Pronóstico del mercado de almacenamiento de datos de próxima generación de América del Norte hasta 2030 – Análisis regional – por sistema de almacenamiento [almacenamiento conectado directo (DAS), almacenamiento conectado a la red (NAS) y red de área de almacenamiento (SAN)], usuario final (BFSI, comercio minorista, TI y telecomunicaciones, atención médica, medios y entretenimiento, y otros), medio de almacenamiento (disco duro, unidad de estado sólido y cinta), arquitectura de almacenamiento (almacenamiento basado en archivos-objetos y almacenamiento en bloque) e implementación (en las instalaciones, en la nube). -basado e híbrido)

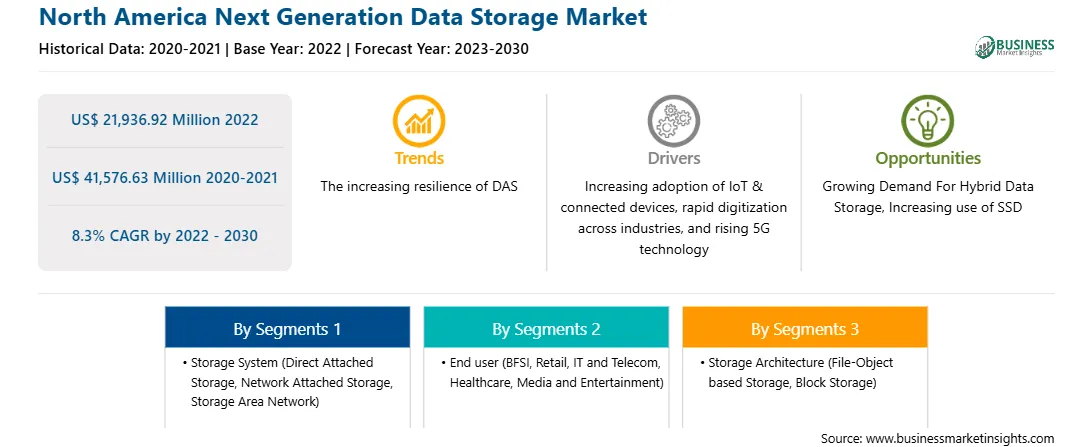

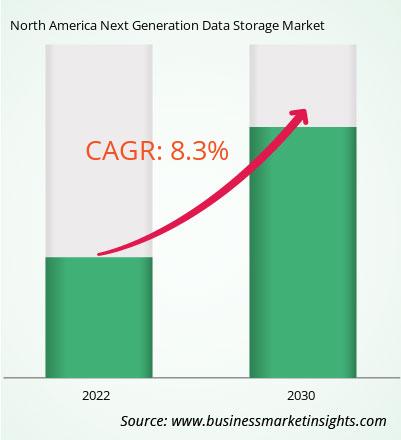

El mercado de almacenamiento de datos de próxima generación de América del Norte se valoró en 21.936,92 millones de dólares en 2022 y se espera que alcance los 41.576,63 millones de dólares en 2030; se estima que registrará una tasa compuesta anual del 8,3% entre 2022 y 2030.

La creciente adopción de IoT y dispositivos conectados impulsa el mercado de almacenamiento de datos de próxima generación en América del Norte

La creciente penetración de Internet de las cosas (IoT) en industrias como la manufactura, la atención médica y el comercio minorista está respaldando la implementación de la computación en la nube. IoT es un aspecto importante de diversas aplicaciones, ya que puede utilizarse para simplificar la gestión remota y monitorear los activos móviles. Por ejemplo, una organización que alquila inversores potentes puede utilizar IoT para gestionar el inventario, realizar un seguimiento de la maquinaria, modelar su cadena de suministro, facturar a los clientes y más. Además, la fabricación es uno de los sectores empresariales que más se beneficia del IoT. Los gerentes de planta y los trabajadores pueden obtener información sin precedentes relacionada con sus instalaciones y equipos mediante la implementación de una multitud de sensores. También puede reducir la necesidad de que los empleados accedan o inspeccionen físicamente los equipos en situaciones potencialmente peligrosas.

Miles de millones de dispositivos IoT generan continuamente datos de sensores, lo que se prevé creará una avalancha de datos sin precedentes. Las soluciones de almacenamiento tradicionales no serán suficientes para impulsar la demanda de tecnologías de próxima generación escalables y rentables.

