Prévisions du marché européen des infrastructures de gazoducs jusqu’en 2030 – Analyse régionale – par opération (transmission et distribution), équipement (pipeline, station de compression, skids de comptage et autres) et application (onshore et offshore)

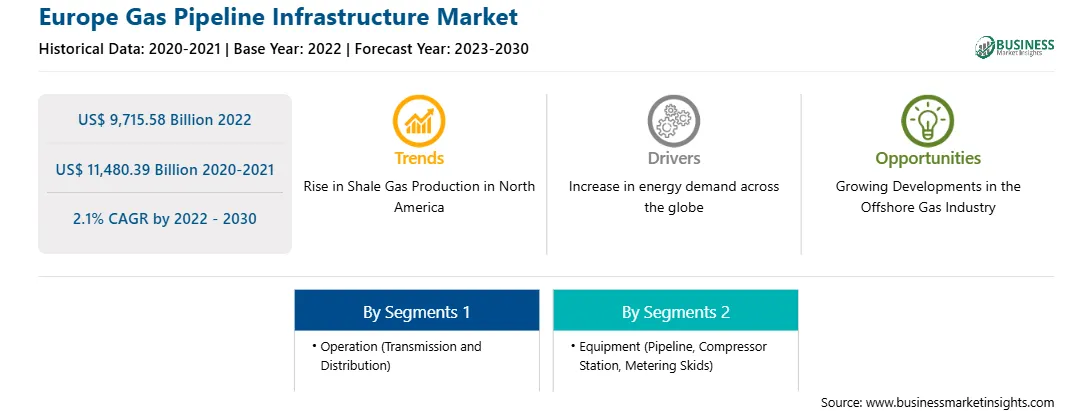

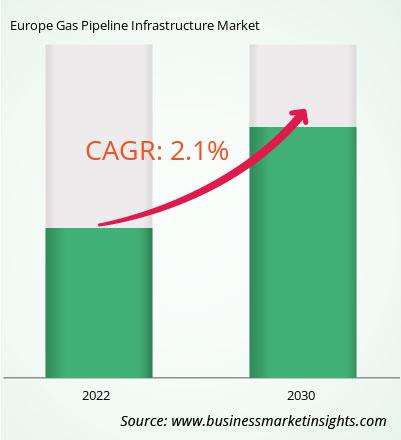

Le marché européen des infrastructures de gazoducs devrait passer de 9 715,58 milliards de dollars américains en 2022 à 11 480,39 milliards de dollars américains d\'ici 2030. Il devrait enregistrer un TCAC de 2,1 % de 2022 à 2030.

Intégration avec les énergies renouvelables Stimule le marché européen des infrastructures de gazoducs. L\'intégration avec les énergies renouvelables implique de tirer parti des gazoducs pour soutenir la nature intermittente des sources renouvelables telles que l\'énergie solaire et éolienne. Cette intégration offre aux exploitants de pipelines la possibilité de collaborer avec les développeurs d\'énergies renouvelables et d\'investir dans des infrastructures qui complètent la production d\'énergies renouvelables. Par exemple, les centrales électriques au gaz peuvent assurer la stabilité du réseau pendant les périodes de faible production d’énergie renouvelable, réduisant ainsi la dépendance aux combustibles fossiles et les émissions de carbone. De plus, les progrès technologiques tels que le power-to-gas permettent de convertir l’excédent d’énergie renouvelable en hydrogène ou en gaz naturel synthétique, qui peut être stocké dans des pipelines pour une utilisation ultérieure. En intégrant les gazoducs aux sources d’énergie renouvelables, les entreprises peuvent contribuer aux efforts de décarbonation, améliorer la sécurité énergétique et soutenir la transition vers un système énergétique plus durable.

Aperçu du marché européen des infrastructures de gazoducs

La Russie, l\'Allemagne, la France et l\'Espagne font partie des principaux pays qui contribuent à la croissance globale du marché des infrastructures de gazoducs en Europe. Les politiques et mandats gouvernementaux conformes aux objectifs de zéro émission nette de carbone et d’énergie propre créent une demande d’infrastructures durables, y compris des réseaux de gazoducs. Dans l’Union européenne, le taux de dioxyde de carbone dans le secteur de l’électricité s’est considérablement intensifié en 2022. Quelques pays ont repris l’exploitation de centrales électriques au charbon, tandis que les pannes de centrales nucléaires et la faible production d’hydroélectricité ont renforcé la fiabilité du gaz naturel. Conformément à l\'Accord de Paris, qui a impliqué 196 participants à la Conférence des Nations Unies sur les changements climatiques (COP21) à Paris, en France, en 2015, le gouvernement met en place des politiques de zéro émission nette et d\'énergie verte. La part croissante des ressources énergétiques à faibles émissions de carbone dans le mix énergétique et le secteur industriel sont des facteurs déterminants pour le marché des infrastructures de gazoducs dans la région. Le développement de nouvelles infrastructures de gazoducs et l’augmentation de la capacité des gazoducs existants sont également susceptibles d’alimenter la croissance du marché des infrastructures de gazoducs en Europe au cours de la période de prévision. L\'Allemagne a connu une croissance lente de sa production de gaz jusqu\'à fin 2022 en raison de la rareté des ressources gazières dans les zones minières du pays. Le pays dépend principalement des importations en provenance de différents pays, tels que les États-Unis, l\'Italie, le Royaume-Uni et la Norvège. Elle importe environ 70 % de ses besoins énergétiques, car sa production nationale ne couvre qu’environ 6 % de sa consommation de gaz. En 2023, les gouvernements allemand et italien ont collaboré pour former un projet de gazoduc. Le gazoduc proposé est un projet de 3 300 km et devrait intégrer quatre gestionnaires de réseau de transport européens, dont Trans Austria Gasleitung, Snam, Bayernets et Gas Connect Austria en Allemagne. Ainsi, le développement du nouveau gazoduc et l’entretien du réseau gazier existant devraient stimuler le développement de l’infrastructure des gazoducs en Allemagne au cours de la période de prévision.

