Pronóstico del mercado europeo de equipos de prueba automatizados hasta 2030 – Análisis regional – por tipo (pruebas de circuitos integrados (CI), pruebas de placas de circuito impreso (PCB), pruebas de unidades de disco duro (HDD) y otros), componente (PC industriales, interconexión masiva, y manejador/probador) y usuario final (electrónica de consumo, automoción, medicina, aeroespacial y defensa, TI y telecomunicaciones, y otras industrias)

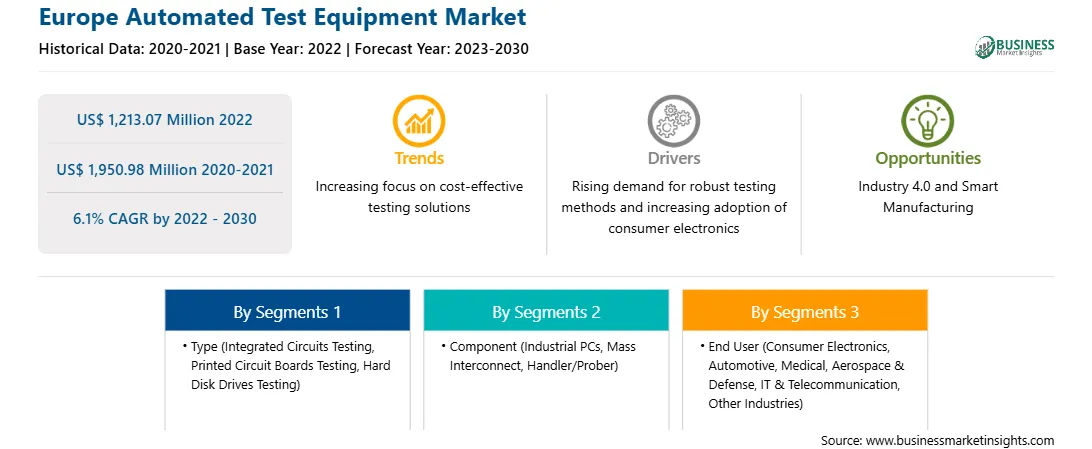

El mercado europeo de equipos de prueba automatizados se valoró en 1.213,07 millones de dólares en 2022 y se espera que alcance los 1.950,98 millones de dólares en 2030; se estima que registrará una tasa compuesta anual del 6,1% entre 2022 y 2030.

La creciente necesidad de capacidades de prueba de alta velocidad impulsa el mercado europeo de equipos de prueba automatizados

En un escenario altamente competitivo, el tiempo- La llegada al mercado de cualquier producto juega un papel extremadamente crítico. Un menor tiempo de comercialización del producto crea una mayor posibilidad para que la empresa obtenga una ventaja competitiva en el mercado. Las pruebas de productos consumen una cantidad excesiva de tiempo y recursos, lo que ralentiza el tiempo de lanzamiento de nuevos productos al mercado. Las pruebas tradicionales realizadas por técnicos en el banco tardan hasta dos semanas en caracterizar completamente un producto, incluido un amplificador de potencia de RF (PA), lo que lo convierte en un proceso largo, tedioso y repetitivo. Es costoso, ya que el costo de la mano de obra y el costo de la oportunidad perdida resultan en una pérdida de eficiencia, pérdida de ganancias y un mayor precio de los productos.

Las diferenciaciones de productos y precios se han reducido en los últimos tiempos. En tal escenario, las empresas buscan otros factores que puedan conducir a un mayor atractivo para los clientes en el mercado. Por lo tanto, las empresas de productos se esfuerzan por reducir el tiempo de comercialización de sus productos. La identificación de anomalías en las etapas iniciales permite tomar acciones más rápidas y conduce a un mayor ahorro de costos.