Según un análisis de ZScaler, a nivel mundial habrá más de 29 mil millones de dispositivos IoT conectados para 2027, frente a 16,7 mil millones en 2023. El sector manufacturero generó el mayor volumen de tráfico de dispositivos IoT, ya que las empresas utilizan tecnología inteligente. para satisfacer las demandas modernas de innovación en la cadena de suministro. Por lo tanto, la creciente adopción de dispositivos conectados a IoT impulsa el mercado de almacenamiento de datos de próxima generación.

Descripción general del mercado de almacenamiento de datos de próxima generación de América del Norte

América del Norte se ha establecido como un actor destacado en el mercado de almacenamiento de datos de próxima generación debido a varios factores. América del Norte cuenta con una sólida infraestructura tecnológica y alberga varios gigantes tecnológicos y nuevas empresas innovadoras. La sólida economía de la región impulsa las inversiones en investigación y desarrollo, ayudando al desarrollo de tecnologías de almacenamiento de datos de vanguardia. Además, América del Norte tiene un gran enfoque en industrias con uso intensivo de datos, como el comercio electrónico, la atención médica y las finanzas, generando grandes cantidades de datos que requieren soluciones de almacenamiento económicas. Las políticas y regulaciones gubernamentales positivas respaldan el crecimiento del mercado de almacenamiento de datos en América del Norte. La presencia de una población conocedora de la tecnología y de los primeros en adoptar tecnologías emergentes también contribuye al mercado de almacenamiento de datos de próxima generación de América del Norte. El importante volumen de datos no estructurados de la región en varios sectores verticales de la industria y la necesidad de soluciones de almacenamiento de datos seguras y rentables impulsan aún más las perspectivas de crecimiento del mercado de América del Norte. En general, América del Norte tiene una participación sustancial en el mercado de almacenamiento de datos de próxima generación, impulsada por su destreza tecnológica, industrias con uso intensivo de datos, políticas favorables y una población que adopta nuevas tecnologías.

Ingresos del mercado de almacenamiento de datos de próxima generación de América del Norte y pronóstico hasta 2030 (millones de dólares estadounidenses)

Segmentación del mercado de almacenamiento de datos de próxima generación de América del Norte

Segmentación del mercado de almacenamiento de datos de próxima generación de América del Norte El mercado se clasifica en sistema de almacenamiento, usuario final, medio de almacenamiento, arquitectura de almacenamiento, implementación y país.

Basado en el sistema de almacenamiento, el mercado de almacenamiento de datos de próxima generación de América del Norte se segmenta en almacenamiento conectado directo (DAS), almacenamiento conectado a la red (NAS) y red de área de almacenamiento (SAN). El segmento de almacenamiento adjunto directo (DAS) tuvo la mayor cuota de mercado de almacenamiento de datos de próxima generación de América del Norte en 2022.

En términos de usuario final, el mercado de almacenamiento de datos de próxima generación de América del Norte está segmentado en BFSI, comercio minorista y TI. y telecomunicaciones, atención médica, medios y entretenimiento, y otros. El segmento BFSI tuvo la mayor cuota de mercado de almacenamiento de datos de próxima generación de América del Norte en 2022.

Por medio de almacenamiento, el mercado de almacenamiento de datos de próxima generación de América del Norte se divide en unidad de disco duro, unidad de estado sólido y cinta. El segmento de unidades de estado sólido tuvo la mayor participación de mercado de almacenamiento de datos de próxima generación en América del Norte en 2022.

Según la arquitectura de almacenamiento, el mercado de almacenamiento de datos de próxima generación de América del Norte se divide en almacenamiento basado en archivos y objetos y almacenamiento en bloques. . El segmento de almacenamiento basado en archivos-objetos tuvo una mayor participación en el mercado de almacenamiento de datos de próxima generación de América del Norte en 2022.

Por implementación, el mercado de almacenamiento de datos de próxima generación de América del Norte se clasifica en local, basado en la nube y híbrido. El segmento local tuvo la mayor cuota de mercado de almacenamiento de datos de próxima generación de América del Norte en 2022.

Por país, el mercado de almacenamiento de datos de próxima generación de América del Norte está segmentado en EE. UU., Canadá y México. Estados Unidos dominó la cuota de mercado de almacenamiento de datos de próxima generación de América del Norte en 2022.

Dell Technologies Inc, Hewlett Packard Enterprise Co, NetApp Inc, Hitachi Ltd, International Business Machines Corp, Pure Storage Inc, DataDirect Networks Inc, Fujitsu Ltd, NETGEAR y Huawei Technologies Co Ltd son algunas de las empresas líderes que operan en el mercado de almacenamiento de datos de próxima generación de América del Norte.

