北米細胞および遺伝子治療製造サービス市場 2030 年までの予測 - 地域分析 - タイプ別 [細胞治療 (自己および同種) および遺伝子治療 (ウイルスおよび非ウイルスベクター)]、適応症 (がん、整形外科、その他)、用途別(臨床製造および商業製造)、およびエンドユーザー [製薬企業およびバイオテクノロジー企業および受託研究機関 (CRO)]

No. of Pages: 110 | Report Code: BMIRE00029298 | Category: Life Sciences

No. of Pages: 110 | Report Code: BMIRE00029298 | Category: Life Sciences

細胞および遺伝子治療製造は複雑なプロセスであるため、作業の適切な実行と監督が重要になります。細胞および遺伝子治療のメーカーには、生物学およびプロセス工学に精通した資格のある人材の数が限られています。さらに、経験豊富なチームにとって、マニュアルとオープンな製造方法を使用して最初の臨床試験に到達する試みを管理し、その後、より商業的に適切なプロセスを構築するのは難しい場合があります。したがって、これらの企業は、臨床研究と商品化プロセスを加速するために、受託開発製造組織 (CDMO) と協力することを選択します。 CDMO は、製品開発、製造、臨床試験サポート、および商品化サービスを細胞および遺伝子治療会社に契約ベースで提供します。 CDMO と提携することで、細胞治療および遺伝子治療のメーカーは拡張性、市場投入までのスピード、諸経費なしでの技術的専門知識へのアクセス、コスト効率の向上が可能になります。 2022年4月、サーモジェネシスは米国カリフォルニア州にCDMO施設を設立し、T細胞受容体(TCR)、キメラ抗原受容体T細胞(CAR-T細胞)、腫瘍に関する専門知識を活用して細胞および遺伝子治療のメーカーにCDMOサービスを提供しました。 -浸潤性白血球(TIL)、iPSC、ナチュラルキラー細胞(NK)、間葉系幹細胞(MSC)の製造。細胞および遺伝子治療薬の製造を CDMO に委託することは、メーカーにとってコスト効率が高いことが証明されています。したがって、成長中の細胞および遺伝子治療薬の製造を CDMO にアウトソーシングする傾向が高まっており、北米の細胞および遺伝子治療薬の製造サービス市場の成長が促進されています。

細胞および遺伝子治療 (CGT) は、治療ニーズが満たされていない重篤な希少疾患に苦しむ患者を治療します。 CGT の製造は非常に複雑なプロセスであり、インフラストラクチャと専門知識の不足が大きな制限要因となっています。中間体や最終製品に関連する物流上の課題も、企業の CGT 製造能力を制限します。 CGT の製造プロセスには、「アフェレーシス」による自己細胞の抽出、それを専門の研究室に送り、患者に投与するために診療所に返送することが含まれますが、これらすべての作業は厳格な品質管理のもとで行われなければなりません。米国食品医薬品局 (USFDA) が承認した CGT 薬は 7 種類のみで、新製品のパイプラインは約 1,200 の実験的治療法に達しています。このうち半数は第 2 相臨床試験中であり、化学薬品業界の推定によると、年間売上高の伸びは細胞治療で 15%、遺伝子治療で約 30% を占めると推定されています。 Engineering News report 2022。2022 年 3 月 31 日、CELL Technologies Inc. は、患者が科学的根拠に基づいた規制当局が承認した幹細胞処置を利用できるようにするため、疼痛および関節炎における幹細胞プログラムの臨床データをカナダ保健省の承認を求めて提出したと発表しました。カナダ全土。したがって、上記の要因は、予測期間中に細胞および遺伝子治療薬製造サービス市場の成長を促進すると予想されます。したがって、上記の要因は、北米の細胞および遺伝子治療の製造サービス市場の成長に貢献します。

北米の細胞および遺伝子治療の製造サービス市場は分割されています。

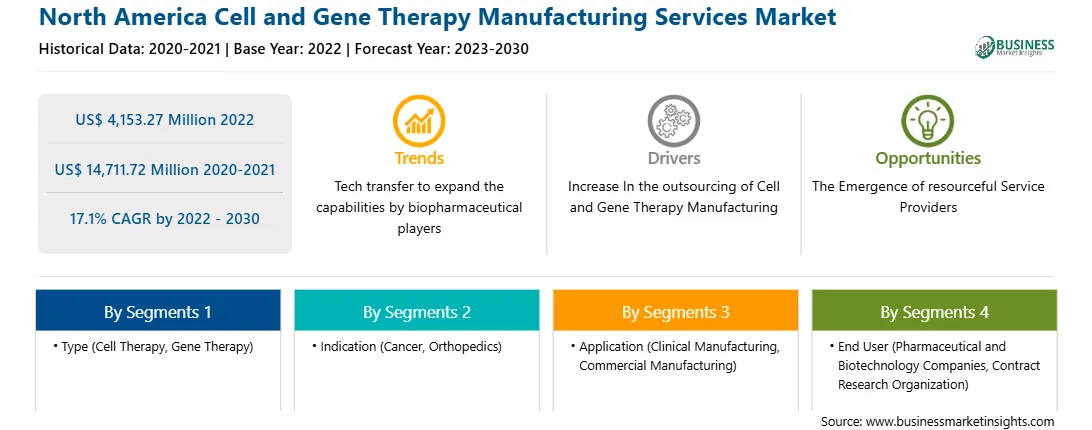

種類に基づいて、北米の細胞および遺伝子治療の製造サービス市場は、細胞治療と遺伝子治療に二分されます。 2022 年には、細胞治療部門が北米の細胞および遺伝子治療製造サービス市場で大きなシェアを記録しました。細胞療法セグメントは、さらに自己細胞と同種異系細胞に分類されます。遺伝子治療セグメントは、ウイルスベクターと非ウイルスベクターにさらに分類されます。