En épocas anteriores, las pruebas de los dispositivos se realizaban manualmente, lo que es en gran medida ineficiente e incapaz de manejar los volúmenes actuales de demanda. Estos métodos de prueba manuales también eran muy defectuosos y lentos. El aumento de la población en todo el mundo, junto con los crecientes ingresos de la clase media y la capacidad de gasto de los individuos, han dado lugar a una creciente demanda de productos en diversos sectores industriales. Las crecientes presiones para lograr economías de escala durante la fabricación, ayudadas por las crecientes capacidades de gasto de los individuos, impulsarían las integraciones de ATE en la industria de semiconductores.

Descripción general del mercado europeo de equipos de prueba automatizados

Las empresas de fabricación más destacadas en países europeos incluyen vehículos aeroespaciales, de maquinaria y equipos, automotrices, de construcción naval y militares. La industria automotriz contribuye significativamente al PIB de varios países de la Unión Europea (UE). Europa es el principal productor de vehículos de motor con presencia de varios fabricantes de automóviles premium, incluidos General Motors, Ford, Jeep, Chevrolet, Toyota, Nissan y Stellantis. La industria automotriz en Europa representa las mayores inversiones en I+D, incluidas las contribuciones de la industria privada y gubernamental. Según la Asociación Europea de Fabricantes de Automóviles (ACEA), en septiembre de 2023 se matricularon 8.61.062 unidades de automóviles nuevos en Europa. La región tiene casi 300 instalaciones de fabricación y ensamblaje de vehículos en ~26 países.

Según la ACEA, las instalaciones de fabricación en la UE representaron el 19,2% del total de automóviles fabricados en el mundo en 2022. Alemania tiene una participación significativa del 30% del mercado automotriz en la región. Los principales fabricantes de automóviles como VW, BMW, Opel, Daimler AG y Audi tienen una presencia notable en el país. En promedio, Alemania produce aproximadamente 6 millones de vehículos comerciales y de pasajeros cada año. Se prevé que la sólida industria del automóvil, especialmente la presencia de los principales fabricantes de automóviles premium, impulse el mercado de equipos de prueba automatizados en Europa. La Unión Europea planea invertir 1.900 millones de dólares para implementar 2,7 millones de puntos de carga públicos para 2030. Las inversiones se realizaron para fomentar el uso de vehículos eléctricos como una solución ecológica. Por lo tanto, se espera que el posterior aumento de las inversiones en la fabricación de baterías para automóviles eléctricos impulse el mercado de equipos de prueba automatizados en Europa en los próximos años.

Ingresos del mercado europeo de equipos de prueba automatizados y pronóstico hasta 2030 (millones de dólares estadounidenses)

Segmentación del mercado europeo de equipos de prueba automatizados

El mercado europeo de equipos de prueba automatizados se clasifica en tipo, componente, usuario final y país.

Según el tipo, el mercado europeo de equipos de prueba automatizados se segmenta en pruebas de circuitos integrados (CI), pruebas de placas de circuito impreso (PCB), pruebas de unidades de disco duro (HDD) y otras. El segmento de pruebas de circuitos integrados (CI) tuvo la mayor cuota de mercado en 2022.

En términos de componentes, el mercado europeo de equipos de prueba automatizados se clasifica en PC industriales, interconexión masiva y manipulador/probador. El segmento de PC industriales tuvo la mayor cuota de mercado en 2022.

Por usuario final, el mercado europeo de equipos de prueba automatizados está segmentado en electrónica de consumo, automoción, medicina, aeroespacial y defensa, TI y telecomunicaciones, y otras industrias. El segmento de electrónica de consumo tuvo la mayor cuota de mercado en 2022.

Por país, el mercado europeo de equipos de prueba automatizados está segmentado en Alemania, Francia, Reino Unido, Italia, Países Bajos y el resto de Europa. Alemania dominó la cuota de mercado europea de equipos de prueba automatizados en 2022.

Advantest Corp; Anritsu Corp; Averna Technologies Inc; Croma ATE Inc.; Corporación de Instrumentos Nacionales; SPEA SpA; Teradyne Inc; y Test Research, Inc. se encuentran entre las empresas líderes que operan en el mercado europeo de equipos de prueba automatizados.

