Asia Pacific Advanced Composites Market

Bio-based polymer matrices are environment-friendly and are the subject of extensive research in various fields. Bio-based matrices are also lightweight and exhibit long-term sustainability, which drives their use in commercial applications. Further, the easy availability of natural raw materials to produce bio-based resin is fueling its supply and demand. Bio-based matrices and biocomposites are employed in several secondary applications in the aerospace, automobiles, packaging, electronics, and construction sectors. In the construction industry, biocomposites are generally used to produce doors, windows, terrace decking, insulation material, and acoustic components. According to the report from the Global Alliance for Building and Construction, construction is one of the most harmful sectors to the environment. The study conducted by the alliance at the end of 2019 stated that the construction sector is responsible for 39% of the carbon dioxide emissions dispersed in the environment, 36% of the consumption of energy, and 50% of the extraction of raw materials. Conventional construction materials are highly resource- and energy-intensive. Hence, owing to the rising concern and awareness about the social and environmental impacts of conventional building materials, manufacturers of composites are shifting toward environment-friendly raw materials. Thus, the growing adoption of bio-based matrices or resins, sourced from carbohydrates, vegetable fats and oils, starch, bacteria, and other biological materials, over petroleum-derived plastic matrices is expected to emerge as an important trend in the Asia Pacific advanced composites market during the forecast period.

The Asia Pacific advanced composites market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. In 2021, Asia Pacific holds the largest share of the global advanced composites market. The market growth in the region is attributed to the development of various end-use industries, including automotive, wind energy, marine, electrical & electronics, and construction. Asia Pacific is a hub for automotive manufacturing with a large presence of international and domestic players operating in the region. According to a report published by the China Passenger Car Association, in 2022, Tesla Inc delivered 83,135 made-in-China electric vehicles, indicating growth in sales of electric vehicles compared to 2021. As per the International Organization of Motor Vehicle Manufacturers report, in 2021, various countries in Asia Pacific produced ~46.73 million units of motor vehicles. Advanced composites are used in various automotive parts to reduce tooling costs and improve design flexibility for manufacturers, while enhancing fuel efficiency and overall driving experience for the consumer by reducing noise and vibration. Such benefits of advanced composites, coupled with the growing automotive industry, propel the market growth.

Strategic insights for the Asia Pacific Advanced Composites provides data-driven analysis of the industry landscape, including current trends, key players, and regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by identifying untapped segments or developing unique value propositions. Leveraging data analytics, these insights help industry players anticipate the market shifts, whether investors, manufacturers, or other stakeholders. A future-oriented perspective is essential, helping stakeholders anticipate market shifts and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

| Report Attribute | Details |

|---|---|

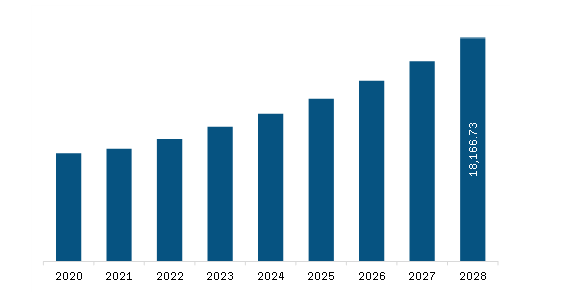

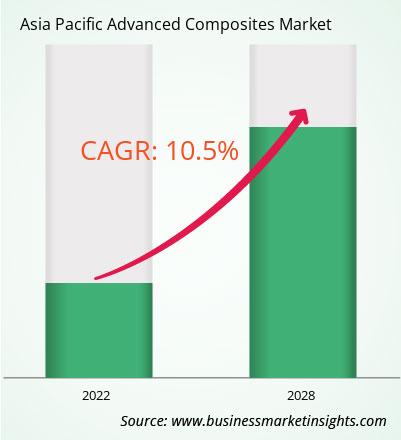

| Market size in 2022 | US$ 9,990.80 Million |

| Market Size by 2028 | US$ 18,166.73 Million |

| Global CAGR (2022 - 2028) | 10.5% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Fiber Type

|

| Regions and Countries Covered | Asia-Pacific

|

| Market leaders and key company profiles |

The geographic scope of the Asia Pacific Advanced Composites refers to the specific areas in which a business operates and competes. Understanding local distinctions, such as diverse consumer preferences (e.g., demand for specific plug types or battery backup durations), varying economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved areas or adapting their offerings to meet local demands. A clear market focus allows for more effective resource allocation, targeted marketing campaigns, and better positioning against local competitors, ultimately driving growth in those targeted areas.

The Asia Pacific advanced composites market is segmented based on fiber type, matrix type, end-use industry, and country.

Based on fiber type, the Asia Pacific advanced composites market is segmented into carbon fiber composites, aramid fiber composites, glass fiber composites, and others. The carbon fiber composites segment held the largest share of the Asia Pacific advanced composites market in 2022.

Based on matrix type, the Asia Pacific advanced composites market is segmented into epoxy resin, phenolics, polyester resin, polyurethane resin, polyphenylene sulfide (PPS), polyetherimide (PEI), and others. The epoxy resin segment held the largest share of the Asia Pacific advanced composites market in 2022.

Based on end-use industry, the Asia Pacific advanced composites market is segmented into aerospace & defense, automotive, wind energy, building & construction, electrical & electronics, and others. The aerospace & defense segment held the largest share of the Asia Pacific advanced composites market in 2022.

Based on country, the Asia Pacific advanced composites market has been categorized into China, India, Japan, South Korea, Australia, and the Rest of Asia Pacific. Our regional analysis states that China dominated the Asia Pacific advanced composites market in 2022.

Avient Corp, Ensinger GmbH, Johns Manville Corp, Mitsubishi Chemical Corp, Owens Corning, SGL Carbon SE, Solvay SA, Teijin Ltd, and Toray Industries Inc are the leading companies operating in the Asia Pacific advanced composites market.

The Asia Pacific Advanced Composites Market is valued at US$ 9,990.80 Million in 2022, it is projected to reach US$ 18,166.73 Million by 2028.

As per our report Asia Pacific Advanced Composites Market, the market size is valued at US$ 9,990.80 Million in 2022, projecting it to reach US$ 18,166.73 Million by 2028. This translates to a CAGR of approximately 10.5% during the forecast period.

The Asia Pacific Advanced Composites Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Advanced Composites Market report:

The Asia Pacific Advanced Composites Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Advanced Composites Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Advanced Composites Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Advanced Composites Market

Get Free Sample For Asia Pacific Advanced Composites Market