適応症に基づいて、北米の細胞および遺伝子治療製造サービス市場はがん、整形外科などに分類されます。 2022 年、がんセグメントは北米の細胞および遺伝子治療製造サービス市場で最大のシェアを記録しました。

アプリケーションに基づいて、北米の細胞および遺伝子治療製造サービス市場は臨床製造と商用に分類されます。製造業。 2022 年、商用製造部門は北米の細胞および遺伝子治療の製造サービス市場で最大のシェアを記録しました。

エンドユーザーに基づいて、北米の細胞および遺伝子治療の製造サービス市場は医薬品と遺伝子治療に二分されます。バイオテクノロジー企業と受託研究機関 (CRO)。 2022 年、北米の細胞および遺伝子治療製造サービス市場では、製薬会社およびバイオテクノロジー企業セグメントがより大きなシェアを記録しました。

国に基づいて、北米の細胞および遺伝子治療製造サービス市場は次のように分類されます。アメリカ、カナダ、メキシコ。 2022 年、米国は北米の細胞および遺伝子治療薬製造サービス市場で最大のシェアを記録しました。

Catalent Inc、Charles River Laboratories International Inc、富士フイルム ホールディングス株式会社、Lonza Group AG、Merck KgaA、National Resilience Inc、Nikon Corp、Oxford BioMedica Plc、Takara Bio Inc、Thermo Fisher Scientific Inc、WuXi AppTec Co Ltd は、北米の細胞および遺伝子治療薬製造サービス市場で事業を展開する大手企業です。

Strategic insights for North America Cell and Gene Therapy Manufacturing Services involve closely monitoring industry trends, consumer behaviours, and competitor actions to identify opportunities for growth. By leveraging data analytics, businesses can anticipate market shifts and make informed decisions that align with evolving customer needs. Understanding these dynamics helps companies adjust their strategies proactively, enhance customer engagement, and strengthen their competitive edge. Building strong relationships with stakeholders and staying agile in response to changes ensures long-term success in any market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 4,153.27 Million |

| Market Size by 2030 | US$ 14,711.72 Million |

| Global CAGR (2022 - 2030) | 17.1% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By タイプ

|

| Regions and Countries Covered | 北米

|

| Market leaders and key company profiles |

The regional scope of North America Cell and Gene Therapy Manufacturing Services refers to the geographical area in which a business operates and competes. Understanding regional nuances, such as local consumer preferences, economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved regions or adapting their offerings to meet regional demands. A clear regional focus allows for more effective resource allocation, targeted marketing, and better positioning against local competitors, ultimately driving growth in those specific areas.

1. Catalent Inc

2. Charles River Laboratories International Inc

3. FUJIFILM Holdings Corp

4. Lonza Group AG

5. Merck KgaA

6. National Resilience Inc

7. Nikon Corp

8. Oxford BioMedica Plc

9. Takara Bio Inc

10. Thermo Fisher Scientific Inc

11. WuXi AppTec Co Ltd?

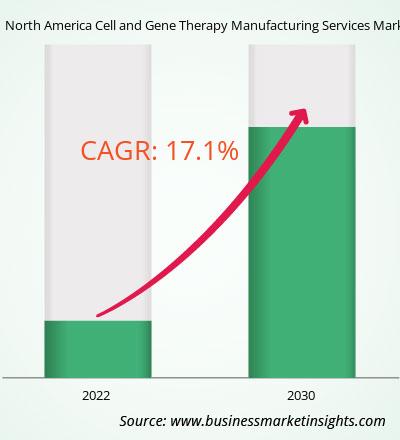

The North America Cell and Gene Therapy Manufacturing Services Market is valued at US$ 4,153.27 Million in 2022, it is projected to reach US$ 14,711.72 Million by 2030.

As per our report North America Cell and Gene Therapy Manufacturing Services Market, the market size is valued at US$ 4,153.27 Million in 2022, projecting it to reach US$ 14,711.72 Million by 2030. This translates to a CAGR of approximately 17.1% during the forecast period.

The North America Cell and Gene Therapy Manufacturing Services Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Cell and Gene Therapy Manufacturing Services Market report:

The North America Cell and Gene Therapy Manufacturing Services Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Cell and Gene Therapy Manufacturing Services Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Cell and Gene Therapy Manufacturing Services Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Cell and Gene Therapy Manufacturing Services Market

Get Free Sample For North America Cell and Gene Therapy Manufacturing Services Market