Asia-Pacific Air Barrier Market

The popularity of fluid-applied air barriers is rapidly increasing, owing to their various advantages such as versatility, ease of application, and effectiveness even on irregular substrates. Fluid-applied air barriers are easier and faster to apply in comparison with sheet air barriers. These fuel-applied air barriers are used as self-adhered membranes, saving labor costs and time. Moreover, a fluid-applied membrane air barrier requires fewer applicators, which helps reduce labor costs. Fluid-applied air barriers eliminate the issues of tearing, holes, and mislapped joints and provide stable rigidity under air pressure loads. With a fluid-applied air barrier, there are no concerns about UV-ray degradation for up to six months, which is a concern with sheet-applied air barriers when stored outside. They found that fluid-applied air barriers were very popular for their ease of use compared to sheet membranes, and ~62% of applicators use fluid-applied air barrier coatings. Hence, the increasing use of fluid-applied air barriers is expected to Asia Pacific boost air barrier market growth.

Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific are the key contributors to the Asia Pacific air barrier market. The Indian government is keen on the major remodeling of public infrastructure and further expansion of development of the construction sector in the country. Alongside this, profit-bearing growth strategies and product innovations by many key players are projected to boost the sales of air barriers over the forecast period. Moreover, the significantly growing demand for air Barriers in the region is attributed to the presence of a strong industrial base that is making this region the workshop of the world. As regional pollution increases, air barriers will become essential in these areas. Awareness about personal care is growing among people, and as COVID-19 has hit these areas quite badly, these two factors boost growth for Asia Pacific air barrier market in the future.

Strategic insights for the Asia-Pacific Air Barrier provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

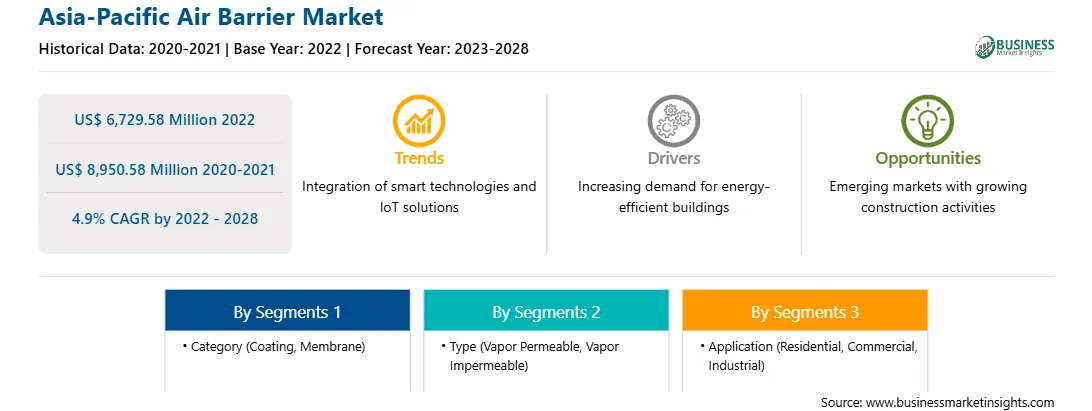

| Market size in 2022 | US$ 6,729.58 Million |

| Market Size by 2028 | US$ 8,950.58 Million |

| Global CAGR (2022 - 2028) | 4.9% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Category

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia-Pacific Air Barrier refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Asia Pacific air barrier market is segmented into category, type, application, and country. Based on category, the market is segmented into coating and membrane segment. The coating segment registered a larger market share in 2022.

3M Co; BASF SE; Carlisle Companies Inc; Dow Inc; GCP Applied Technologies Inc; General Electric Co; Henry Co; TK Products Construction Coating; VaproShield LLC; and W. R. Meadows Inc are the leading companies operating in the Asia Pacific air barrier market.

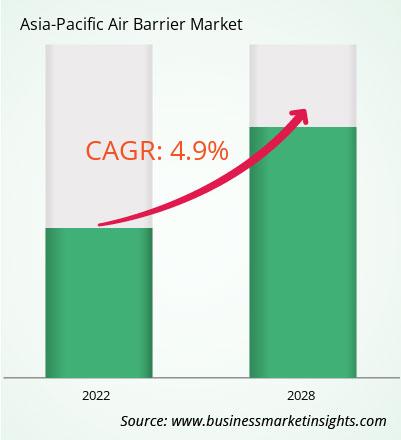

The Asia-Pacific Air Barrier Market is valued at US$ 6,729.58 Million in 2022, it is projected to reach US$ 8,950.58 Million by 2028.

As per our report Asia-Pacific Air Barrier Market, the market size is valued at US$ 6,729.58 Million in 2022, projecting it to reach US$ 8,950.58 Million by 2028. This translates to a CAGR of approximately 4.9% during the forecast period.

The Asia-Pacific Air Barrier Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia-Pacific Air Barrier Market report:

The Asia-Pacific Air Barrier Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia-Pacific Air Barrier Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia-Pacific Air Barrier Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia-Pacific Air Barrier Market

Get Free Sample For Asia-Pacific Air Barrier Market