North America Next Generation Data Storage Strategic Insights

Strategic insights for North America Next Generation Data Storage involve closely monitoring industry trends, consumer behaviours, and competitor actions to identify opportunities for growth. By leveraging data analytics, businesses can anticipate market shifts and make informed decisions that align with evolving customer needs. Understanding these dynamics helps companies adjust their strategies proactively, enhance customer engagement, and strengthen their competitive edge. Building strong relationships with stakeholders and staying agile in response to changes ensures long-term success in any market.

Get more information on this report

North America Next Generation Data Storage Report Scope

Report Attribute

Details

Market size in 2022

US$ 21,936.92 Million

Market Size by 2030

US$ 41,576.63 Million

Global CAGR (2022 - 2030)

8.3%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Sistema de almacenamiento

almacenamiento conectado directamente

almacenamiento conectado a red

red de área de almacenamiento

By Usuario final

BFSI

Comercio minorista

TI y telecomunicaciones

Salud

Medios y entretenimiento

By Arquitectura de almacenamiento

almacenamiento basado en archivos y objetos

almacenamiento en bloques

Regions and Countries Covered

América del Norte

EE. UU.

Canadá

México

Market leaders and key company profiles

Dell Technologies Inc

Hewlett Packard Enterprise Co

NetApp Inc

Hitachi Ltd

International Business Machines Corp

Pure Storage Inc

DataDirect Networks Inc

Fujitsu Ltd

NETGEAR

Huawei Technologies Co Ltd

Get more information on this report

North America Next Generation Data Storage Regional Insights

The regional scope of North America Next Generation Data Storage refers to the geographical area in which a business operates and competes. Understanding regional nuances, such as local consumer preferences, economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved regions or adapting their offerings to meet regional demands. A clear regional focus allows for more effective resource allocation, targeted marketing, and better positioning against local competitors, ultimately driving growth in those specific areas.

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - North America Next Generation Data Storage Market

1. Dell Technologies Inc 2. Hewlett Packard Enterprise Co 3. NetApp Inc 4. Hitachi Ltd 5. International Business Machines Corp 6. Pure Storage Inc 7. DataDirect Networks Inc 8. Fujitsu Ltd 9. NETGEAR 10. Huawei Technologies Co Ltd

Frequently Asked Questions

How big is the North America Next Generation Data Storage Market?

The North America Next Generation Data Storage Market is valued at US$ 21,936.92 Million in 2022, it is projected to reach US$ 41,576.63 Million by 2030.

What is the CAGR for North America Next Generation Data Storage Market by (2022 - 2030)?

As per our report North America Next Generation Data Storage Market, the market size is valued at US$ 21,936.92 Million in 2022, projecting it to reach US$ 41,576.63 Million by 2030. This translates to a CAGR of approximately 8.3% during the forecast period.

What segments are covered in this report?

The North America Next Generation Data Storage Market report typically cover these key segments-

Sistema de almacenamiento (almacenamiento conectado directamente, almacenamiento conectado a red, red de área de almacenamiento)

Usuario final (BFSI, Comercio minorista, TI y telecomunicaciones, Salud, Medios y entretenimiento)

Arquitectura de almacenamiento (almacenamiento basado en archivos y objetos, almacenamiento en bloques)

What is the historic period, base year, and forecast period taken for North America Next Generation Data Storage Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Next Generation Data Storage Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2030

Who are the major players in North America Next Generation Data Storage Market?

The North America Next Generation Data Storage Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Dell Technologies Inc

Hewlett Packard Enterprise Co

NetApp Inc

Hitachi Ltd

International Business Machines Corp

Pure Storage Inc

DataDirect Networks Inc

Fujitsu Ltd

NETGEAR

Huawei Technologies Co Ltd

Who should buy this report?

The North America Next Generation Data Storage Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the North America Next Generation Data Storage Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For North America Next Generation Data Storage Market

1. Complete the form

2. Check your inbox (and spam/junk folder)

3. Your Personal Data is Secure with us

GDPR + CCPA Compliant

Personal & transactional information is kept safe from unauthorized use.

WHAT'S INCLUDED IN FULL REPORT : Market Dynamics,

Competitive Analysis and Assessment, Define Business Strategies, Market Outlook and

Trends, Market Size and Share Analysis, Growth Driving Factors, Future Commercial

Potential, Identify Regional Growth Engines

Get Free Sample For North America Next Generation Data Storage Market

Get Free Sample For North America Next Generation Data Storage Market