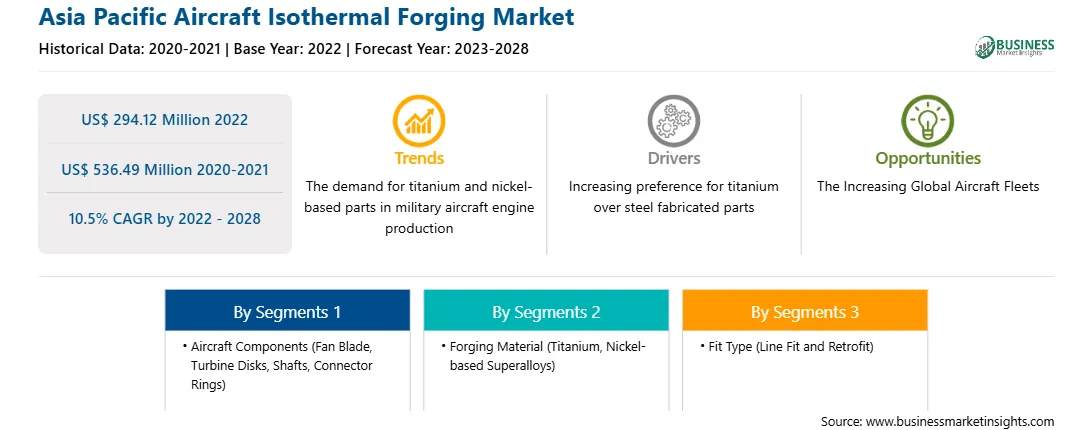

Adopting titanium and nickel-based parts across various applications in military aircraft production is a rising trend expected to propel the aircraft isothermal forging market. Higher demand for lightweight materials and increasing penetration of titanium and nickel-based engine parts usage per aircraft is on the rise. Furthermore, various components of military aircraft models and helicopters, such as flanges, ribs, skins, stringers, stiffeners, and shrouds, to form an aircraft engine structure are manufactured with the help of isothermally forging titanium or nickel alloys. For instance, in India, the Adour 804/811 and 871 engines that power the Indian Air Force’s Jaguar/Hawk aircraft use nickel-based and titanium-based alloys, which is expected to increase the demand for titanium and nickel-based parts. The thermal expansion rate of titanium makes it highly preferable as a composite interface material for military aircraft production. Moreover, titanium and nickel are known for their high strength-to-weight ratio, making them ideal materials for aircraft construction across the military aircraft manufacturing sectors. Furthermore, titanium and nickel-based parts are also corrosion-resistant, which makes them a good choice for use across military aircraft production. These lightweight and strong metals are suitable for manufacturing military aircraft and aircraft engine components. Thus, this trend is expected to boost the aircraft isothermal forging market growth during the forecast period.

The Asia Pacific aircraft isothermal forging market is segmented into aircraft components, forging material, fit type, and country. Based on aircraft components, the Asia Pacific aircraft isothermal forging market is segmented into fan blade, turbine disks, shafts, and connector rings. The fan blade segment is expected to account for the largest market share in 2022. Based on forging material, the Asia Pacific aircraft isothermal forging market is bifurcated into titanium and nickel-based superalloys. The nickel-based superalloy segment is expected to account for a larger market share in 2022. On the basis of fit type, the Asia Pacific aircraft isothermal forging market is categorized into line fit and retrofit segment. The line fit segment is expected to account for a larger market share in 2022. Based on country, the Asia Pacific aircraft isothermal forging market is segmented into Australia, China, India, Japan, South Korea, and the rest of Asia Pacific. China accounted for the largest share of the aircraft isothermal forging market in 2022.

Key players dominating the Asia Pacific aircraft isothermal forging market are Alcoa Corporation, ALD Vacuum Technologies GmbH, ATI, H.C. Starck Solutions, Howmet Aerospace, Leistritz Turbinentechnik GmbH, LISI Aerospace, SCHULER GROUP, and SMT Limited.

Strategic insights for the Asia Pacific Aircraft Isothermal Forging provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 294.12 Million |

| Market Size by 2028 | US$ 536.49 Million |

| Global CAGR (2022 - 2028) | 10.5% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Aircraft Components

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Aircraft Isothermal Forging refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Asia Pacific Aircraft Isothermal Forging Market is valued at US$ 294.12 Million in 2022, it is projected to reach US$ 536.49 Million by 2028.

As per our report Asia Pacific Aircraft Isothermal Forging Market, the market size is valued at US$ 294.12 Million in 2022, projecting it to reach US$ 536.49 Million by 2028. This translates to a CAGR of approximately 10.5% during the forecast period.

The Asia Pacific Aircraft Isothermal Forging Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Aircraft Isothermal Forging Market report:

The Asia Pacific Aircraft Isothermal Forging Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Aircraft Isothermal Forging Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Aircraft Isothermal Forging Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Aircraft Isothermal Forging Market

Get Free Sample For Asia Pacific Aircraft Isothermal Forging Market