Europe Automated Test Equipment Strategic Insights

Strategic insights for Europe Automated Test Equipment involve closely monitoring industry trends, consumer behaviours, and competitor actions to identify opportunities for growth. By leveraging data analytics, businesses can anticipate market shifts and make informed decisions that align with evolving customer needs. Understanding these dynamics helps companies adjust their strategies proactively, enhance customer engagement, and strengthen their competitive edge. Building strong relationships with stakeholders and staying agile in response to changes ensures long-term success in any market.

Get more information on this report

Europe Automated Test Equipment Report Scope

Report Attribute

Details

Market size in 2022

US$ 1,213.07 Million

Market Size by 2030

US$ 1,950.98 Million

Global CAGR (2022 - 2030)

6.1%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Tipo

Pruebas de circuitos integrados

pruebas de placas de circuitos impresos

pruebas de unidades de disco duro

By Componente

PC industriales

interconexión masiva

manipulador/sonda

By Usuario final

electrónica de consumo

automoción

medicina

aeroespacial y defensa

TI y telecomunicaciones

otras industrias

Regions and Countries Covered

Europa

Reino Unido

Alemania

Francia

Rusia

Italia

resto de Europa

Market leaders and key company profiles

Advantest Corp

Anritsu Corp

Averna Technologies Inc

Chroma ATE Inc.

National Instruments Corp

SPEA S.p.A.

Teradyne Inc

Test Research, Inc.

Get more information on this report

Europe Automated Test Equipment Regional Insights

The regional scope of Europe Automated Test Equipment refers to the geographical area in which a business operates and competes. Understanding regional nuances, such as local consumer preferences, economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved regions or adapting their offerings to meet regional demands. A clear regional focus allows for more effective resource allocation, targeted marketing, and better positioning against local competitors, ultimately driving growth in those specific areas.

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Europe Automated Test Equipment Market

1. Advantest Corp

2. Anritsu Corp

3. Averna Technologies Inc

4. Chroma ATE Inc.

5. National Instruments Corp

6. SPEA S.p.A.

7. Teradyne Inc

8. Test Research, Inc.

Frequently Asked Questions

How big is the Europe Automated Test Equipment Market?

The Europe Automated Test Equipment Market is valued at US$ 1,213.07 Million in 2022, it is projected to reach US$ 1,950.98 Million by 2030.

What is the CAGR for Europe Automated Test Equipment Market by (2022 - 2030)?

As per our report Europe Automated Test Equipment Market, the market size is valued at US$ 1,213.07 Million in 2022, projecting it to reach US$ 1,950.98 Million by 2030. This translates to a CAGR of approximately 6.1% during the forecast period.

What segments are covered in this report?

The Europe Automated Test Equipment Market report typically cover these key segments-

Tipo (Pruebas de circuitos integrados, pruebas de placas de circuitos impresos, pruebas de unidades de disco duro)

Usuario final (electrónica de consumo, automoción, medicina, aeroespacial y defensa, TI y telecomunicaciones, otras industrias)

What is the historic period, base year, and forecast period taken for Europe Automated Test Equipment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Automated Test Equipment Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2030

Who are the major players in Europe Automated Test Equipment Market?

The Europe Automated Test Equipment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Advantest Corp

Anritsu Corp

Averna Technologies Inc

Chroma ATE Inc.

National Instruments Corp

SPEA S.p.A.

Teradyne Inc

Test Research, Inc.

Who should buy this report?

The Europe Automated Test Equipment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Automated Test Equipment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Automated Test Equipment Market

1. Complete the form

2. Check your inbox (and spam/junk folder)

3. Your Personal Data is Secure with us

GDPR + CCPA Compliant

Personal & transactional information is kept safe from unauthorized use.

WHAT'S INCLUDED IN FULL REPORT : Market Dynamics,

Competitive Analysis and Assessment, Define Business Strategies, Market Outlook and

Trends, Market Size and Share Analysis, Growth Driving Factors, Future Commercial

Potential, Identify Regional Growth Engines

Get Free Sample For Europe Automated Test Equipment Market

Get Free Sample For Europe Automated Test Equipment Market