亚太地区飞机等温锻造市场预测至 2028 年 – COVID-19 影响和区域分析 – 按飞机零部件(风扇叶片、涡轮盘、轴和连接器环)、锻造材料(钛和镍基高温合金)、和配合类型(直线配合和改造)

No. of Pages: 136 | Report Code: BMIRE00025578 | Category: Aerospace and Defense

No. of Pages: 136 | Report Code: BMIRE00025578 | Category: Aerospace and Defense

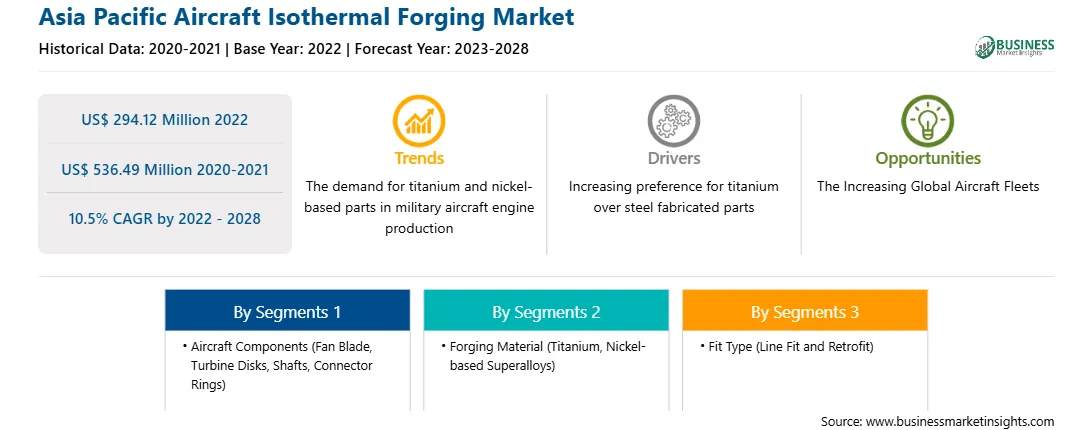

在军用飞机生产的各种应用中采用钛和镍基零件预计这种上升趋势将推动飞机等温锻造市场的发展。对轻质材料的需求不断增加,每架飞机钛和镍基发动机零件的使用率不断提高。此外,军用飞机模型和直升机的各种部件,如法兰、肋骨、蒙皮、纵梁、加强筋和护罩,形成飞机发动机结构,都是借助等温锻造钛合金或镍合金制造的。例如,在印度,为印度空军捷豹/鹰飞机提供动力的Adour 804/811和871发动机使用镍基和钛基合金,预计这将增加对钛和镍基零部件的需求。钛的热膨胀率使其非常适合作为军用飞机生产的复合界面材料。此外,钛和镍以其高强度重量比而闻名,使其成为军用飞机制造领域飞机制造的理想材料。此外,钛和镍基零件还耐腐蚀,这使得它们成为军用飞机生产的不错选择。这些轻质而坚固的金属适合制造军用飞机和飞机发动机部件。因此,这一趋势预计将在预测期内推动飞机等温锻造市场的增长。

亚太地区飞机等温锻造市场细分为飞机零部件、锻造材料、装配类型和国家/地区。根据飞机零部件,亚太地区飞机等温锻造市场分为风扇叶片、涡轮盘、轴和连接环。预计到 2022 年,风扇叶片领域将占据最大的市场份额。根据锻造材料,亚太地区飞机等温锻造市场分为钛和镍基高温合金。预计202年镍基高温合金将占据更大的市场份额2。按照配合类型,亚太地区飞机等温锻造市场分为线配合和线配合。改造部分。预计到 2022 年,线配合细分市场将占据更大的市场份额。基于国家,亚太地区飞机等温锻造市场细分为澳大利亚、中国、印度、日本、韩国和亚太地区其他地区。 2022年,中国在飞机等温锻造市场中占据最大份额。

主导亚太飞机等温锻造市场的主要参与者包括美国铝业公司、ALD Vacuum Technologies GmbH、 ATI、HC Starck Solutions、Howmet Aerospace、Leistritz Turbinentechnik GmbH、LISI Aerospace、SCHULER GROUP 和 SMT Limited。

Strategic insights for Asia Pacific Aircraft Isothermal Forging involve closely monitoring industry trends, consumer behaviours, and competitor actions to identify opportunities for growth. By leveraging data analytics, businesses can anticipate market shifts and make informed decisions that align with evolving customer needs. Understanding these dynamics helps companies adjust their strategies proactively, enhance customer engagement, and strengthen their competitive edge. Building strong relationships with stakeholders and staying agile in response to changes ensures long-term success in any market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 294.12 Million |

| Market Size by 2028 | US$ 536.49 Million |

| Global CAGR (2022 - 2028) | 10.5% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By 飞机部件

|

| Regions and Countries Covered | 亚太地区

|

| Market leaders and key company profiles |

The regional scope of Asia Pacific Aircraft Isothermal Forging refers to the geographical area in which a business operates and competes. Understanding regional nuances, such as local consumer preferences, economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved regions or adapting their offerings to meet regional demands. A clear regional focus allows for more effective resource allocation, targeted marketing, and better positioning against local competitors, ultimately driving growth in those specific areas.

The Asia Pacific Aircraft Isothermal Forging Market is valued at US$ 294.12 Million in 2022, it is projected to reach US$ 536.49 Million by 2028.

As per our report Asia Pacific Aircraft Isothermal Forging Market, the market size is valued at US$ 294.12 Million in 2022, projecting it to reach US$ 536.49 Million by 2028. This translates to a CAGR of approximately 10.5% during the forecast period.

The Asia Pacific Aircraft Isothermal Forging Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Aircraft Isothermal Forging Market report:

The Asia Pacific Aircraft Isothermal Forging Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Asia Pacific Aircraft Isothermal Forging Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the Asia Pacific Aircraft Isothermal Forging Market value chain can benefit from the information contained in a comprehensive market report.

Office No. 1011, First floor, Farena Corporate Park, Magarpatta-Mundhwa road, Pune - 411028, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Asia Pacific Aircraft Isothermal Forging Market

Get Free Sample For Asia Pacific Aircraft Isothermal Forging Market