Revenus et prévisions du marché européen des infrastructures de gazoducs jusqu\'en 2030 (milliards de dollars américains)

Segmentation du marché européen des infrastructures de gazoducs

Le marché européen des infrastructures de gazoducs est segmenté en exploitation, équipement, application et pays.

Sur la base de l\'exploitation, le marché européen des infrastructures de gazoducs est divisé en transport et distribution. Le segment de distribution détenait une part plus importante du marché européen des infrastructures de gazoducs en 2022.

En termes d\'équipement, le marché européen des infrastructures de gazoducs est classé en pipelines, stations de compression, skids de comptage et vannes. Le segment des gazoducs détenait la plus grande part du marché européen des infrastructures de gazoducs en 2022.

Sur la base des applications, le marché européen des infrastructures de gazoducs est divisé en onshore et offshore. Le segment terrestre détenait une part plus importante du marché européen des infrastructures de gazoducs en 2022.

En fonction des pays, le marché européen des infrastructures de gazoducs est segmenté en Allemagne, France, Italie, Espagne, Russie, Royaume-Uni et Le reste de l\'Europe. Le reste de l\'Europe a dominé le marché européen des infrastructures de gazoducs en 2022.

Enbridge Inc, Berkshire Hathaway Inc, Kinder Morgan Inc, Beltps, Enagas SA et Saipem SpA font partie des principales sociétés opérant dans le secteur gazier européen. marché des infrastructures de pipelines.

Europe Gas Pipeline Infrastructure Strategic Insights

Strategic insights for Europe Gas Pipeline Infrastructure involve closely monitoring industry trends, consumer behaviours, and competitor actions to identify opportunities for growth. By leveraging data analytics, businesses can anticipate market shifts and make informed decisions that align with evolving customer needs. Understanding these dynamics helps companies adjust their strategies proactively, enhance customer engagement, and strengthen their competitive edge. Building strong relationships with stakeholders and staying agile in response to changes ensures long-term success in any market.

Get more information on this report

Europe Gas Pipeline Infrastructure Report Scope

Report Attribute

Details

Market size in 2022

US$ 9,715.58 Billion

Market Size by 2030

US$ 11,480.39 Billion

Global CAGR (2022 - 2030)

2.1%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Exploitation

Transport et Distribution

By Équipement

pipeline

station de compression

skids de mesure

Regions and Countries Covered

Europe

Royaume-Uni

Allemagne

France

Russie

Italie

reste de Europe

Market leaders and key company profiles

Enbridge Inc

Berkshire Hathaway Inc

Kinder Morgan Inc

Beltps

Enagas SA

Saipem SpA

Get more information on this report

Europe Gas Pipeline Infrastructure Regional Insights

The regional scope of Europe Gas Pipeline Infrastructure refers to the geographical area in which a business operates and competes. Understanding regional nuances, such as local consumer preferences, economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved regions or adapting their offerings to meet regional demands. A clear regional focus allows for more effective resource allocation, targeted marketing, and better positioning against local competitors, ultimately driving growth in those specific areas.

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Europe Gas Pipeline Infrastructure Market

1. Enbridge Inc 2. Berkshire Hathaway Inc 3. Kinder Morgan Inc 4. Beltps 5. Enagas SA 6. Saipem SpA

Frequently Asked Questions

How big is the Europe Gas Pipeline Infrastructure Market?

The Europe Gas Pipeline Infrastructure Market is valued at US$ 9,715.58 Billion in 2022, it is projected to reach US$ 11,480.39 Billion by 2030.

What is the CAGR for Europe Gas Pipeline Infrastructure Market by (2022 - 2030)?

As per our report Europe Gas Pipeline Infrastructure Market, the market size is valued at US$ 9,715.58 Billion in 2022, projecting it to reach US$ 11,480.39 Billion by 2030. This translates to a CAGR of approximately 2.1% during the forecast period.

What segments are covered in this report?

The Europe Gas Pipeline Infrastructure Market report typically cover these key segments-

Exploitation (Transport et Distribution)

Équipement (pipeline, station de compression, skids de mesure)

What is the historic period, base year, and forecast period taken for Europe Gas Pipeline Infrastructure Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Gas Pipeline Infrastructure Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2030

Who are the major players in Europe Gas Pipeline Infrastructure Market?

The Europe Gas Pipeline Infrastructure Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Enbridge Inc

Berkshire Hathaway Inc

Kinder Morgan Inc

Beltps

Enagas SA

Saipem SpA

Who should buy this report?

The Europe Gas Pipeline Infrastructure Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Gas Pipeline Infrastructure Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Gas Pipeline Infrastructure Market

1. Complete the form

2. Check your inbox (and spam/junk folder)

3. Your Personal Data is Secure with us

GDPR + CCPA Compliant

Personal & transactional information is kept safe from unauthorized use.

WHAT'S INCLUDED IN FULL REPORT : Market Dynamics,

Competitive Analysis and Assessment, Define Business Strategies, Market Outlook and

Trends, Market Size and Share Analysis, Growth Driving Factors, Future Commercial

Potential, Identify Regional Growth Engines

Get Free Sample For Europe Gas Pipeline Infrastructure Market

Get Free Sample For Europe Gas Pipeline Infrastructure Market